KEY TAKEAWAYS

● Global growth prospects remain sanguine, despite elevated geopolitical risks

● Debt sustainability concerns around the world are fuelling bond vigilantes’ activity

● Technical shifts in investor positionings could exert influence on asset prices

MARKET RECAP

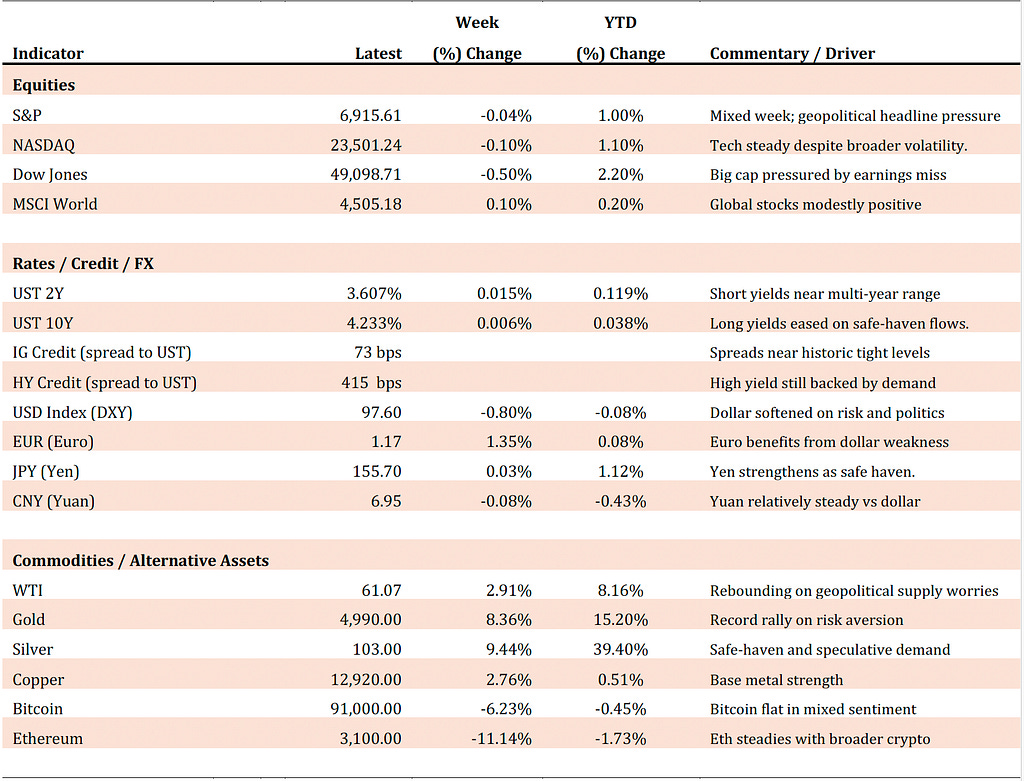

Global markets finished mixed amid geopolitical tensions.

● Precious metals continued their blistering rally, with silver surpassing $100/oz for the first time. Poland’s central bank approved an additional purchase of 150 tonnes of gold, targeting a 28% increase over its current holding of 543 tonnes.

● Crude and energy also posted remarkable gains. Natural gas soared over +60% from a week ago in response to this weekend’s extreme winter storm.

● In FX, the week’s theme was broad-based weakness in the US dollar, except for the Indian rupee, which depreciated to a new low of 92 against the greenback. The Japanese yen advanced +1.7% on Friday to its strongest level in a month, on market speculation of a possible joint intervention between Japan’s Finance Ministry and the New York Fed.

● In equities, US stocks partially recouped early losses, while Europe underperformed. Stock indices in Brazil, Colombia, South Korea, and Taiwan reached new highs.

● In fixed-income markets, the 10-year Treasury yield briefly touched a 5-month high of 4.30% on news of Danish Pension’s divestment of $100 million in Treasury bonds, before stabilizing to close the week at 4.23%. Japan had a “Liz Truss” moment last Tuesday as markets reacted to proposed fiscal expansion plans. The 30-year government bond yield spiked 27 bps to an all-time high of 3.92% in a single day, before retracing to finish the week 14 bps higher.

