Crosslight Weekly Perspecitve - June 7, 2026

An Air Pocket on a Clear Day

# An Air Pocket on a Clear Day

*A blockbuster jobs report sent stocks, bonds, gold, and Bitcoin falling together. Plus the contrarian case for the world’s cheapest safe haven, the Japanese yen.*

---

---

A pilot will tell you the most unsettling moment in a flight is not the storm you can see building on the horizon. It is the air pocket on a clear day, the sudden drop when nothing on the instruments looked wrong. Markets hit one of those last Friday. The trigger was not a crisis or a scandal. It was good news. American employers added far more jobs in May than anyone expected, and a strong economy is supposed to be exactly what everyone wants. Last week it was what sent stocks, bonds, gold, and crypto tumbling together.

## MARKET RECAP: Hitting an Air Pocket

Here is how good news does that. The May jobs report showed employers added 172,000 workers, nearly double the 88,000 economists had penciled in. A strong job market gives the Federal Reserve little reason to cut interest rates and a fresh reason to raise them, and higher rates are the one thing this market cannot stand. The moment traders did the math, the interest rate the US government pays to borrow for ten years, the number that quietly sets the cost of mortgages, car loans, and company debt, jumped sharply in a single day. When borrowing gets more expensive that fast, everything bought with cheap money is suddenly worth less. The hardest hit were the things that pay their owners nothing to hold them: technology shares riding the promise of artificial intelligence, gold, and Bitcoin. Once a safe government bond starts paying you more, anything that pays you nothing looks worse by the hour.

The rest of the week told the same story. Two widely watched surveys of American business, one covering factories and one covering the service companies where most people work, both came in stronger than expected. A report from the Bipartisan Policy Center in Washington warned that the federal government will likely hit its $41.1 trillion borrowing limit sometime between late winter and the middle of 2027. And the standoff between the United States and Iran kept traders on edge about oil prices, and about whether inflation will fade or dig in. Put it together and the mood around the Fed flipped: investors now see a better than even chance of a rate increase as soon as October. A year that began with talk of rate cuts is now braced for the opposite.

**Key Takeaways**

- Good news turned into bad news. A strong jobs report convinced investors the Fed will not cut rates this year, and might raise them.

- When borrowing costs jump, the things that pay no income, technology shares, gold, and Bitcoin, fall together.

- This week’s government bond sales and the SpaceX market debut will show whether buyers are ready to step back in after the drop.

