Back to the Future in Latin America

Latin America's growth never matched the hype. Why the case for the region's bonds is shifting back from growth to value.

(At the height of the Lava Jato scandal in the second half of 2015, the policy rate in Brazil reached 14.25%, more than 11 points above Mexico’s 3%.) In both countries, while efforts to tame inflation remain unfinished, policymakers have turned more wary of growth.

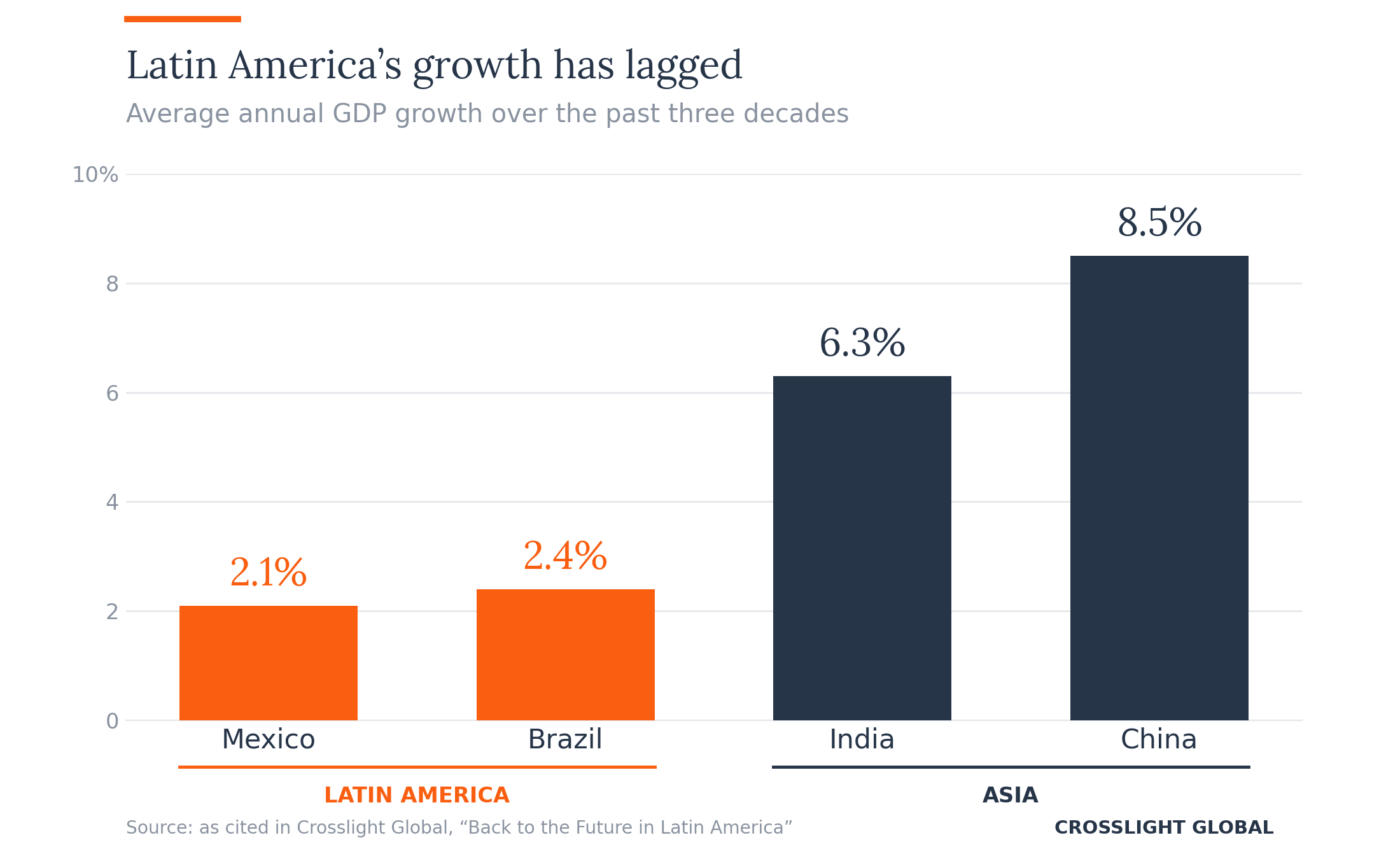

Indeed, by EM standards, their historical growth records are surprisingly mediocre. In the past three decades, annual GDP growth in Mexico and Brazil averaged 2.1% and 2.4% respectively, well below China (8.5%) and India (6.3%). Interestingly, for Mexico, there is scant evidence of a long-term boost from NAFTA membership over this period. Among other factors, this likely reflected a stubbornly large informal sector domestically, as well as the concurrent emergence of China as a competitor.

Whilst realized growth fell short, secular optimism regarding the global commodity cycle nonetheless fueled market interest in LatAm assets. Investors and rating agencies alike jumped on the bandwagon. Between April 2008 and February 2016, Brazil was rated investment grade by at least one of the three rating agencies. It has since reverted to the junk category (Ba2/BB/BB). On the other hand, Mexico has managed to retain its investment grade status (Baa2/BBB/BBB-), although ratings are off the historical high of single-A.

For bond investors, EM and LatAm are often used, or at least thought of, interchangeably. This owes to the fact that the investable pool was initially concentrated in the region. (In 1994, the benchmark weight of LatAm in the JPMorgan Emerging Markets Bond Index topped 85%.) In the early stages, the investment proposition was primarily value-driven, typically as a result of political uncertainty or economic turmoil. In the post-millennium years, the growth wave emanating from the China boom fortified investor interest. A generalized EM love fest, one that outlasted the Global Financial Crisis, was thus propelled by the twin engine of value and growth.

In CrossLight’s view, the case for LatAm investing is retrogressing toward value hunting. Idiosyncratic country factors are once again exerting a greater influence on asset prices. To be sure, with higher rates globally, a market outcome where a rising tide lifts all boats is unlikely. Instead, there will be increased differentiation based on individual merits. In the wake of Moody’s recent outlook revision to positive, Brazil’s ability to push through reforms will be under scrutiny. The outcome of next month’s general elections in Mexico will have implications for medium-term fundamental trends. As the policy cycle progresses, rate differentials could become more entrenched, and in turn, spawn relative trade opportunities. The upshot is that as with the pioneer participants of EM, a global investor today can benefit from the value that LatAm bonds offer at different points of the market cycle.

---

Tags: Latin America, Emerging Markets, Fixed Income, Brazil, Mexico, Global Macro