Silver isn’t a commodity. It’s a risk asset — just ask the IMF.

KEY TAKEAWAYS

● Consumer resilience continues to be supportive of US growth

● Rotation by sector and geography reflects theme of defensiveness and diversification

● Deleveraging concerns in risk assets are a key market factor to watch

MARKET RECAP

Financial markets ended a volatile week off the lows after a sharp Friday rebound in risk assets.

● Precious metals and cryptocurrencies had another roller-coaster week, marked by key price breaks amid concerns about deleveraging. Silver plunged -20% on Thursday, ahead of a COMEX hike in margin requirement to 18% from 15%. Bitcoin briefly touched a 15-month low of $60,000 and finished the week down 12%.

● Bonds were mostly firm amid a retreat in risk assets. The 10-year Treasury yield closed at a 10-day low of 4.21%, as weak labor market data offset solid consumer sentiment. Markets are pricing in two rate cuts this year, despite Fed Chair nominee Kevin Warsh’s reputation as a balance sheet hawk.

● Equities saw flows rotate out of technology into defensive and value plays (consumer staples, industrials, and energy). The Dow Jones Index advanced +2.5% to print above the 50,000 level for the first time, while the S&P ended flat on the week. Outside the US, Europe, India, and Japan rallied, while Australia, China, and South Korea consolidated.

● Major currencies took a breather from the weak-dollar theme. The Japanese yen lost -1.6% ahead of this weekend’s snap elections, while the Euro pared losses by 0.3%. However, EM FX generally outperformed, led by the Indian rupee (+1.5%) and the Mexican peso (+1.1%).

LOOKING AHEAD THIS WEEK

The upcoming week is relatively quiet on the data front, except for the delayed release of the January non-farm payroll report (consensus +69k) on Wednesday, due to the brief government shutdown, and the January CPI (consensus +2.5% yoy) on Friday. The annual Munich Security Conference takes place on February 13–15, providing a timely forum for discussing global security issues, including military conflicts and cybersecurity.

FOCUS THEME: Every Rout has a Silver Lining?

Silver volatility recently spiked to its highest level since 1980. After reaching an all-time high of $121.65/oz on January 29, the price of silver plummeted 26% the next day, marking the largest single-day decline. After a brief respite, silver dropped a further 20% on February 5. These drastic corrections coincided with a similar pullback in cryptocurrencies and other precious metals.

Like gold, spikes in silver volatility are usually a symptom of underlying market stress, as seen during the 2008 credit crisis and the 2020 pandemic (see chart below). However, unlike gold, which primarily serves as a store of value, silver is used as an essential input in a wide range of manufacturing processes. Additionally, for the same dollar value, storage costs are much higher for silver than for gold. Furthermore, the silver stockpile tends to be inelastic, as most of its supply is a byproduct of mining other base metals. In fact, demand has consistently outstripped supply since 2021. Consequently, silver has historically been more volatile than gold and is not classified by the IMF as a reserve asset.

Source: Bloomberg; XAGUSD 3 month at-the-money implied volatility

Some commentators point to the January 30 announcement of Fed Chair nominee Kevin Warsh, previously known as an inflation hawk, as the cause of the rout. However, we believe the latest bout of silver volatility has been fueled by a confluence of market factors — asset reallocation, animal spirits, and national strategy — that led to the severe price dislocations.

First, a buildup of geopolitical anxiety over the past year has bolstered the secular appeal of precious metals, an asset class long overlooked. Given stretched equity valuations, tech bubble fears, and weak-dollar expectations, strategic year-ahead allocations from both institutional and retail investors likely fueled the inordinate price gains in December and January.

Second, silver has drawn momentum-based flows. Surging leveraged plays in China have led to new price breaks during Asian hours. However, the market frenzy has unintended consequences. In the past week, a Shenzhen-listed silver futures fund suffered multiple trading halts as staggering inflows drove its premium well above its underlying assets.

Third, silver has emerged as a strategic resource for the modern economy. Its use has increased in the production of electric vehicles, solar panels, and consumer electronics. Similarly, AI data centers and defense supply chains have boosted silver consumption. Last November, the US declared silver a critical mineral. China has tightened restrictions on silver exports through the end of 2027.

In the longer term, a combination of industrial demand and supply bottlenecks should underpin silver prices. Nevertheless, from an investment perspective, our view is that silver will remain prone to boom-bust price swings, given its smaller market cap, the absence of a central bank bid, and the dominance of footloose investors. Accordingly, silver should be allocated only to high-risk portfolios and not treated as a safe-haven asset.

HEARD THROUGH THE GRAPEVINE

This week’s Heard Through the Grapevine reflects a market that looks stable on the surface but feels less certain underneath. Fewer recessions, greater policy intervention, and longer cycles have pushed asset prices higher, leaving less margin for error. That strain is starting to show in the dollar, in cross-border capital flows, and in how investors are reassessing concentrated exposure to US tech and AI. Add in a geopolitical backdrop that markets are largely discounting, and the common thread is not panic but growing sensitivity to credibility, diversification, and downside risk.