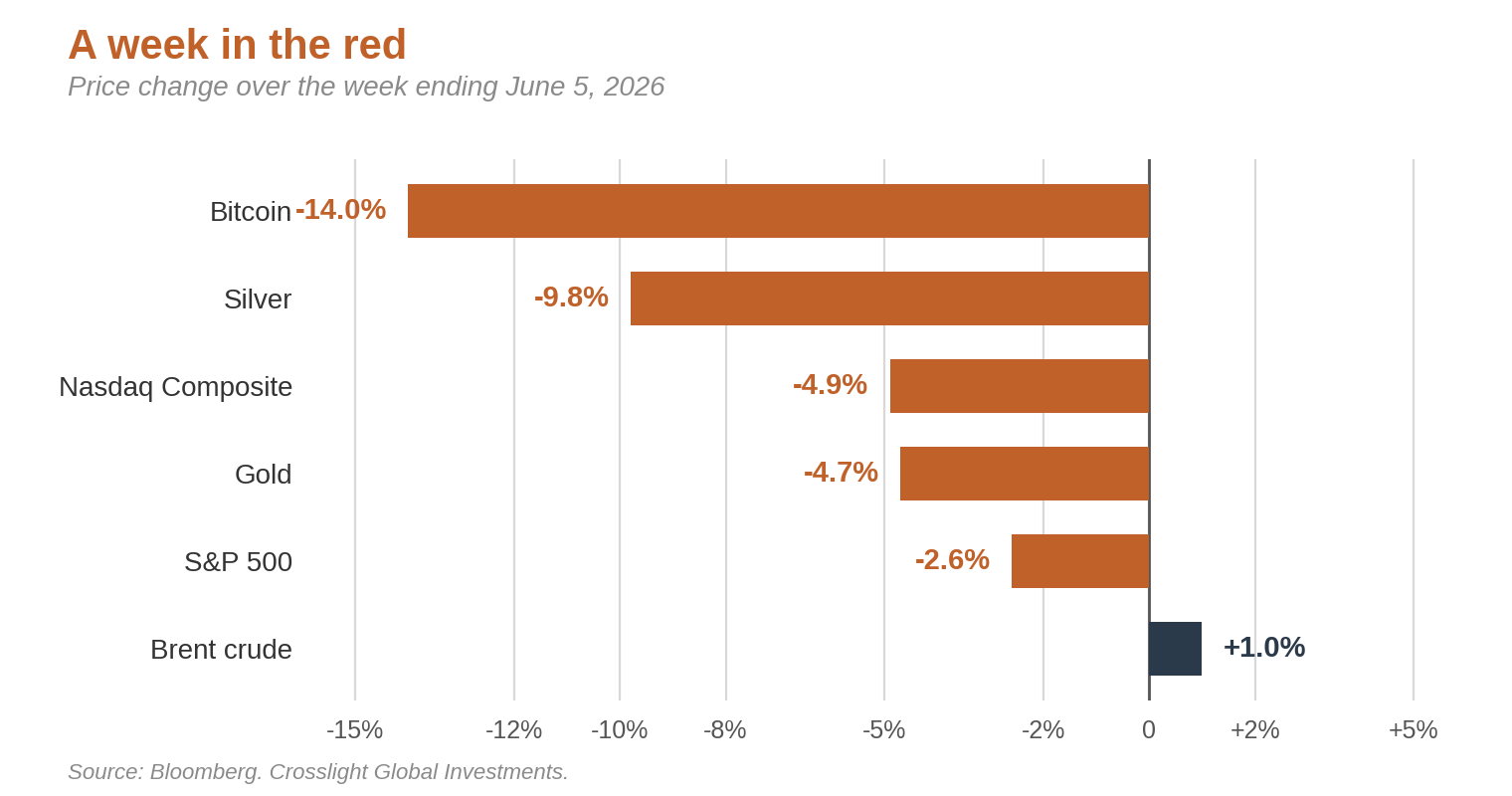

**Stocks.** The technology-heavy Nasdaq index fell almost 5% on the week, its worst stretch since the tariff shock of April 2025. The broader S&P 500 held up better, down 2.6%, helped by gains in energy and healthcare that offset the damage in tech. The worst performer abroad was Indonesia, where the main market dropped 8.7% to its lowest level since November 2020, as foreign investors pulled their money out and the country’s finances looked increasingly shaky.

**Bonds.** Government bonds had a rough week, and short-term ones fared worse than long-term ones. That is unusual, and it tells you the market is worried about the Fed’s next few moves rather than the distant future. The interest rate on the two-year US government bond, the one most sensitive to Fed decisions, rose to 4.15%, the highest in fifteen months. (When a bond’s interest rate goes up, the bond itself is worth less, so anyone already holding it loses money.) Developing economies fared worse still: the rates Brazil and South Africa must pay to borrow for ten years climbed to 14.9% and 8.9%.

**Currencies.** The US dollar rose as jittery investors looked for somewhere safe to park money, which is what usually happens in a nervous week. The currencies that move most with the global mood took the biggest hits, with the South Korean won and the New Zealand dollar each down more than 3%. The Japanese yen, despite repeated government efforts to prop it up, stayed stuck near 160 to the dollar, the subject of this week’s focus theme. The one winner was the Indian rupee, which held its ground after India’s central bank opened its bond market a little wider to foreign money.

