Crosslight Weekly Perspective - April 19, 2026

Strait Talk: While the world watched the Strait of Hormuz, the Taiwan Strait quietly became the bigger story.

### KEY TAKEAWAYS

- Hopes of a Gulf peace deal lifted markets broadly

- The longer-term effects on growth and prices have not fully played out

- Stretched valuations keep us on the sidelines for now

### MARKET RECAP: Peace and Pause, for Now

Markets rallied broadly this week on optimism that the US and Iran are moving toward a peace deal. Iran reopened the Strait of Hormuz for the 10-day Israel-Lebanon ceasefire, though mixed signals from both sides suggest differences remain. Talks resume this weekend.

- **Stocks rallied worldwide.** The S&P 500 (+4.5%) and NASDAQ (+6.2%) hit new highs, fully erasing losses from the US-Iran conflict. Falling oil lifted Asia’s importers, with South Korea (+5.7%) and Taiwan (+3.9%) leading. China gained 2% on stronger-than-expected first-quarter GDP of 5.0%, and Europe rose 2 to 3%, with Germany up 3.8%.

- **The dollar weakened for a third straight week.** Commodity-linked currencies outperformed, with the Norwegian krone and Australian dollar both up 1.6%. The standout was Hungary’s forint, which jumped 4.2% to a four-year high after Peter Magyar unseated Viktor Orban.

- **Bonds strengthened** as lower oil eased inflation concerns. European and UK 10-year yields fell about 10 bps, and the US 10-year ended at 4.25%, down 7 bps. Emerging-market bonds in Brazil, Mexico, and South Africa also rallied.

- **Commodities were mixed.** Brent crude fell 3% to around $90 a barrel on the Strait reopening, though it is still 24% above pre-conflict levels. Precious metals climbed, with silver up 6.6% and gold up 1.7%.