The Downside of Staving Off Recessions (Financial Times): Modern economies have experienced fewer recessions as governments and central banks have become more aggressive in stabilizing growth. That stability has come at a cost: it has encouraged excessive leverage, inflated asset prices, and weaker productivity, as inefficient firms are kept alive. The danger is that with debt already high and policy tools stretched, the next downturn may be harder to contain and more damaging when it arrives.

U.S. Dollar Rebound to Be Cut Short by Rate Cut Bets, Doubts Over Fed Independence (Reuters): A Reuters poll of FX strategists suggests the dollar’s recent rebound is temporary, with most expecting it to weaken again later this year as markets continue to price in US rate cuts and question Federal Reserve independence. Despite inflation remaining above target, investors largely expect easier policy under political pressure, which would push real yields lower and weigh on the dollar. Strategists see choppy trading in the near term and a gradual depreciation over the medium term, with net-short dollar positioning likely to persist.

Europe, Asia Lead Global Equity Fund Inflows as Investors Cut U.S. tech exposure (Reuters): Global equity funds attracted $31.5bn in inflows, led by Europe and Asia, as investors diversified away from volatile U.S. technology stocks. European equities saw their strongest demand since April as markets hit record highs, while tech funds experienced net outflows amid sector rotation. At the same time, investors increased allocations to bonds, money markets, and gold, signaling a broader shift toward diversification and risk management rather than outright risk-taking.

How to Hedge a Bubble, AI Edition (The Economist): As massive AI spending revives fears of a tech-led bubble, investors are seeking protection without sacrificing upside. Traditional hedges, such as government bonds, may no longer be effective if inflation or policy instability causes stocks and bonds to move in tandem. Options-based hedging can be costly and erode long-term returns. Historical evidence suggests that the most effective hedge may be to remain invested and shift toward lower-volatility, higher-quality equity strategies, rather than attempting to time an exit or relying on traditional safe havens.

China Warns US Arms Sales to Taiwan Could Threaten Trump Visit in April (Financial Times): The US is preparing a major new arms package for Taiwan, potentially worth up to $20bn, prompting Beijing to warn that the move could jeopardize a planned Trump–Xi meeting in April. US officials view the warning as a pressure tactic and cite long-standing legal obligations under the Taiwan Relations Act. China’s unusually blunt stance highlights rising tensions as Washington signals continued support for Taiwan’s defense.

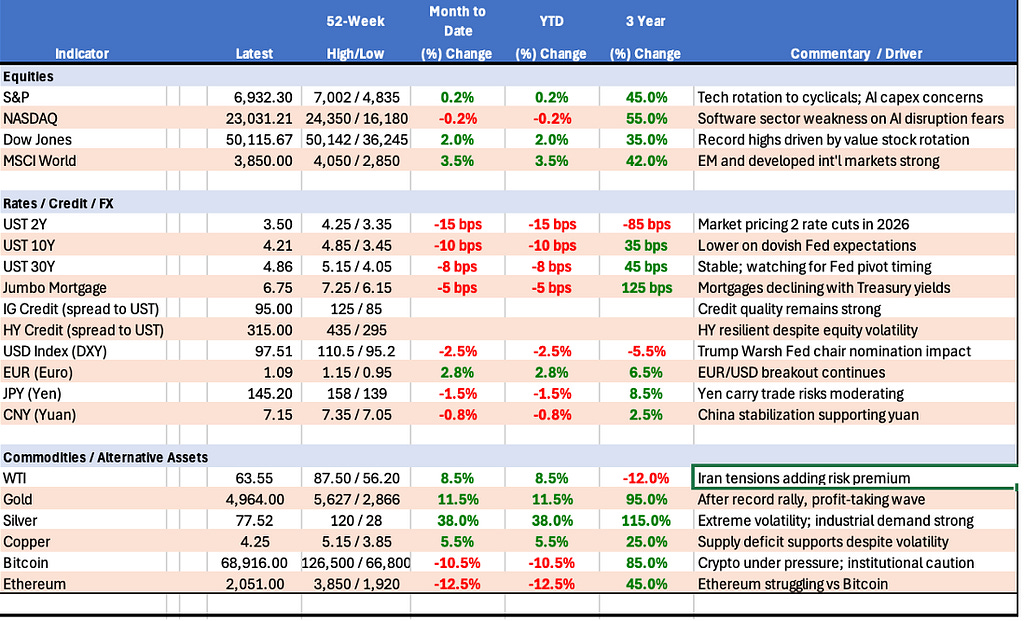

MARKET DASHBOARD

Thank you for reading CrossLight’s Weekly Perspectives. If you wish to talk through any of these themes, please reply to this note. This note is strictly for informational purposes only and does not constitute investment advice for the reader.