Crosslight Monthly Perspective - June 2026 (Vol.1, No.3)

Booming markets, a flagging economy. Speed bumps ahead.

### KEY TAKEAWAYS

- Soaring asset prices alongside a rising cost of living point to a lopsided, K-shaped recovery

- A Middle East ceasefire may cheer markets, but the jump in prices it caused will linger…

- …leaving central banks far less room to cut rates and spur growth

### MARKET RECAP: May the Force Be with You

Risk assets rose for a second month running in May, carrying world markets to fresh highs. It is a lopsided rally. A handful of technology firms are doing the heavy lifting, even as household names such as Walmart and Whirlpool warn that their sales are sliding. And for all the on-again, off-again headlines about the Strait of Hormuz, investors are betting on a US-Iran peace deal: oil has slipped to a one-month low.

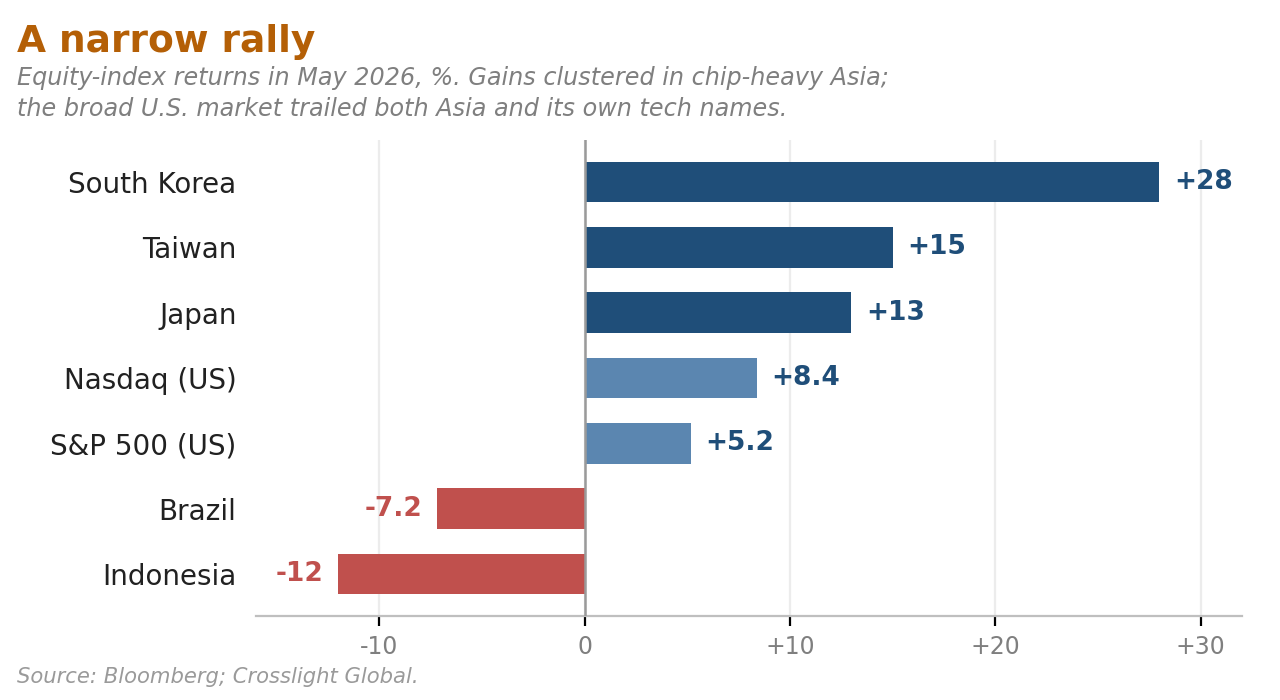

**Equities.** Shares climbed again as enthusiasm for technology drowned out the noise from the Gulf. North Asia set the pace, with South Korea up 28%, Taiwan 15% and Japan 13%, all riding their chipmakers. Closer to home, the tech-heavy NASDAQ (+8.4%) again left the broader S&P 500 (+5.2%) trailing – a reminder that, for now, a plain US index fund is largely a wager on a handful of technology names. The laggards had troubles of their own: Indonesia fell for a fifth straight month (-12%) as the index provider MSCI kept questioning the transparency of its market, while Brazil dropped 7.2% after a banking scandal caught up with the front-runner in October’s presidential election.

**Bonds.** Yields rose across the rich world – in plain terms, governments had to pay more to borrow. The number that matters most at home: the 30-year US Treasury yield finished the month at 4.97%, a post- pandemic high, and that feeds straight through to mortgage rates and corporate borrowing costs. Britain was the louder drama. Its 30-year gilt touched 5.85% in mid-May, the highest since 1998, as Sir Keir Starmer fought off challenges to his leadership, before cheaper oil pulled it back to 5.52% by month-end – still the steepest in the G7.

