China's Growth Dilemma

China's miracle decade is over. Why its growth is turning more DM-like, and why it still leans on producing more than consuming.

Released ahead of the Golden Week holidays in China, the April PMI prints came in as expected at slightly above par and yielded few cyclical signals that were of note. Yet, the relative stability of leading indicators belies longer-term growth challenges that policymakers themselves are likely well aware of. Here, we propose two macro takeaways on China. First, the growth trajectory in the coming years will increasingly become more DM-like. Second, unlike large DM countries, China remains more of a producer than a consumer.

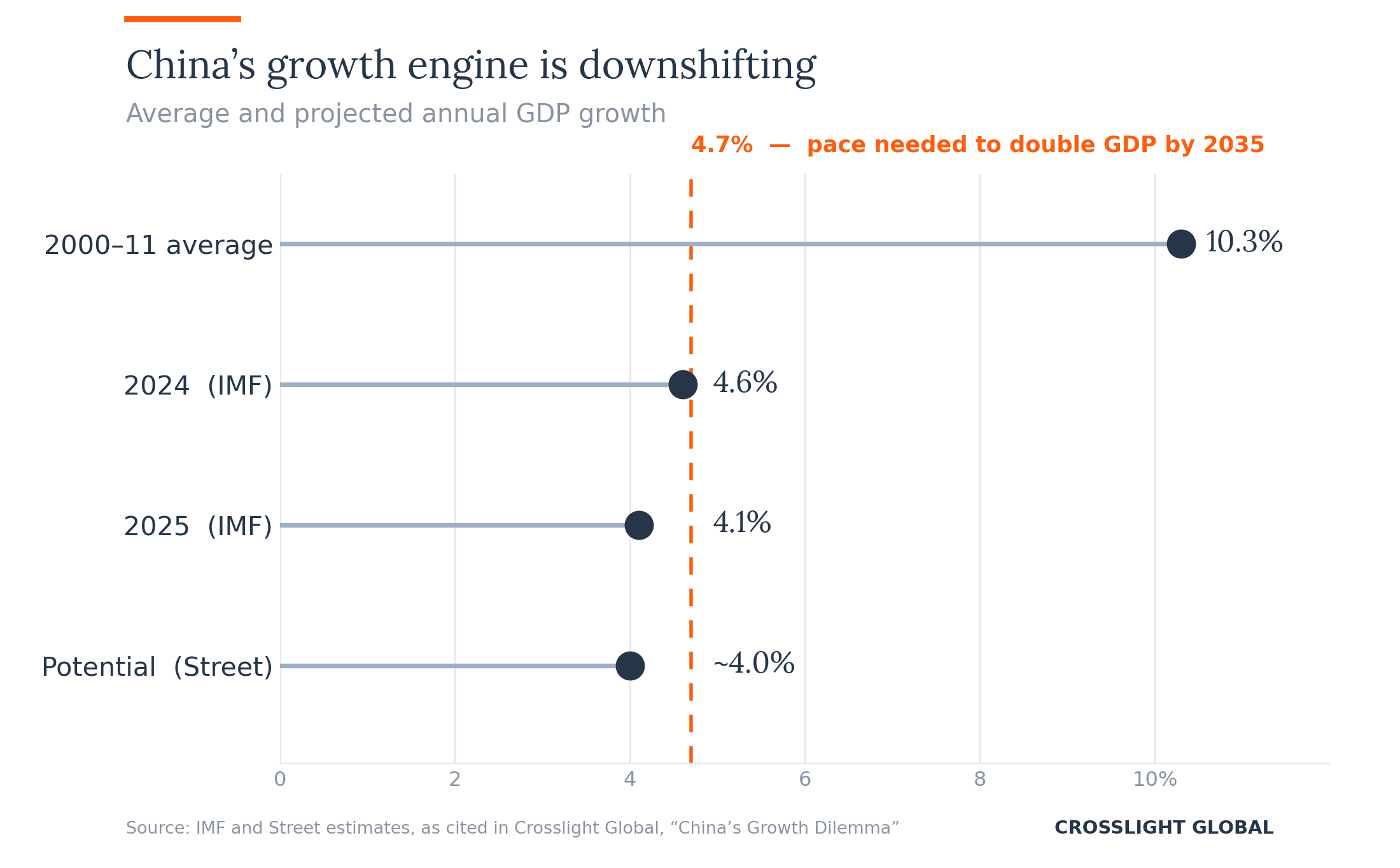

To be sure, the eye-watering 10.3% average growth achieved between 2000 and 2011 was, in many respects, a result of a rare confluence of one-off factors, notably favorable demographics, trade liberalization and constructive geopolitics. However, rapid expansion within a relatively short period of time has unintended socioeconomic consequences. To address these tradeoffs, the policy design on growth in the last decade has pivoted toward favoring quality over quantity.

Indeed, trends in production factors, particularly labor input, have unambiguously reversed. Working-age population peaked in 2011, while the overall population has begun to shrink since 2022. On global trade, Sino-US tensions have remained rife since the imposition of US tariffs on Chinese imports in 2018. In early April, the USTR initiated investigations relating to China’s dominance in the maritime, logistics and shipbuilding sectors. The ongoing EU probe since late-2023 into China-made electric vehicles is another case in point.

Despite a build-up in structural obstacles, the commitment to the 2020 vision of doubling the country’s GDP by 2035 is tacitly intact on the policy agenda. Achieving this goal would require an average growth of 4.7% per annum between 2020 and 2035. As a back-of-envelope comparison, the IMF expects China’s growth to moderate to 4.1% in 2025 from this year’s 4.6%. Street estimates of potential GDP growth vary but typically converge to around 4%.

All things equal, sustaining long-term growth requires consumption to play a more dominant role, given its economic maturation. Recall that, in the past, the decision by foreign MNCs to establish local manufacturing plants was made not just to benefit from low costs, but also to position themselves for the expansive domestic market. For now, the Chinese economy is mired in a Catch-22 situation, as asset market doldrums and a weak social safety net will constrain household spending.

For now, favoring production over consumption appears to be the official rule. To China’s credit, policymakers have dealt head-on with excesses by shifting the investment focus away from real estate toward new sectors, including high-tech, IT, and green economy. As highlighted earlier, a production-centered strategy is not without challenges, especially given the current geopolitical climate. Consequently, the investment focus will continue to center on at least two trade-related themes: (1) a continuation of a China+1 strategy by MNCs, of which India and Southeast Asia have been key beneficiaries, and (2) the creation of intermediary manufacturing facilities by Chinese firms in countries that are close to the final destination of its exports.

---

Tags: China, Global Macro, Emerging Markets, Trade, Fixed Income