**Commodities and crypto.** A brutal week for anything that pays no income while you hold it. Brent crude oil edged up about 1% after the previous week’s slide, but it was a lonely gain. Precious metals were hammered by the stronger dollar and the prospect of higher rates: silver fell nearly 10%, and gold dropped 4.7%, wiping out almost all of its gains for the year. Bitcoin was the biggest casualty, down 14% to just above $60,000, less than half the record $126,200 it hit only eight months ago.

## LOOKING AHEAD THIS WEEK

**The inflation tests.** Two American price reports will set the tone. On Wednesday, the cost of living is expected to come in more than 4% higher than a year ago, the first time it has crossed that line in three years, and an awkward number for a Fed already leaning toward higher rates. Thursday brings the prices businesses charge one another, which eventually flow through to store shelves and may reach a post-pandemic high. On Friday, the University of Michigan’s survey of how Americans feel about the economy is expected to tick up to 46.0 in June, a small bounce from May’s record low of 44.8 but still gloomy. The pattern to watch is the one that keeps repeating: prices up, mood down.

**What China is signaling.** China is expected to report on Tuesday that its trade surplus, the gap between what it sells abroad and what it buys, grew to a four-month high of $92.6 billion in May, with its own inflation figures due Wednesday. For an American investor, what matters is what these numbers say about global demand and the health of the supply chains that run through Asia.

**Central banks pulling apart.** The big event is Thursday’s European Central Bank meeting, where officials are expected to raise interest rates for the first time this cycle, a small step up to 2.25%. The same day, Turkey’s central bank is likely to leave its main rate at a steep 37%, though its unusual methods for defending its currency will draw fresh scrutiny. On Wednesday, Canada’s central bank is expected to hold steady while hinting it could tighten later. The thread we keep pulling holds: the world’s central banks no longer move together, and the daylight between them is where the opportunities in currencies tend to open up.

**The bond sales that matter.** After last week’s drop, the government’s regular sales of new debt, this time 3-, 10-, 20-, and 30-year bonds, turn into a genuine test of nerve. A weak showing would mean buyers are demanding higher interest to lend to Washington, which would push up borrowing costs for everyone. A strong one would settle things down.

**A rocket goes public.** SpaceX is expected to set its share price on Thursday and start trading Friday, one of the most anticipated stock-market debuts in years. It should join the Nasdaq-100 index within about two weeks, though it must trade for a full year before it can enter the S&P 500. In a nervous market, the warmth of its welcome will say a lot about how much risk investors still have the stomach for.