**Currencies.** The dollar firmed against the other big currencies as investors came round to the idea that the Fed’s next move is up, not down. The yen slipped 1.7% even after Tokyo spent a remarkable $73.6 billion between April 28 and May 27 trying to hold it up. The same taste for risk that lifted shares rewarded the racier currencies, led by the South African rand (+2.7%), the Hungarian forint (+2.4%) and the New Zealand dollar (+1.4%).

**Commodities.** A mixed month. Brent crude tumbled almost 20% as hopes of a US-Iran ceasefire revived – welcome relief for American drivers after a punishing spring at the pump. Silver did best of the precious metals, up 2%, though that still leaves it 35% below the record it set at the end of January. Gold found few buyers even as nerves steadied, slipping 1.7%.

### LOOKING AHEAD THIS MONTH

**Economic data.** America’s jobs report on Friday is the week’s main event; analysts expect hiring to have cooled to a three-month low of 89,000 in May. The ISM surveys of factory (Mon) and services (Wed) activity should hold roughly steady, pointing to a stable near-term outlook. In the euro zone, inflation (Tue) is thought to have edged up to 3.2% from a year earlier. In Asia, the activity surveys out of China, South Korea and Taiwan (Mon) are likely to stay healthy, while India’s first-quarter GDP (Fri) is forecast at a brisk 7.0%.

**Central bank watch.** The Reserve Bank of India will most likely keep its rate at 5.25% on Friday, while making clear it stands ready to act against rising inflation and a softer rupee. Poland’s central bank is expected to hold on Tuesday. The diary is thick with speeches, among them Bank of Japan Governor Kazuo Ueda (Wed), the ECB’s Christine Lagarde (Thurs) and a parade of Fed officials (Tue-Thurs).

**International trade.** Ahead of the July 1st review of the USMCA, North America’s trade pact, the first bilateral talks have begun, with America pressing for a rule that half of every car’s content be made in the US. China’s foreign minister, Wang Yi, paid a three-day visit to Canada, the latest effort to warm relations. And Washington has opened a third trade probe into Vietnam, this time over intellectual property.

### FOCUS THEME: Speed Bumps Ahead for the Global Economy

The gulf between booming markets and a flagging economy is a classic Dickensian contrast.

**”It was the best of times.”** After a wobble in March, global equities turned up again, driven by a seemingly insatiable appetite for technology and AI. America’s three big benchmarks – the S&P 500, the Dow and the NASDAQ – all ended May at record highs. South Korea’s KOSPI has risen an eye-watering 101% this year, though that owes much to two giants that tower over the index, Samsung Electronics (27%) and SK Hynix (25%). Nearby, Taiwan’s stockmarket, now worth $4.95 trillion, edged past India’s ($4.93 trillion) to become the world’s fifth largest. Its economy grew 14.6% in the first quarter, figures last week showed – the fastest since 1981, and a reminder of how thoroughly the island dominates the making of semiconductors.

