WEEKLY PERSPECTIVES

February 1, 2026

KEY TAKEAWAYS

· Asset price volatility is likely to persist amid evolving geopolitics and technical factors

· Fed chair pick and sticky producer prices suggest limited scope for near-term easing

· Outside the US, countries are seeking to reengage with trade partners

MARKET RECAP

Global assets ended January mostly higher, though returns masked sharp, event-driven volatility across markets.

· Precious metals saw the most dramatic swings. After surging to record highs earlier in the month, gold and silver plunged on January 30 (-9% and -26%, respectively), marking the steepest single-day declines in decades. Despite the selloff, gold finished January up +13% and silver +19%.

· Equities posted mixed leadership. US stocks rose +1.4%, with the S&P briefly reaching a new high, but non-US markets continued to outperform. Korea led (+24%), with Colombia, Brazil, and Taiwan also delivering double-digit gains, while Indonesia lagged (-3.7%) amid MSCI downgrade concerns.

· Bond markets were unsettled. The US 10-year Treasury yield ended January at 4.24%, up 7 bps, driven by European fund outflows and firmer producer-price data. Japanese bonds sold off after Prime Minister Takaichi announced snap elections for early February.

· Currency and energy markets reflected shifting policy and geopolitical risk. The dollar strengthened late in the month following President Trump’s selection of Kevin Warsh as Fed chair, though the DXY still fell 1.2% in January. Commodity currencies outperformed, while energy prices surged — natural gas rose nearly +40% during an Arctic cold snap, and crude climbed +14% on heightened Iran-related tensions.

LOOKING AHEAD THIS WEEK

This week’s focus is on the January nonfarm payrolls report (consensus +68k), which should offer further clarity on the trajectory of the US labor market. A partial government shutdown began over the weekend, though passage of a Senate-backed funding bill early this week is expected to reopen the government.

On the policy front, the Reserve Bank of Australia is expected to deliver its first rate hike in two years on Tuesday, raising the cash rate by 25 bps to 3.85%, while the ECB is likely to leave rates unchanged at Thursday’s meeting.

Geopolitical risks remain elevated. The US–Russia New START treaty expires on February 4 with no extension in place, ending formal nuclear constraints for the first time since the 1970s. At the same time, speculation around a potential US strike on Iran persists amid a visible buildup of military assets in the Gulf.

FOCUS THEME: Revisiting the Plaza Accord

The Japanese yen rebounded 1.3% against the dollar in January, snapping a multi-month depreciation that had pushed it near its weakest level in 36 years. The move was driven largely by speculation of coordinated support involving Japan’s Ministry of Finance and the New York Fed.

Market confidence in Japan, however, remains fragile. On January 20, Japanese government bonds experienced a “Liz Truss–style” shock following ambitious fiscal spending signals, with long-dated yields jumping nearly 30 bps in a single session. While yields have since retraced, the 30-year JGB still sits near all-time highs at 3.63%, a stark contrast to just 0.05% a decade ago.

These developments have revived comparisons to the Plaza Accord of September 1985, when the G5 nations jointly intervened to weaken an overvalued US dollar. After the dollar fell sharply, the Louvre Accord followed in 1987 to stabilize currencies. Despite surface parallels, we see important differences that make a modern-day replay unlikely.

First, dollar strength ahead of the Plaza Accord was far more extreme. The DXY nearly doubled between 1980 and 1985 amid aggressive monetary tightening that pushed the effective fed funds rate above 20%. Today’s dollar strength reflects a slower, structural appreciation since the global financial crisis rather than a sharp cyclical overshoot.

Second, the current geopolitical environment is far less conducive to coordinated action. The original intervention targeted multiple currencies, yet recent unilateral efforts by Japan to support the yen — in 2022 and again in 2024 — have had limited and short-lived impact.

Third, the Plaza Accord addressed severe US trade imbalances with its largest partners. Replicating such an effort today would require China’s participation, given the size of the US-China trade deficit. Given Japan’s experience with prolonged stagnation and China’s own structural challenges, a policy-engineered currency revaluation appears politically and economically implausible.

HEARD THROUGH THE GRAPEVINE

The World Economy Is Hooked on Government Debt — Governments are increasingly carrying global growth through deficit-financed spending, masking weak private demand but raising long-term risks as debt-service costs rise in a higher-rate world. (WSJ)

Xi Jinping calls for China’s renminbi to attain global reserve currency status — Beijing is making its clearest push yet for the renminbi to play a larger role in global finance, though capital controls and limited convertibility remain significant barriers to reserve status. (FT)

OPEC+ agrees to keep oil output unchanged as tensions with Iran boost prices. OPEC+ held production steady in March despite rising crude prices, underscoring producers' caution amid geopolitical risks that add a fresh inflation premium to energy markets. (Reuters)

What will Kevin Warsh’s Federal Reserve look like? — Kevin Warsh’s nomination signals a Fed skeptical of quantitative easing and more politically exposed, raising questions around independence even as markets take comfort in his institutional experience. (The Economist)

Gold and Silver Prices Fall Sharply as Trump Picks Warsh as Fed Chair. Here’s Why. — Precious metals sold off sharply after Warsh’s nomination boosted the dollar and triggered profit-taking in crowded “Fed credibility” and debasement trades. (Barron’s)

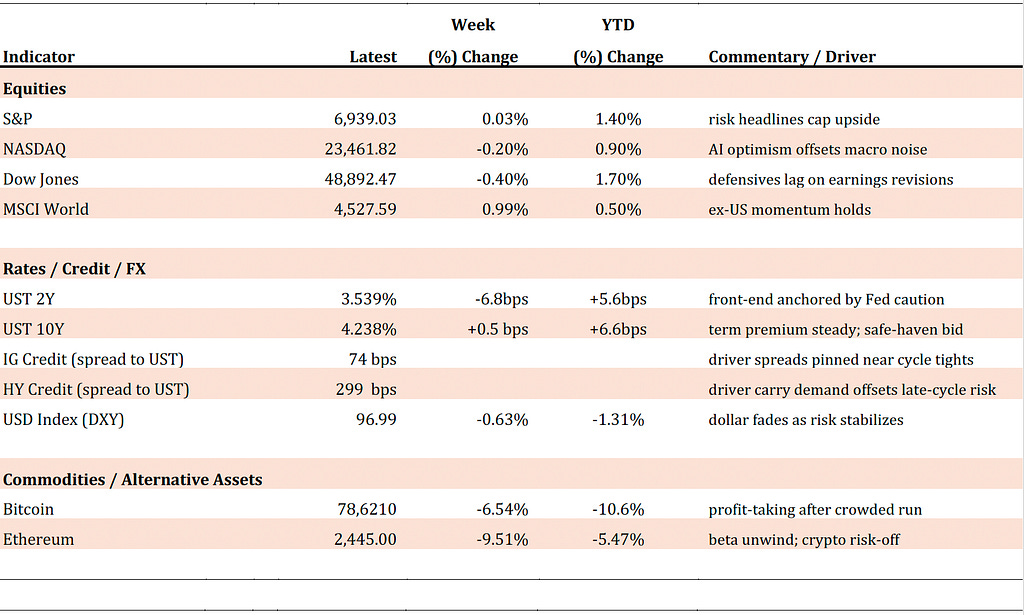

MARKET DASHBOARD

Thank you for reading CrossLight’s Weekly Perspectives. This note is strictly for informational purposes only and does not constitute investment advice for the reader.