KEY TAKEAWAYS

• US growth stays close to trend, alongside stubborn inflation and sluggish job market

• Fed likely on hold through mid-year; avoid long-dated Treasuries

• Geopolitical risks poised to heat up; add time-tested safe haven assets like gold

MARKET RECAP

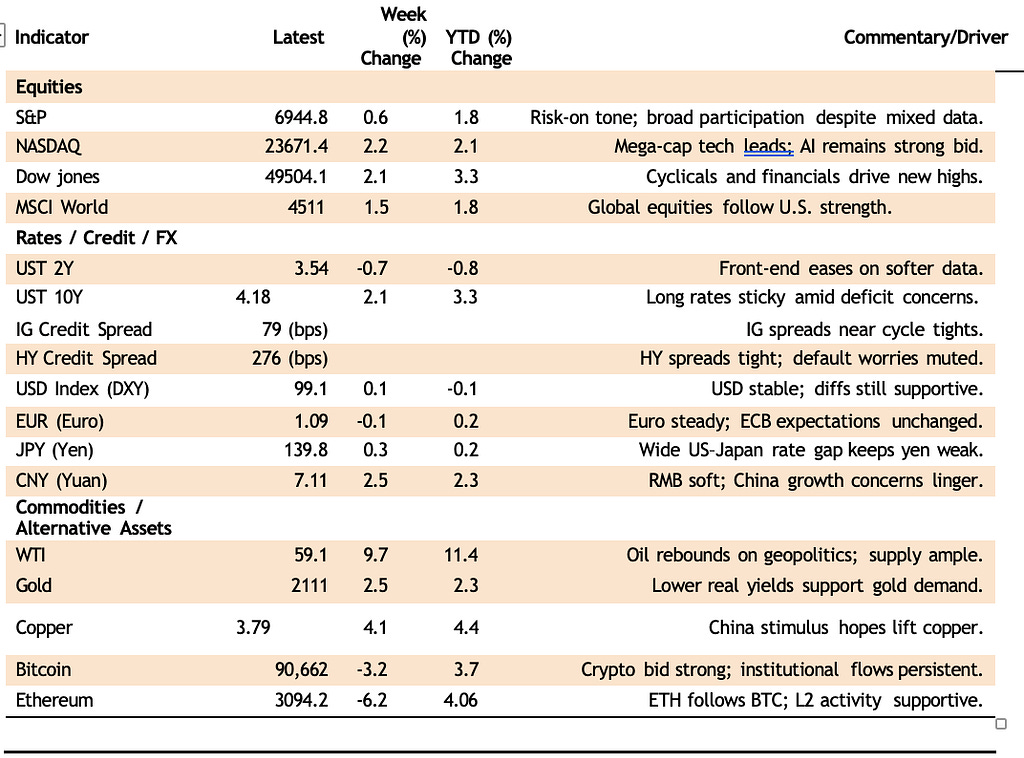

Global financial markets held firm in a week laden with headline-grabbing developments. In geopolitics, markets digested news of the US raid on Venezuela, with investor anxiety shifting to potential next-in-line targets (Greenland and Iran). On the domestic front, investors shrugged off a lackluster labor market report, even as the SCOTUS postponed its ruling on Liberation Day tariffs to mid-January. Meanwhile, in a bid to lower the cost of home ownership, President Trump proposed a ban on single-family home purchases by large institutional investors and directed Fannie Mae and Freddie Mac to purchase $200 billion in mortgage bonds. Separately, the White House announced plans to withdraw from 66 international organizations, of which 31 are UN entities. Elsewhere, a majority of EU member states endorsed an extensive trade deal with Mercusor (a South American trade bloc led by Argentina currently), despite opposition from France and Poland.

In terms of market performance, global equities rose 2%, while the US dollar advanced on diminished hopes of near-term rate cuts. Crude oil advanced 2.5% on abating fears of an imminent supply glut; ExxonMobil’s statement that Venezuela remains “uninvestable” underscores business skepticism. After last year’s blockbuster performance, precious metals overcame the recently imposed increase in margin requirements by the Chicago Mercantile Exchange to extend their outperformance. Silver, platinum and palladium posted double-digit year-to-date gains.

