A Passage to India

India is joining the world's major bond benchmarks. Why the long-term case for its local bonds is a marathon, not a sprint.

At the end of this month, India will enter the JPMorgan GBI-EM Global index suite after a decade-long evaluation by the index provider. In many ways, the inclusion appears long overdue. India has the second-largest domestic debt market in EM. The country is the last BRICS member to be index-eligible since the inception of EM local debt benchmarks in June 2005 (notwithstanding Russia’s removal in March 2022). Moreover, foreign access to its equity market has been progressively liberalized. India was added to the MSCI EM index three decades ago, and its benchmark weight of 18% is currently the second highest after China.

Regardless, the global investor should welcome the latest developments. Since assuming office ten years ago, Prime Minister Narendra Modi has made economic reforms a key priority. By GDP, India now ranks as the fifth largest and tops four G7 nations (UK, France, Italy and Canada). Last year, it overtook China to become the world’s most populous country. Almost two-thirds of its population are under the age of 35, contrasting the aging demographics in Western Europe and most of Asia. India also stands to benefit from being an alternative to China for supply chain diversification. These secular tailwinds underpin market expectations of India achieving the fastest growth among major economies in the next two years, with the IMF projecting at least 6.5% per annum.

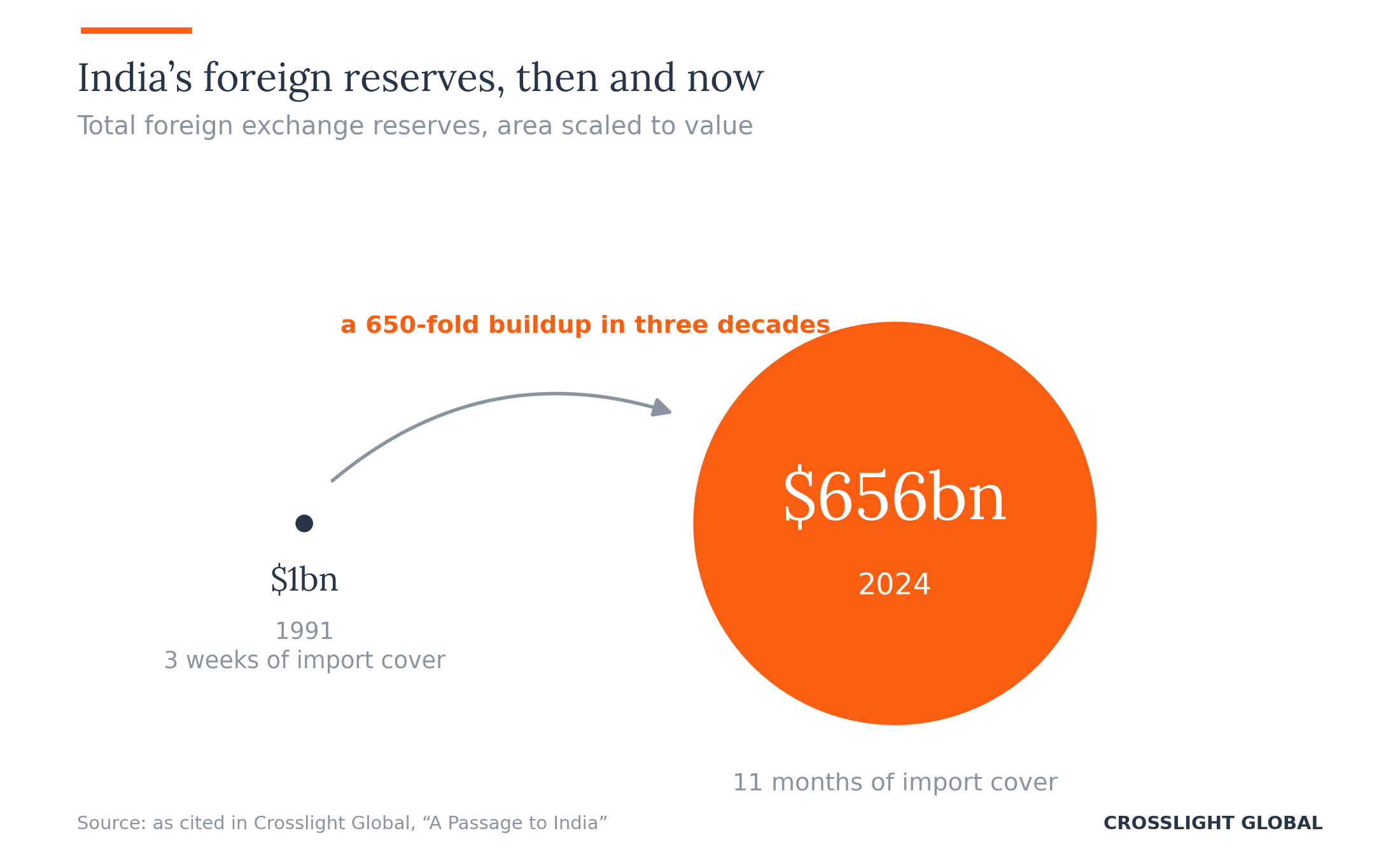

To be sure, the foundation of market liberalization was laid thirty years ago as a response to a balance-of-payments crisis in 1991. At the lowest point, foreign reserves were depleted to barely $1 billion, enough for just three weeks of imports. Turning its back on the post-independence import-substitution model, India adopted market-opening measures by encouraging foreign direct investment (FDI), abolishing import-restraining industrial licensing, and devaluing the currency by 20% to spur exports. India became a member of the World Trade Organization (WTO) in 1995, seven years ahead of China. Since then, the buildup in the country’s external buffer has been nothing short of spectacular. Foreign reserves now stand at a record $656 billion, equivalent to 11 months of import coverage.

Yet, beyond these headline-grabbing achievements, macroeconomic anxiety in India stays high for a couple of reasons. First, whilst a phenomenal expansion in services exports has helped narrow the current account shortfall, the manufacturing trade deficit remains elevated. Thematically speaking, this owes to India’s unconventional transformation from agriculture to services, leapfrogging manufacturing as a result. This stands in contrast with the industry-led experience in China, where massive trade surpluses helped contribute to reserve accumulation. Second, the composition of capital inflows has deteriorated, with increased reliance on the more volatile portfolio inflows amid stagnating FDI. This probably explains the extended time taken for the index inclusion talks, as well as a longstanding official aversion to hard currency sovereign debt issuance. (India is the only country in the EMBIG index without a USD government bond.)

Fundamentally, CrossLight views the case for an allocation to local bonds in India as compelling. The ingredients for continued economic expansion are in place, and the incoming Modi-led coalition government is expected to stay committed to long-term economic priorities. S&P’s move in late May to raise the outlook on the country’s BBB- rating underscores the agency’s constructive view. That said, we would curb market enthusiasm on near-term currency appreciation on the basis of index inclusion since the decision has been well-telegraphed ahead of time in September 2023. Instead, our investment thesis centers on long-term value and diversification and considers bond investing in India as a marathon rather than a sprint.

---

Tags: India, Emerging Markets, Fixed Income, Global Macro, Bond Index