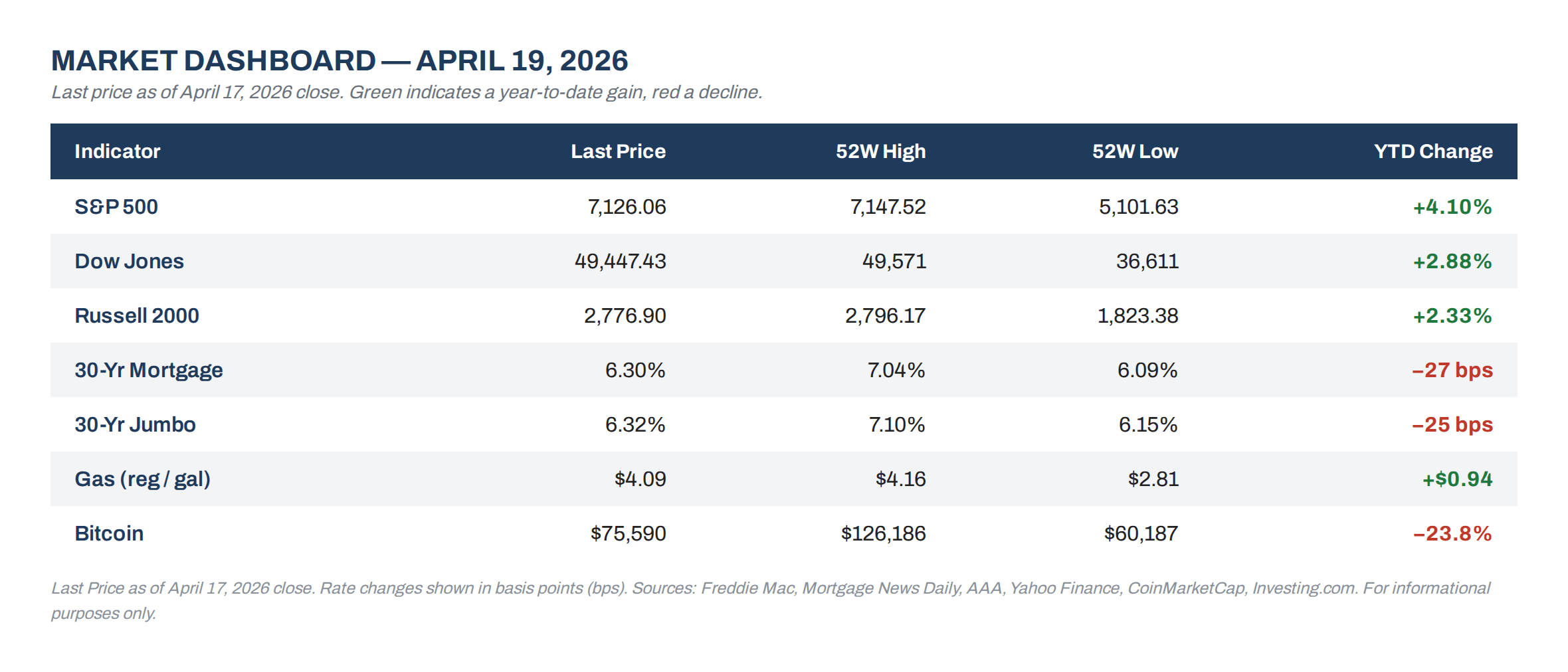

### MARKET DASHBOARD

### LOOKING AHEAD THIS WEEK

#### Economic data.

A wave of leading indicators will offer the first read on how higher crude prices are affecting activity. PMIs in Japan (Wed), the US (Thu), and the Eurozone (Thu) are expected to hover near the neutral 50 mark. In the UK, March CPI (Wed) will draw close attention after recent bond-market volatility.

#### Central banks.

Kevin Warsh, President Trump’s pick for Fed Chair, testifies before the Senate Banking Committee on April 21. The hearing comes amid Democratic objections, with some lawmakers arguing it should be postponed until investigations into Fed Chair Jerome Powell and Governor Lisa Cook conclude. On policy, central banks in Indonesia (Wed), Turkey (Wed), and the Philippines (Thu) are expected to hold steady as they await further clarity on the Gulf.

#### Middle East.

Despite ongoing indirect talks between the US and Iran, the two-week ceasefire announced on April 8 formally expires on April 22 (Wed).

### FOCUS THEME: Strait Talk

While the world’s attention has been fixed on the Strait of Hormuz since the US-Iran conflict began on February 28, another significant cross-Strait event occurred earlier this month. Li-wun Cheng, chairwoman of Taiwan’s opposition Kuomintang (KMT), visited China from April 7 to 12. Beijing has refused official relations with the pro-independence Democratic Progressive Party, Taiwan’s ruling party since 2015, which makes the timing notable. Touted as a “peace journey” across Beijing, Nanjing, and Shanghai, the trip culminated in a meeting with President Xi Jinping at the Great Hall of the People, the first formal meeting between leaders of the Chinese Communist Party and the KMT in over a decade.

The parallels between the two straits are uncanny. The Taiwan Strait carries 20% of global maritime trade and is a critical chokepoint for technology and energy. For Japan and South Korea, nearly a third of imports pass through it. The strait is roughly 110 miles wide, but the narrowest point, between Xiamen on the mainland and Taiwan’s Kinmen Islands, is just 1.3 miles.