## FOCUS THEME: Yen for Strength

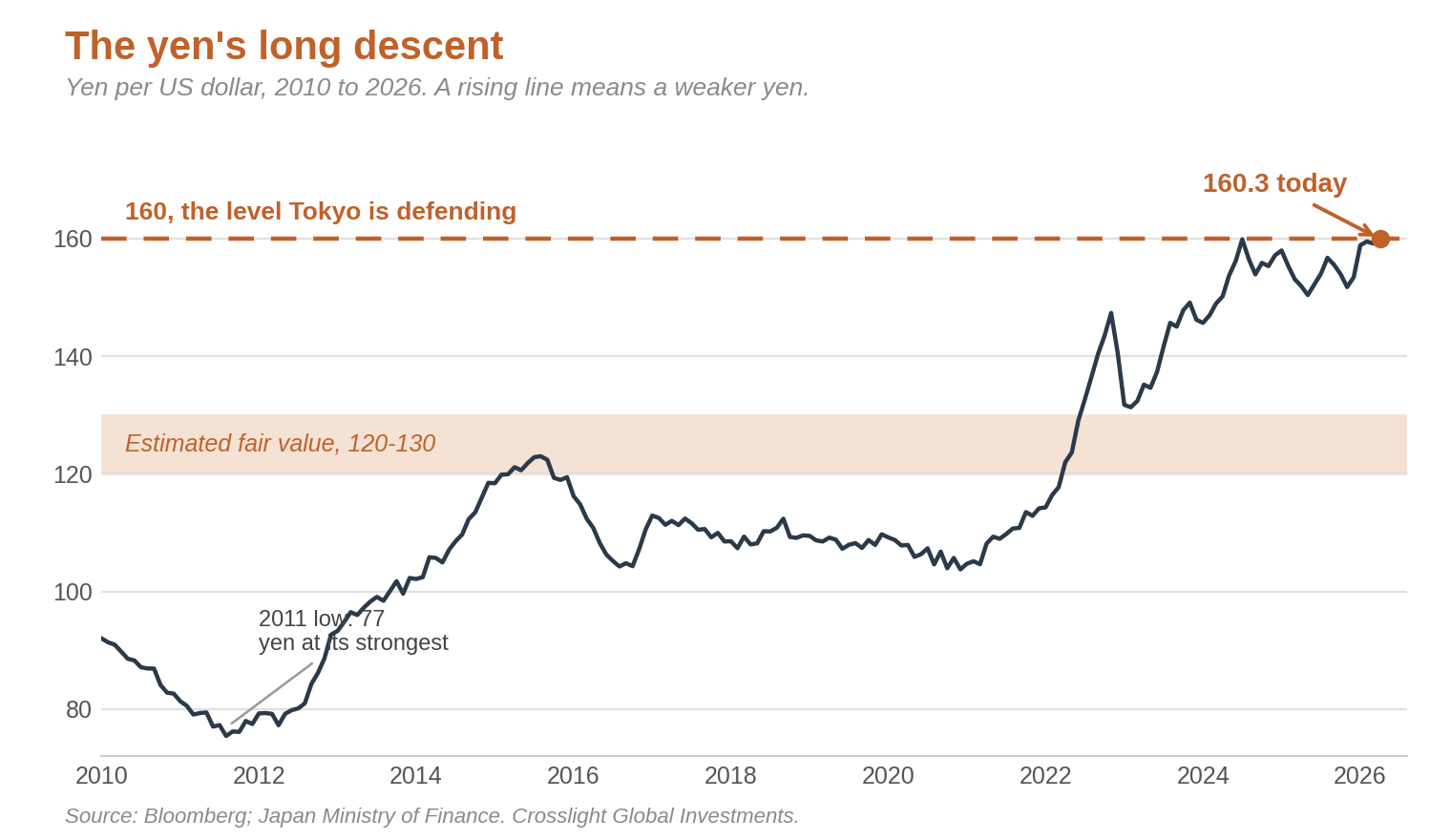

When fear sweeps through markets, the Japanese yen is supposed to rise. For decades it was the world’s reliable safe haven, the currency investors ran to when everything else looked dangerous. Last Friday, as global markets sold off, the yen did the opposite. It weakened, finishing the week near 160 to the dollar, roughly its lowest level in 34 years.

That reaction breaks an old rule. The rule held for a simple reason. For years, investors borrowed yen almost for free, thanks to Japan’s rock-bottom interest rates, and used the money to buy investments that paid more elsewhere. The move even had a name: the carry trade. When markets turned ugly, those investors had to sell what they owned and buy back yen to repay what they had borrowed, and the scramble to buy sent the yen shooting up. The clearest example came after the Tōhoku earthquake and tsunami in March 2011, when the yen jumped about 8% in the days after the disaster as money rushed home, even as Japan reeled.

So why is the safe-haven currency now stuck at a generational low? The answer is a tidy piece of economics with a name: the impossible trinity. In plain terms, a country can have two of three things, but never all three at once. It can hold its currency steady. It can let money move freely in and out across its borders. And it can set interest rates to suit its own economy. Pick any two, and the third has to give. Japan, which wants open borders for money and rock-bottom rates at home, has let its currency be the thing that gives.

For most of the past decade, that was a deliberate choice. Japan was fighting falling prices and carrying one of the largest government debt loads in the world, so keeping interest rates on the floor mattered more than a strong currency. To pull it off, the Bank of Japan reached for tools unusual enough to come with their own initials. It set interest rates at zero, then below zero, which meant banks were effectively charged to leave their money at the central bank. It also bought so many government bonds that it now owns close to half of all the debt Japan has ever issued. That spending spree did not come free. The bill shows up as a weak yen.