LOOKING AHEAD THIS WEEK

The Fed is expected to keep the policy rate unchanged at 3.75% at this Wednesday’s FOMC meeting. Market attention will be on Fed Chair Jerome Powell’s press briefing, his first public address since the DOJ’s subpoenas earlier this month. President Trump’s choice for the new Fed Chair continues to hold market participants in suspense, as BlackRock executive Rick Rieder recently leapfrogged other contenders to be the top candidate.

On geopolitics, news reports of US naval vessels being dispatched from Asia to the Middle East, alongside a decision by a slew of commercial airlines to suspend flights to the Gulf, have fuelled speculation of a possible military operation against Iran. Keep an eye on market reaction following President Trump’s threat yesterday to impose a 100% tariff on all Canadian exports to the US should the China-Canada trade deal take effect on March 1, 2026.

FOCUS THEME: From Multilateralism to Plurilateralism

Plurilateralism refers to subsets of countries forming bespoke trade agreements rather than broad multilateral pacts.

In mid-January, two transpacific bilateral trade agreements presented a stark contrast to a tariff spat across the Atlantic. First, the US pledged to lower tariffs on goods from Taiwan in exchange for new US tech investments. Second, in a reset of strategic partnership, Canada committed to slashing import tariffs on Chinese electric vehicles, while China will resume inbound shipments of canola and add Canada to its list of nearly 50 countries for visa-free entry. Meanwhile, the US announced new tariffs of up to 25% on eight NATO partners, but rescinded the plan just days later, purportedly after both sides agreed to a Greenland framework.

To be sure, trade and politics have always been inextricably intertwined. In the 1990s, the end of the Cold War and the imminent rise of China as an economic powerhouse provided fresh impetus for global cooperation. By contrast, recent developments are part of a proliferation of customized trade accords outside a rules-based multilateral system, which has come under severe strain due to shifting geopolitics, rising nationalism, and the WTO’s institutional limitations.

Nostalgia aside, the post-WWII record of multilateralism is not as robust as widely believed. The GATT, the predecessor of the WTO, existed only as a provisional treaty on goods trade. Instead, collective partnerships began in the neighborhood, underscored by the inception of the EEC (1957) in Europe, ASEAN (1967) in Southeast Asia, Mercosur (1991) in South America, as well as the US-Canada FTA (1989) and NAFTA (1994) in North America. Crucially, FTAs do not imply zero tariffs. Rather, they seek to establish predictable import barriers, with members committing to reducing them over time. FTAs, therefore, are meant to be contractually binding in spirit and letter.

Going forward, the surgical rewiring of trade linkages is likely to push global trade toward plurilateralism, in which overlapping subsets of countries commit to bespoke trade arrangements. In this regard, a few market and economic observations are worth noting.

First, the trend of expanding and diversifying trade partnerships to mitigate the risk of market access will likely continue. This is especially true for small, open economies that have less political clout in bilateral negotiations and are therefore more vulnerable to hegemonic interests.

Second, an emerging patchwork of operating ecosystems for cross-border trade could facilitate the coexistence of multiple currencies as mediums of exchange. In fact, virtually all bilateral trade between China and Russia is now invoiced in either of the two countries' currencies.

Third, trade disputes and diplomatic rows could trigger retaliatory responses through portfolio capital flows. The spat over Greenland has prompted a Danish pension operator to sell its Treasury holdings, while a Greenland pension is reportedly considering divesting US equities.

Fourth, the reshoring of manufacturing production, particularly in technologically sensitive industries, reverses the decades-long trend of offshoring to take advantage of lower costs. All else equal, the structural inflationary impulse could prove sticky over the long term.

