Crosslight Weekly Perspective - February 22, 2026

Growth Is No Longer Moving in Lockstep: US exceptionalism topped the G7 again — but Q4 cracks are showing as Asia surges. Why desynchronized growth makes geography matter again.

### KEY TAKEAWAYS

- Ambiguity in the US tariff policy could restrain the economic outlook

- Cyclical trajectories globally are less synchronized due to trade fractures

- Incipient private market dislocations warrant monitoring

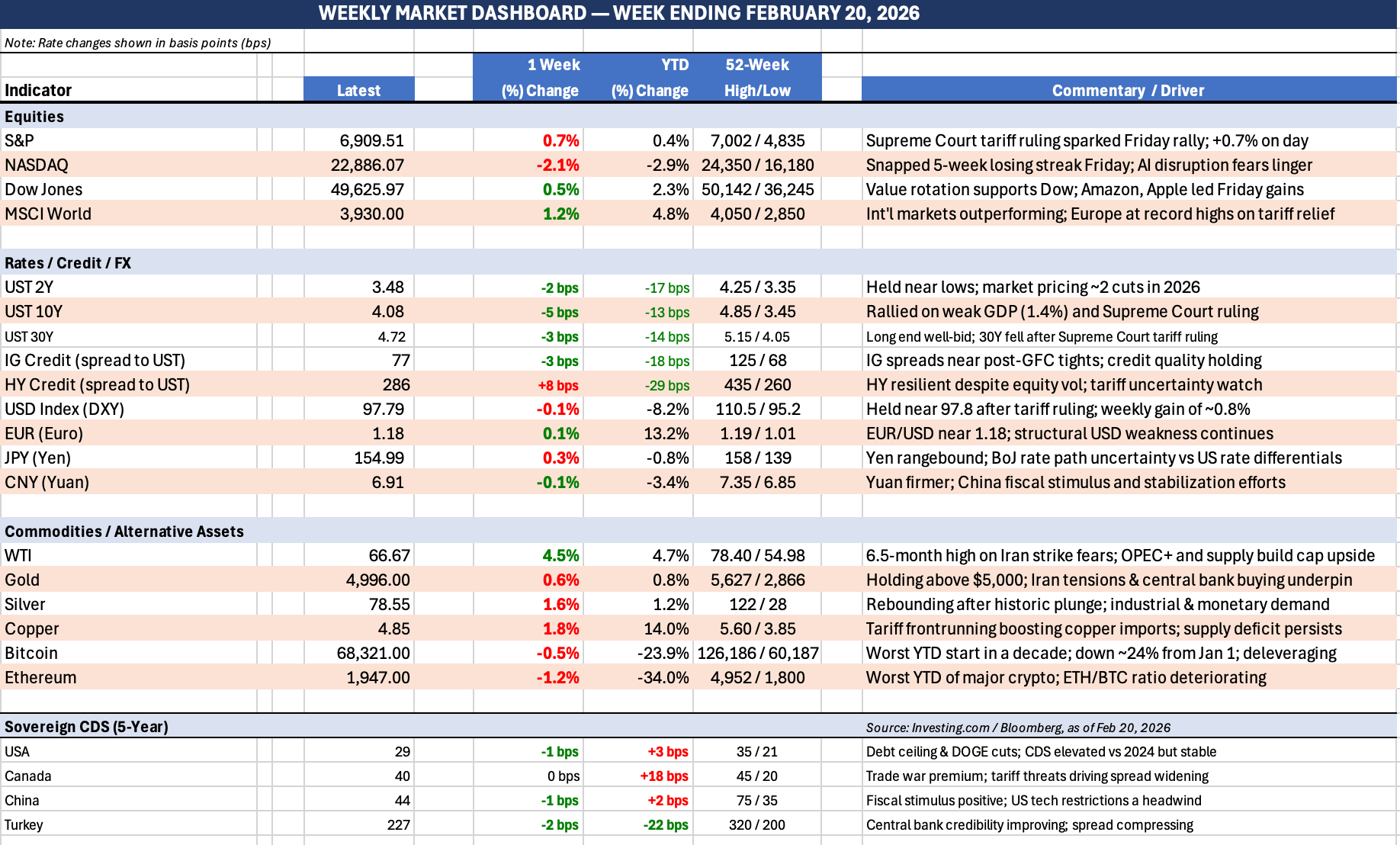

### MARKET RECAP

Global financial markets had a mixed week.

- In equities, the S&P finished +1.1% on the week, as the SCOTUS ruling on IEEPA tariffs on Friday offset private credit worries stemming from Blue Owl’s decision to suspend redemptions. Non-US equities continued their outperformance, with European bourses gaining as much as +2.9% (Spain). In Asia, while most markets were closed for the Lunar New Year holidays, South Korea hit a new high on Friday, up a blistering +5.5% from a week ago.

- In currencies, the US dollar advanced against the majors, with the Japanese yen (-1.5%) and the British Pound (-1.3%) among the main losers. The notable exception was the Chinese yuan, which gained half a percent against the greenback.