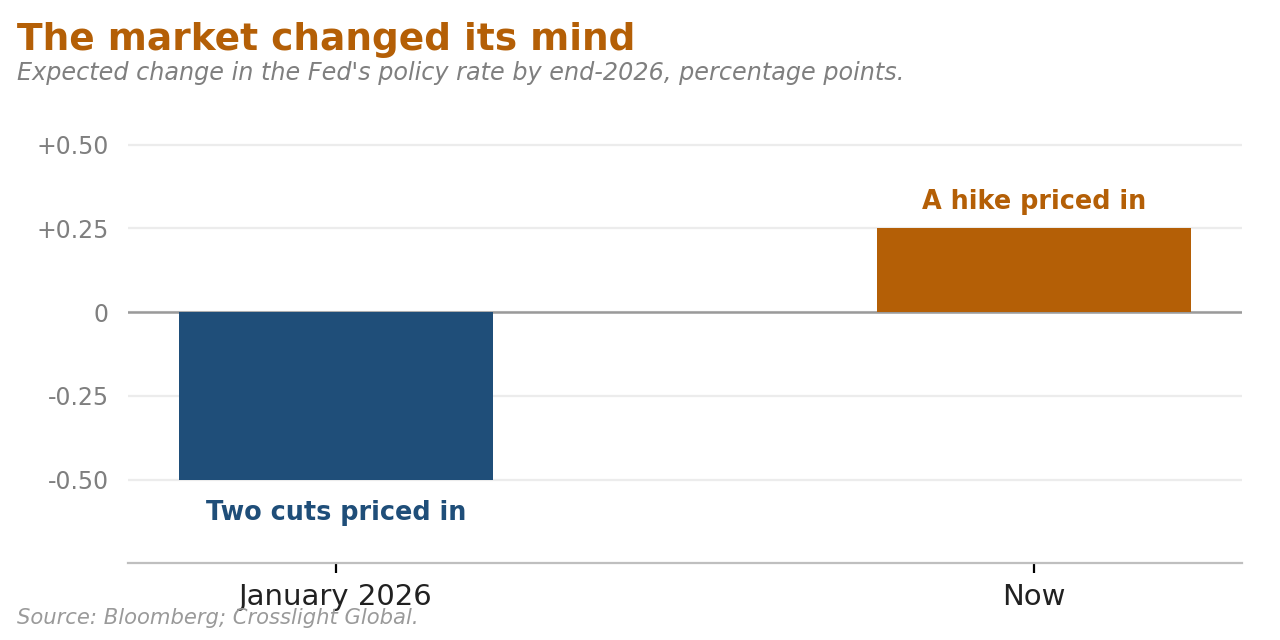

**”It was the worst of times.”** Geopolitics and inflation, meanwhile, are making the global growth engine sputter. Canada has slipped into recession for the first time since the pandemic, its economy shrinking for a second straight quarter (by an annualized 0.1%). America is sturdier, though less than it first looked: first- quarter growth was revised down to an annualized 1.6%, from 2.0%. The Fed’s preferred inflation gauge, core PCE, rose 3.3% in the year to April – its quickest in two and a half years, and well above the 2% target. Consumer confidence, as measured by the University of Michigan, sank to 44.8, the lowest since the survey began in 1952. Whirlpool, which makes household appliances, warned of a “recession-level industry decline.” And the share of credit-card debt at least 90 days overdue hit 13.12% in March, a 15-year high. This K-shaped path leaves central banks with an awkward choice. Even if the Strait of Hormuz reopens, tangled supply chains will take time to clear, so tighter policy is needed to keep a lid on inflation. Yet easier policy – the obvious salve for a slowing real economy – sits uncomfortably beside asset prices that are already at record highs. For now the hawks have the louder voice. In the rich world, the central banks of Australia, the euro zone, Japan, New Zealand and Britain have all signaled a readiness to lean against inflation. Among emerging markets, Indonesia, the Philippines and South Africa have been raising rates since late March, and Turkey is expected to resume tightening in June. Even in Brazil, which has been cutting, a senior official insisted that “lowering rates does not mean” the bank has turned dovish – a hint that the easing is about to pause. Putting price stability ahead of growth points to speed bumps in the second half of the year. Nor can governments easily spend their way around them: debt loads are already too high almost everywhere. Oil importers are the most exposed, though snarled supply chains will pinch everyone. An outright recession is not impossible, but it looks unlikely – the wealth created by rising asset prices should cushion the blow. Step back, and a larger theme is coming into focus: the decades-long era of cheap money is ending. When borrowing was all but free – as it was ten years ago, when Japan and Europe ran negative rates – buying risky assets was easy money in itself. No longer. From here, returns will hinge far more on valuations, on how crowded a trade has become, and on the next surprise from policymakers. Both the Bank of Japan and the ECB have sharpened their hawkish language, and each is expected to raise rates by a quarter-point in June. In America, the market has swung from pricing in two Fed cuts this year to betting on a hike near year-end.

**What this means for portfolios.** We continue to favor allocating capital to select international assets. With interest rates higher abroad – especially across emerging markets – and the Fed likely on hold for the rest of the year, foreign currencies now offer a yield cushion against the dollar that they lacked for years. A fresh geopolitical flare-up could send investors scurrying back to the greenback for a time, but, in our view, the strategic drift is toward other currencies and precious metals.

### HEARD THROUGH THE GRAPEVINE

**The $1.776 billion question.** Our cover is not only history. This month, the Justice Department moved to establish a fund of exactly that size – styled the “Anti-Weaponization Fund” – to compensate people who say they were wrongly investigated by earlier administrations, funded by settling the President’s own lawsuit against the IRS. Supporters call it overdue redress; critics call it a slush fund for political allies. We take no view on the politics. The reason it earns the cover is narrower, and it is the thread running through this issue: it is an extraordinary use of public money at a moment when government balance sheets almost everywhere are already stretched. Bond investors price fiscal credibility for a living, and gestures like this are precisely what they notice.

**Tokyo’s $73.6 billion bill.** To stop the yen from sliding further, Japan spent $73.6 billion in a single month propping it up – an enormous sum, and a quietly important one for American investors. Interventions on that scale are funded by selling dollar reserves, and Japan keeps much of those reserves in US Treasuries; it is the largest foreign owner of US government debt. One month of yen-defending does not move a market the size of America’s. But it fits a pattern we keep flagging: when foreign central banks are forced to sell Treasuries to defend their own currencies, the natural buyer of US debt thins out – and that, over time, nudges American mortgage and borrowing costs higher.

**Sources**

Bloomberg; University of Michigan Surveys of Consumers; US Bureau of Labor Statistics; Institute for Supply Management; US Bureau of Economic Analysis; Statistics Canada; Eurostat; central-bank statements and minutes (Federal Reserve, Bank of Japan, European Central Bank, Reserve Bank of India, National Bank of Poland); Moody’s Investors Service and S&P Global Ratings; International Monetary Fund, World Economic Outlook; US Department of the Treasury TIC data; company filings and guidance (Walmart, Whirlpool); US Department of Justice; Reuters; Financial Times; The Wall Street Journal. Cartoon: Thomas Nast, “Who Stole the People’s Money? — ‘Twas Him,” Harper’s Weekly, August 19, 1871 (Library of Congress Prints & Photographs Division; public domain).