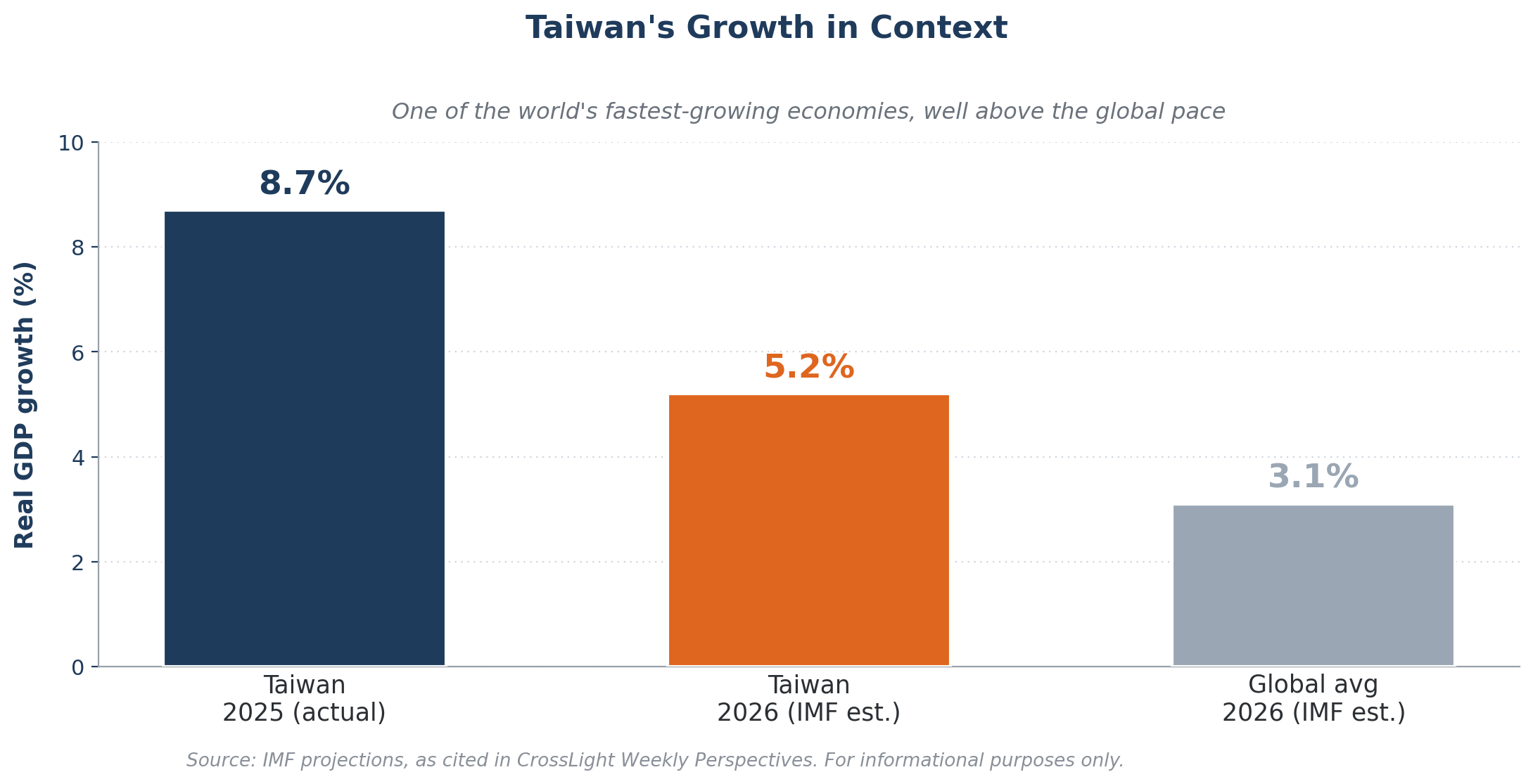

The semi-official trip gave Taiwan’s financial assets a timely boost. By market capitalization, Taiwan’s bourse rose to a record $4.14 trillion this week, surpassing the UK as the world’s seventh-largest. Taiwan is also poised to be one of the fastest-growing economies in 2026, with the IMF projecting 5.2% GDP growth against a 3.1% global average, after a blistering 8.7% expansion in 2025 driven by demand for high-end semiconductors. Taiwan Semiconductor Manufacturing Company is the world’s largest dedicated chip foundry and ranks among the largest non-US companies by market value. Yet the economy's deeper strength lies in its small and medium-sized enterprises, which make up more than 95% of businesses.

The successful US military operation in Venezuela in early January fueled concern among analysts of a similar move by Beijing on Taiwan. In our view, such comparisons are misplaced, given the strong economic ties between the two. We do not dismiss cross-Strait tension as a risk, but from China’s standpoint a military operation is far from the policy of choice.