HEARD THROUGH THE GRAPEVINE

Gold Records Best Week Since 2008 as Greenland Crisis Rattles Dollar — Gold surged nearly 8%, and silver broke above $100/oz as the Greenland standoff and tariff threats triggered a flight from the dollar into safe havens, producing gold’s strongest weekly gain since the 2008 crisis and the dollar’s weakest week since May. Investors and central banks have already been diversifying away from U.S. assets, but the crisis has accelerated concerns about political risk, policy reliability, and the dollar’s institutional credibility. Strategists say the episode strengthens the case for continued dollar hedging and depreciation as the Fed cuts rates and global investors seek alternatives. (FT)

US Investment-Grade Credit Spreads Reach Lowest Level This Century — Investment-grade credit spreads tightened to just 73 bps over Treasuries — the lowest since 1998 — as investors aggressively bought high-quality corporate bonds despite volatility triggered by Trump’s tariff threats. Strong demand reflects a preference for “all-in yield” at higher rates, as well as the view that blue-chip corporate credit now looks comparatively safer than U.S. government debt amid political uncertainty. Issuance has surged to its fastest start since 2020, underscoring how little macro drama is disrupting credit markets. (FT)

Business Activity Picks Up in Parts of Europe and Asia — Global PMIs showed early-year momentum, with business activity accelerating in India, Japan, Australia, and parts of the eurozone as export orders stabilized after last year’s tariff shock. The IMF and World Bank have raised growth forecasts on the back of U.S. AI-driven investment, though both warn the rebound remains fragile and tariff-sensitive. Europe continues to lag the U.S. and China, while U.S. firms reported the sharpest drop in overseas orders since Trump’s tariff escalation. (WSJ)

Niall Ferguson: How Trump Won Davos — Ferguson argues that, contrary to European claims, Trump backed down over Greenland. He also argues that Trump “won Davos” by dominating the agenda, shaping the narrative, and using the forced Greenland issue as deliberate misdirection. He suggests Trump never intended to annex Greenland or impose new tariffs, but used the threat-bluff to divert European attention from U.S. plans in the Middle East and Ukraine. The episode reflects a shift toward hard-power realism — “the strong do what they can, the weak suffer what they must” — with Trump using maskirovka to keep counterparts off balance. (The Free Press)

Trump Threatens 100% Tariffs on Canada if It Seals Trade Deal With China

After Canada resolved trade barriers with China over EVs and canola, Trump warned Ottawa that it would face deeper economic ties with Beijing — accusing Canada of becoming a conduit for Chinese products into the U.S. and threatening tariffs on “all Canadian goods” if it pursued a duty-free path. The threat fits Trump’s pattern of late-night tariff salvos followed by walk-backs and comes amid U.S. use of North America to skirt U.S. levies under USMCA. Ottawa denies that a review of the China free-trade deal is underway, but business leaders warn the dispute risks spilling into the USMCA review and broader U.S.–Canada relations. (FT)

A Chilling, Yet Plausible Scenario: What If Putin Wins? — German strategist Carlo Masala sketches a scenario in which a forced ceasefire in Ukraine and a U.S. pivot to Asia allow Russia to regroup, rearm, and later test NATO by seizing a small Estonian city — calculating that Western leaders will avoid escalation and thus hollow out Article 5. The scenario underscores how political fatigue, populism, and U.S. unpredictability could erode deterrence faster than battlefield outcomes. The broader warning: if Europe doesn’t invest in its own defense, adversaries may conclude the West no longer defends its interests. (The Economist)

The Medicare Charge That’s Taking a Bigger Bite Out of Social Security Checks — Rising Medicare Part B and D premiums — especially IRMAA surcharges — are offsetting Social Security COLAs for higher-earning retirees, with IRMAA projected to rise ~30% between 2026–2030. Because premiums track medical costs, not inflation, net benefits can fall even as COLAs rise. IRMAA thresholds are steep, retroactive to income from two years prior, and offer limited mitigation via MAGI management or qualifying-life-event refunds. (WSJ)

Why Fentanyl Deaths Are Falling — After driving overdose deaths to a historic peak, fentanyl-related fatalities have declined more than 20–30 percent since mid-2023 due to widespread availability of Narcan, declining fentanyl purity, and the introduction of adulterants that dilute potency. Demand-side factors — fewer new users, “saturation” among existing users, and a grim survivor effect — have also contributed to fewer overdoses. Experts caution the trend may not persist, as treatment rates remain low and the market could shift toward even more potent synthetics. (The Free Press)

MARKET DASHBOARD*

Thank you for reading CrossLight’s Weekly Perspectives. If you wish to talk through any of these themes, please reply to this note. This note is strictly for informational purposes only, and does not constitute investment advice for the reader.