This is starting to change, but slowly. Since early 2024 the Bank of Japan has nudged its interest rate up four times, from below zero to 0.75%, and another small increase, to 1%, looks all but certain at its meeting on June 16. The problem is how far behind it remains. Even at 1%, Japan’s rate sits well below America’s 3.75% and Europe’s 2.25%. For comparison, the US Federal Reserve raised rates eleven times between 2022 and 2023, all the way to 5.50%, and Japan did not even start until eight months after the Fed had finished. And once you allow for Japan’s own inflation, lending money to the country still leaves you behind. As long as that gap stays this wide, money keeps draining out of yen and into currencies that pay more.

Tokyo is not sitting still. Between late April and late May, Japan’s finance ministry spent ¥11.7 trillion, about $73.5 billion, buying its own currency to slow the slide, the largest such effort on record. Since 2022 these rescues have cost more than $200 billion. The finance minister, Satsuki Katayama, has said the yen’s fair value is somewhere around 120 to 130 to the dollar, and the standard economic models agree the currency is far too cheap. Yet it keeps drifting back toward 160.

We see three reasons to favor the yen at today’s level. First, the government has made plain it will defend the 160 line, which makes this a lopsided bet: there is little room for the yen to fall much further, and real room for it to recover. Second, as Japan keeps raising rates while others eventually cut, the gap that has hurt the yen should slowly close. Third, Japanese companies are bringing profits and production back home, especially in industries tied to national security, a quiet but steady source of demand for the currency.

There is a price for all this. Japan’s foreign reserves fell by a record $77 billion in May. But with $1.3 trillion still on hand, Tokyo has plenty of room to keep playing this out on its own terms. For a patient investor, a currency this cheap, defended this firmly, by a country this able to defend it, is the kind of setup that usually rewards waiting.

## HEARD THROUGH THE GRAPEVINE

**The tide goes out on crypto.** Bitcoin’s 14% fall last week, to just above $60,000, is worth pausing on. Only eight months ago it traded at $126,200. Something that pays no dividend and no interest is worth exactly what the next person will pay for it, and that willingness dries up fast when a safe government bond suddenly pays more than 4% to do nothing. This is the same force, dressed up in louder clothing, that knocked gold and technology shares down last week. When money gets more expensive, the assets that promise the most and pay out the least are the first to crack. Crypto is just where you can watch it happen most clearly.

**A rocket the market can buy.** SpaceX’s stock-market debut this week will be a spectacle, and also a test. Most of the year’s hottest new listings arrived into rising markets that were hungry for a good story. This one shows up right after the worst week for stocks since last spring’s tariff scare. If investors pile in anyway, it tells us the appetite for a great story still beats caution. If the welcome is cool, it will be the clearest sign yet that higher interest rates are finally making investors pickier about what they will pay up for. Either way, a company famous for landing rockets will be telling us something about the ground.

---

*Thank you for reading CrossLight’s Weekly Perspectives. If you wish to talk through any of these themes, please reply to this note. This note is strictly for informational purposes only and does not constitute investment advice for the reader.*

**Sources**

Bloomberg; US Bureau of Labor Statistics May employment report; Institute for Supply Management manufacturing and services surveys; Bipartisan Policy Center debt limit projection; Federal Reserve; Bank of Japan; European Central Bank; Bank of Canada; Central Bank of the Republic of Turkey; Reserve Bank of India; Japan Ministry of Finance intervention and foreign reserve data; University of Michigan Surveys of Consumers; China General Administration of Customs; Moody’s, S&P Global, and Fitch; Reuters; Financial Times; The Wall Street Journal; CNBC; National Gallery of Art (William Hogarth, “An Emblematical Print on the South Sea Scheme,” 1721; public domain).

*Copyright © 2026 CrossLight Global. All rights reserved.*