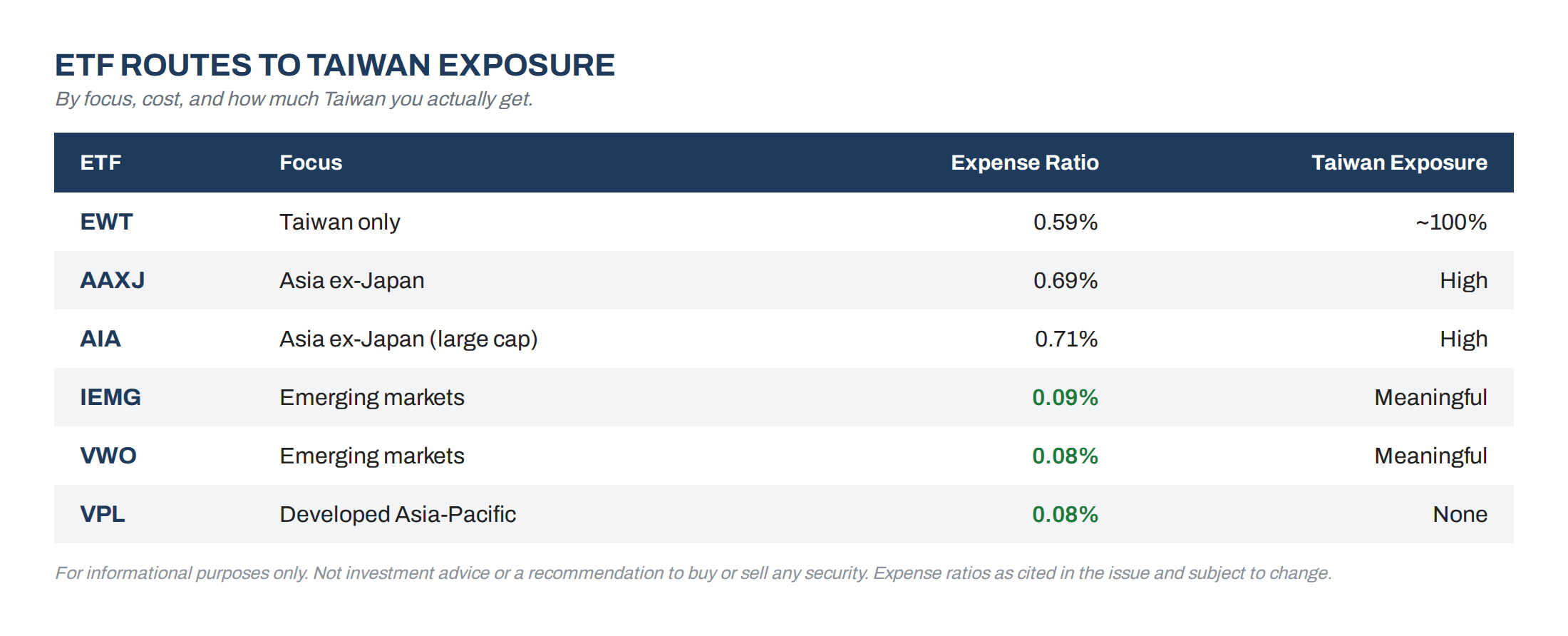

For US investors seeking exposure, several ETFs offer different routes to Taiwan at different costs.

#### Heard Through the Grapevine: How to Stop Iran From Winning the War

In a joint Free Press essay on April 9, Niall Ferguson, Richard Haass, and Philip Zelikow argue that the Strait of Hormuz must reopen, but not on Iran’s terms. Tehran’s demand to tax and regulate shipping would cement its role as toll-keeper of a waterway that carries a fifth of global oil, handing Iran a strategic win that offsets its battlefield losses. The authors propose a three-step response: credible military readiness to ensure safe transit, a backchannel understanding to restart commercial shipping, and a new Hormuz Convention modeled on the agreements governing the Black Sea straits (1936) and the Suez Canal (1888). Under it, a jointly owned Strait of Hormuz Company, with the eight coastal states and the US as principal shareholders, would manage the strait as a neutral waterway with regulated transit fees. The plan is designed to work with Iran rather than require regime change. The broader takeaway for markets is that the terms of reopening matter as much as the reopening itself.

Thank you for reading CrossLight’s Weekly Perspectives. If you wish to talk through any of these themes, please reply to this note. This note is strictly for informational purposes only and does not constitute investment advice for the reader.