- Global bonds had a mixed week. US Treasuries gave back some of the prior week’s gains in response to the hawkish tilt in the January FOMC minutes and a higher-than-expected December core PCE print (+3.0% YoY). The 10-year yield closed at 4.08%, +3 bps from a week ago. By contrast, Japan extended its post-election rally on foreign buying, with the 30-year JGB yield ending the week at 3.32%, the lowest since late November.

- In commodities, crude oil rose 6.1% amid growing fears of US-Iranian military action. Precious metals also had a strong week, with silver outperforming, advancing +9.3%. A safe haven bid pushed gold +1.3% to close above $5,100 for the first time since January 29. However, cryptocurrencies remained sluggish, with Bitcoin ending the week down 1.6%.

### LOOKING AHEAD THIS WEEK

Next week’s key US data releases include February consumer confidence and January producer price index. Markets will be looking for further clarity on tariff developments, particularly as it relates to the refund process following the SCOTUS ruling on IEEPA tariffs, as well as the 10% global tariff (raised to 15% early Saturday) under Section 122 of the Trade Act of 1974 that was signed by President Trump late Friday. Investors remain wary of a potential US military strike on Iran, although Congress members are reportedly preparing for a vote this week to block President Trump from launching attacks on foreign countries without congressional approval.

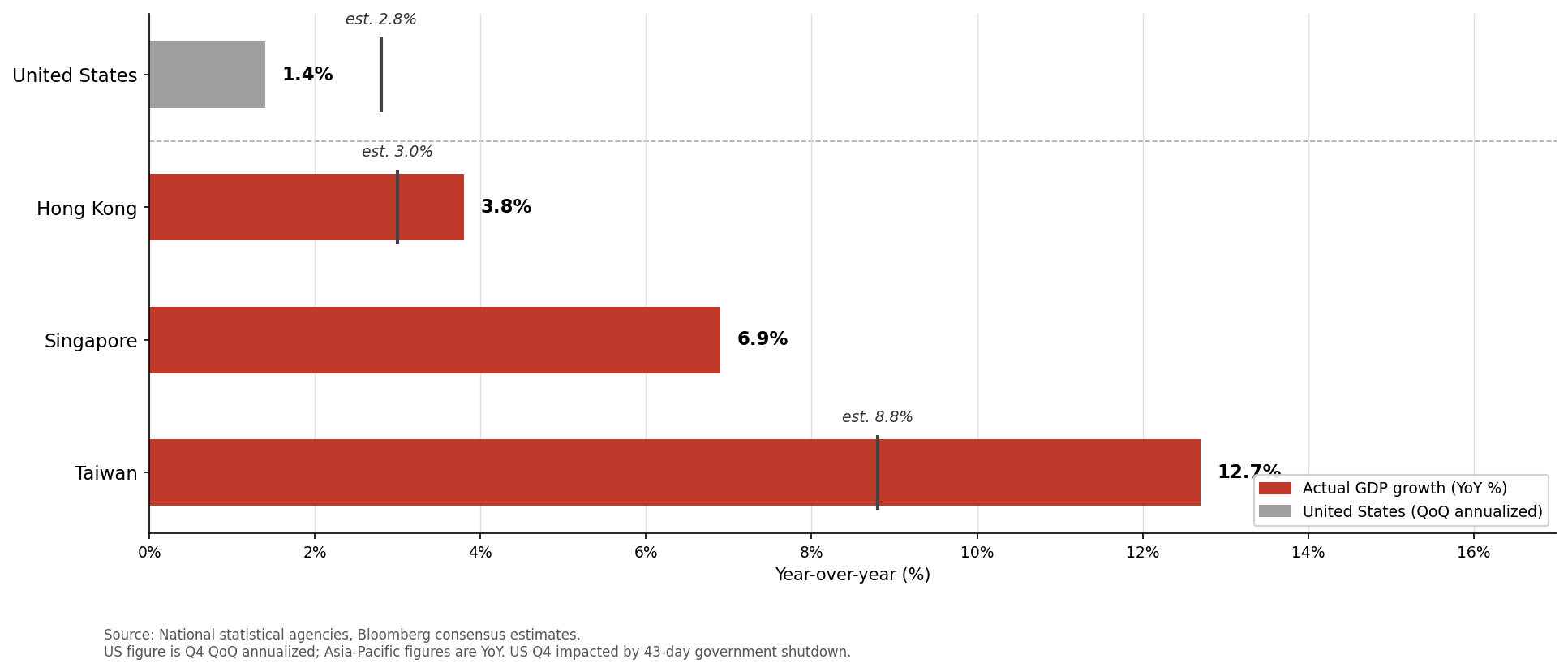

### FOCUS THEME: Cyclical Growth Paths Turn Less Synchronized

US economic momentum decelerated sharply toward the close of the year. GDP grew a paltry 1.4% QoQ (consensus 2.8%) in Q4, down from an average 4.1% QoQ in the preceding two quarters. The outturn largely reflected a one-off drag from the 43-day government shutdown, spanning nearly half of the October–December period. Household consumption cooled but remained sturdy, while IT capex continued to hold up.