LOOKING AHEAD THIS WEEK

This week’s data focus centers on Tuesday’s release of the December CPI (consensus 2.7%). A declining but sticky print that remains above the Fed’s inflation target of 2% likely points to a pause in rate cut through Q2 2026. The SCOTUS verdict on tariffs could be released before the end of this week. According to Treasury Secretary Scott Bessent, President Trump may announce his choice of the new Fed chair before he leaves for Davos to attend the January 19 -23 World Economic Forum. Geopolitics remains a near-term focal point, given President Trump’s latest remarks regarding Greenland and Iran. With Venezuelan opposition leader Maria Corina Machado scheduled to meet President Trump in Washington, D.C., later this week, the outcome could throw a wrench into the works for the newly installed Rodriguez team.

FOCUS THEME: Flashing Amber on Greenland

Following a successful US military operation in Venezuela on January 3, President Trump has ramped up rhetoric over other Western Hemisphere territories. Greenland, a semi-autonomous Danish territory about three times the size of Texas, now appears to be a top priority. Various US officials have cited national security as the key reason, given Greenland’s strategic importance for aerial and maritime approaches to the Arctic.

To be sure, US interest in Greenland is not new. In 1946, Denmark turned down President Harry Truman’s offer of $100 million in gold. During President Trump’s first term in 2019, he had likened it to “a large real estate deal.” Over the last twelve months, the Trump administration has revived its acquisition efforts. In March 2025, Vice President JD Vance made a brief stop at a US Space Base in Pituffik. Last month, President Trump appointed a special envoy to Greenland. Most recently, the White House is reportedly considering a $100,000 cash offer per Greenlander to sweeten the annexation deal.

Across the Atlantic, European leaders have joined Denmark in a diplomatic pushback against an American takeover. A joint statement on January 6 made clear that “it is for Denmark and Greenland, and them only, to decide on matters concerning Denmark and Greenland.” According to a January 2025 survey, 85% of Greenlanders oppose joining the US.

Rather paradoxically, the American footprint in Greenland has dramatically shrunk in the post-Cold War years, from a peak of 17 military bases with 10,000 troops to just one, presently in Pituffik, with 150 personnel. Importantly, under a 1951 defense pact with Denmark, the US retains extensive rights in military operations in Greenland.

Beyond national security, the strategic access to the largely untapped natural resources in Greenland is likely behind American interest. These include rare-earth elements, which are essential to modern technology, as well as hydrocarbons.

Crucially, a US military operation (“always an option”, according to the White House) will likely spell an end to the post-WWII Western alliance. Under Article 5 of the NATO treaty, Denmark would expect NATO’s collective defense mechanism to activate against the aggressor, which, ironically, is a founding member of the alliance. Europe would thus be confronted with the choice of defending the rules-based order or acquiescing to concessions made for the most powerful member of the alliance. Neither scenario bodes well for global stability.

From an investment viewpoint, elevated geopolitical risks will continue to underpin the outperformance of precious metals, particularly gold. Consider exposure to European defense-related ETFs, such as EUAD, as NATO fragility will likely spur increased military spending to deter Russian aggression.

HEARD THROUGH THE GRAPEVINE

Global equity markets rally despite macro crosswinds — Major U.S. equity benchmarks climbed sharply, with the Dow surpassing 49,000 and broad sector participation, reflecting investor optimism amid mixed economic data and geopolitical risk. The rally hints at continued risk appetite and confidence in early 2026 growth prospects, though analysts caution that high expectations may be vulnerable to economic disappointments. (Wall Street Journal)

Weak U.S. jobs data dims hopes for immediate Fed rate cuts — December payrolls missed expectations by a wide margin, marking the weakest job growth since the pandemic and reducing the odds of near-term rate cuts. Softer labor trends and downward revisions add uncertainty to the macro-outlook. (The Guardian)

Yellen Warns of Growing ‘Fiscal Dominance’ Threat to US Economy -Economists warn rising U.S. debt risks “fiscal dominance,” where the Fed cuts rates to fund Treasury deficits rather than fight inflation. With a $1.9tn trillion deficit and debt approaching 118% of GDP, panelists see pressure for cuts and little appetite for reform, raising the odds of a future fiscal crisis. (Bloomberg)

Trump Calls for One-Year Cap on Credit Card Rates at 10% — Trump proposed a one-year 10% cap on credit-card rates as an affordability measure, but offered no enforcement mechanism. Banks warn such a cap would restrict unsecured credit, push borrowers to shadow lenders, and shrink rewards programs. Notably, populists on both the left (Sanders) and right (Hawley) have signaled support, suggesting rate-cap politics are moving toward the center of the 2026 campaign debate. (Bloomberg)

Welfare Grift From Minnesota to Mississippi — Republican-led hearings on welfare fraud in Minnesota and Mississippi have highlighted deep abuses in federal safety-net programs. The Editorial Board argues that outrage should translate into durable policy reform, not performative oversight.

Beyond exposing misuse of TANF funds, the piece urges structural changes — counting all benefits as income for eligibility, converting programs into block grants to improve state accountability, and conditioning benefits on work or rehabilitation — to realign incentives and curb wasteful spending.

Political theater risks eclipsing the need to fix the system’s perverse incentives. (WSJ)

In Donald Trump’s world, the strong take what they can — Trump’s seizure of Nicolás Maduro showcased raw American hard power and a new hemispheric doctrine rooted in resources and coercion rather than democracy. But it also revealed limits: Maduro’s apparatus remains intact, Venezuela is ungovernable from afar, and oil companies show little interest in a 19th-century imperial project in a 21st-century market. The bigger risk is systemic: bullying neighbors without a values-based attractor pushes countries toward China and Russia, erodes U.S. alliance credibility, and nudges the region toward spheres of influence that ultimately weaken rather than consolidate American power. (The Economist)

How Donald Trump Could Take Control of Greenland — Trump’s advisers are exploring ways for the

U.S. to gain major influence or even control over Greenland, from expanding military basing rights to a Compact of Free Association that shifts sovereignty without “buying” the island. Danish officials worry Washington is quietly encouraging Greenlandic independence to create that opening, while U.S. officials say a U.S. security umbrella is needed to block Chinese and Russian leverage in the Arctic. The tail risk — acquisition by force — is militarily trivial but would blow up NATO and the post-WWII European security order, which is why Copenhagen is seeking a face-saving off-ramp that preserves sovereignty. (Financial Times)

The Ayatollah’s Regime Is Crumbling — Iran is facing its most sustained nationwide protests in years as currency collapse, shortages, and state-capacity breakdown accelerate. Analysts argue there is no plausible scenario in which the Islamic Republic reaches 2026 with power intact. The piece outlines three endgames — collapse, military strongman, or muddling through — all of which leave the regime weaker, fragmented, and more dangerous externally due to residual missile, nuclear, and proxy capabilities. Bottom line: Iran’s crisis has shifted from episodic unrest to systemic state f ailure. (The Free Press)

Can the ‘Donroe Doctrine’ Make South America Better Off? — Trump’s Venezuela intervention signals a shift from U.S. soft power to hard power in Latin America. Though the region’s struggles are primarily domestic, this coercive approach risks fueling anti-American politics and driving governments toward China even as it creates openings for reform. The central question is whether U.S. strategy will embrace partnership and market-building or return to extraction and coercion. (The Free Press)

Venezuela presents a big headache for big oil — Trump’s Monroe-Doctrine-style push for U.S. majors to rebuild Venezuela’s oil sector runs into the reality that today’s supermajors are capital-disciplined, risk-averse, and not in the business of subsidizing geopolitical projects. With crude prices soft, demand possibly peaking this decade, and Guyana offering far lower breakevens, Venezuela’s heavy sour barrels — break-even above $80 with large upfront capex — screen poorly for shareholders. The broader point: unlike the 1950s, the White House can’t will a petrodollar revival without legal, contractual, and security guarantees; capital will otherwise flow to jurisdictions that are easier to underwrite. (The Economist)

How Rubio Won — Marco Rubio has emerged as the most influential figure in Trump’s second-term foreign policy apparatus, consolidating an unusually broad portfolio — State, National Security Advisor, USAID (now shuttered), and effectively Venezuela — through competence, loyalty, and strategic alignment rather than ideological grandstanding. Once overshadowed by VP J.D. Vance and MAGA’s isolationist wing, Rubio has repositioned himself as a hawkish realist who matches Trump’s willingness to use hard power without committing to open-ended nation-building, a stance that has proven decisive in the Venezuela operation. The piece frames Rubio as the second-most-powerful man in Washington and a likely kingmaker for 2028, not by opposing Trumpism but by adapting to it. (The Free Press)

MARKET DASHBOARD*

Thank you for reading CrossLight’s Weekly Perspectives. If you wish to talk through any of these themes, please reply to this note. This note is for informational purposes only and is not an investment advice or a recommendation to buy or sell any sec