The Q4 disappointment in the US stands in stark contrast to impressive Q4 GDP prints in Taiwan, Hong Kong, and Singapore. Despite their openness, the impact of heightened global trade tensions on all three economies has not been as significant as feared, suggesting that idiosyncratic factors are steering their cyclical paths.

**Taiwan.** The economy finished the year on a high note, with Q4 GDP up a staggering 12.7% YoY (consensus 8.8%), the fastest pace in nearly four decades. Full-year 2025 growth reached a 15-year high of 8.7%, led by insatiable demand for high-end semiconductors. TSMC recently guided its AI accelerator revenue CAGR to the mid-to-high 50% through 2029. With 2026 projections near 8%, Taiwan is poised to remain one of the fastest-growing economies.

**Hong Kong.** Q4 GDP growth accelerated to a two-year high of 3.8% YoY (consensus 3.0%), lifting full-year growth to 3.5%, the fastest annual expansion since 2021. Financial services provided a strong boost, driven by a blockbuster year of IPO listings from new energy and tech companies. Policymakers are stepping up efforts to establish Hong Kong as an international gold trading hub.

**Singapore.** GDP expansion hastened to a five-quarter high of 6.9% YoY in Q4, buoyed by AI-led electronics manufacturing and trade flow shifts from supply chain adjustments. The government recently upgraded its 2026 growth forecast to 4%.

Despite Q4 weakness, the US economy grew by 2.2% in 2025, topping the G7 GDP league table for a sixth consecutive year. Nevertheless, the narrative of US exceptionalism may face greater scrutiny given persistent policy uncertainty. The twists and turns surrounding US tariffs, culminating in the Supreme Court ruling last Friday, pose real challenges for long-term business capex. For a global investor, desynchronized growth paths support the case for active country diversification.

### HEARD THROUGH THE GRAPEVINE

Beneath this week’s headlines, the market quietly reprices a new world order. These five pieces capture the forces driving that shift: a tariff regime thrown into legal limbo, a nuclear standoff with no clear off-ramp, a historian’s Cold War warning, a new case for active management, and a slow-motion entitlement reckoning heading toward your retirement income.

**The Court Strikes Down Trump’s Tariffs — Then He Raises Them Anyway (Bloomberg / Reuters)**

In a 6-3 ruling on Friday, the Supreme Court held that IEEPA does not authorize the president to levy import duties, invalidating over $160 billion already collected and triggering a refund process expected to take 12 to 18 months. Hours later, Trump signed a new 15% global tariff under the Trade Act of 1974, and Treasury Secretary Bessent insisted collections would remain “virtually unchanged.” The ruling shifts the tariff era toward a slower, patchwork set of legal mechanisms, adding months of uncertainty ahead of Trump’s Beijing summit in late March.

**Iran: “Guiding Principles” Agreed, but Two Aircraft Carriers Are Parked Nearby (Axios / Al Jazeera / The Soufan Center)**

The second round of U.S.-Iran nuclear talks concluded in Geneva, with both sides claiming agreement on “guiding principles” for a deal framework, a modest step forward from the opening Oman session. The U.S. has also deployed two carrier strike groups to the region, with more than 50 advanced fighter jets within striking distance of Iranian territory. With Trump pressing deadlines and Iran holding firm on enrichment rights and missiles, diplomacy and military escalation are running in parallel, and the outcome will move oil markets and defense equities.

**Welcome to Cold War Two: Niall Ferguson on AI, Geopolitics, and the New Competition (Hoover Institution / World Economic Forum / Free Press)**

Hoover Institution historian Niall Ferguson argues that the U.S.-China rivalry is a genuine “Cold War Two,” more economically entangled than its predecessor and, because of AI, more dangerous and unpredictable. He draws a parallel to the printing press, which similarly redistributed information and destabilized existing power structures across Europe. His core warning: the technological arms race is accelerating, and the outcome of the U.S.-China AI contest will determine which capital markets lead for the next generation.

**The “Smart Money” Is Back: Active Management Finally Outperforming Passive (Bloomberg)**

In a market rattled by tariff whiplash, AI disruption fears, and stretched valuations, tactical active management is outperforming passive strategies in ways rarely seen over the past decade. Nearly 30% of S&P 500 companies have risen or fallen by more than 20% over three months, creating the dispersion that rewards research-driven stock selection, with chipmakers rallying while legacy software firms fall. After years of index fund dominance, the case for selective, actively managed strategies across equities and fixed income is re-emerging, backed by real data.

**The Social Security Clock Is Moving Faster Than Congress (CBO / Fortune / Committee for a Responsible Federal Budget)**

This week’s CBO outlook moved the Social Security insolvency date up a full year to fiscal 2032 and raised the projected automatic benefit cut from 24% to 28%, meaning a retiree receiving $2,000 per month could face a reduction of roughly $560 monthly without congressional action. The drivers are converging tariff-driven inflation, lifting cost-of-living adjustments, slower payroll tax growth from reduced immigration, and a retiring generation drawing benefits faster than workers can replenish them. For families with multigenerational wealth plans, the 2026 midterms represent the last realistic legislative window before this deadline turns imminent.