Crosslight Weekly Perspective - April 26, 2026

Don't Worry be Happy - Stocks hit records while a diplomatic mission collapses and inflation catches up with oil. The Fed's independence is the question underneath it all.

### KEY TAKEAWAYS

- Tech euphoria is doing a lot of work to mask real geopolitical risk

- The macro bill from higher oil is arriving, and oil importers will pay first

- A narrow rally leaves little margin for a macro surprise

### MARKET RECAP: Don’t Worry, Be Happy

A diplomatic mission collapsed, an Iranian military commander warned of retaliation, and the inflation data finally caught up with the oil price. The S&P 500 closed at a record. So did the NASDAQ. That is either remarkable composure or remarkable inattention. Both have been wrong before.

The Witkoff-Kushner trip to Islamabad was cancelled on Saturday with hours to spare; the President said the Iranian offer was not good enough and that the US “has all the cards.” March CPI showed energy up 10.9% on the month and gas-station spending up 15.5% on the month, a record. A handful of governments, the UAE included, have begun asking Washington about dollar swap lines. And two private loans, Medallia and Affordable Care, defaulted, the kind of small data point that becomes a large one in retrospect.

- **Equities:** tech did the heavy lifting again. The NASDAQ added 2.4% to a fresh record, the S&P 500 tagged along with a 0.8% gain to its own all-time high, and Intel, of all names, posted its best quarter in nearly forty years. Look beneath the surface, though, and the picture thins out: financials and healthcare continued to lag. In Asia, Taiwan (+5.8%) and South Korea (+4.6%) rode the same chip wave. Europe broke its four-week winning streak, with major bourses down 3 to 4%.

- **Currencies:** the dollar firmed as questions lingered over the Strait of Hormuz. The euro, yen, and Swiss franc each slipped 0.4%. The Norwegian krone was the outlier, up 0.7%, as oil exports and a hawkish central bank proved a useful combination. Emerging markets had a rougher week, with the Indian rupee (-1.4%) and South African rand (-1.2%) leading the declines.

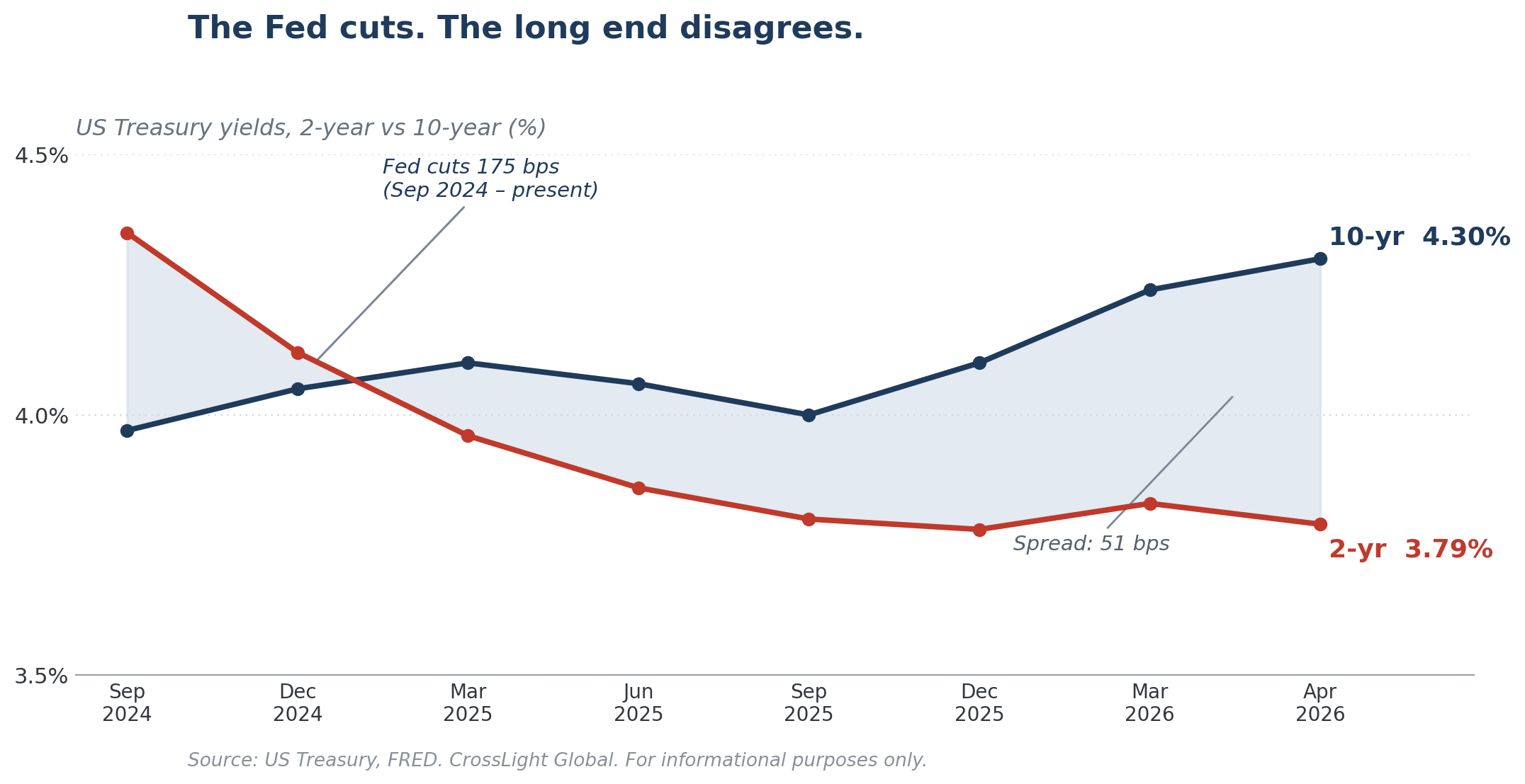

- **Bonds:** global bonds sold off on the familiar mix of cyclical inflation worries and structural fiscal anxiety. The US 10-year yield rose 5 bps to 4.30%. The UK remains the problem child of the developed world, with 10-year gilts up another 15 bps to 4.91%, near levels not seen since the financial crisis.

- **Commodities:** crude snapped back hard, with Brent up 17% and back above $100. Precious metals took a breather after their recent run, as gold gave up 2.5% and silver, ever the amplifier, fell 6.4%.

### LOOKING AHEAD THIS WEEK

#### Central banks.

A busy week of policy meetings, all expected to hold steady: Japan (Apr 28), the Fed and Bank of Canada (Apr 29), the ECB and Bank of England (Apr 30). Brazil (Apr 28) is the exception, set to deliver its second 25 bps cut of the year.

#### Economic data.

First-quarter GDP and April inflation prints dominate the calendar. US GDP (Apr 30) likely came in around 2.2% annualized, with core PCE running at 3.2%, still well above the Fed’s 2% target. The Eurozone offers the usual contrast: Q1 GDP a tepid 0.9% year-on-year, with CPI accelerating toward 3%. Taiwan’s Q1 GDP (Apr 30), expected at 10.7% year-on-year, is on track for a second straight quarter of double-digit growth, the chip cycle in numerical form.

### FOCUS THEME: Fed Independence Back in the Spotlight

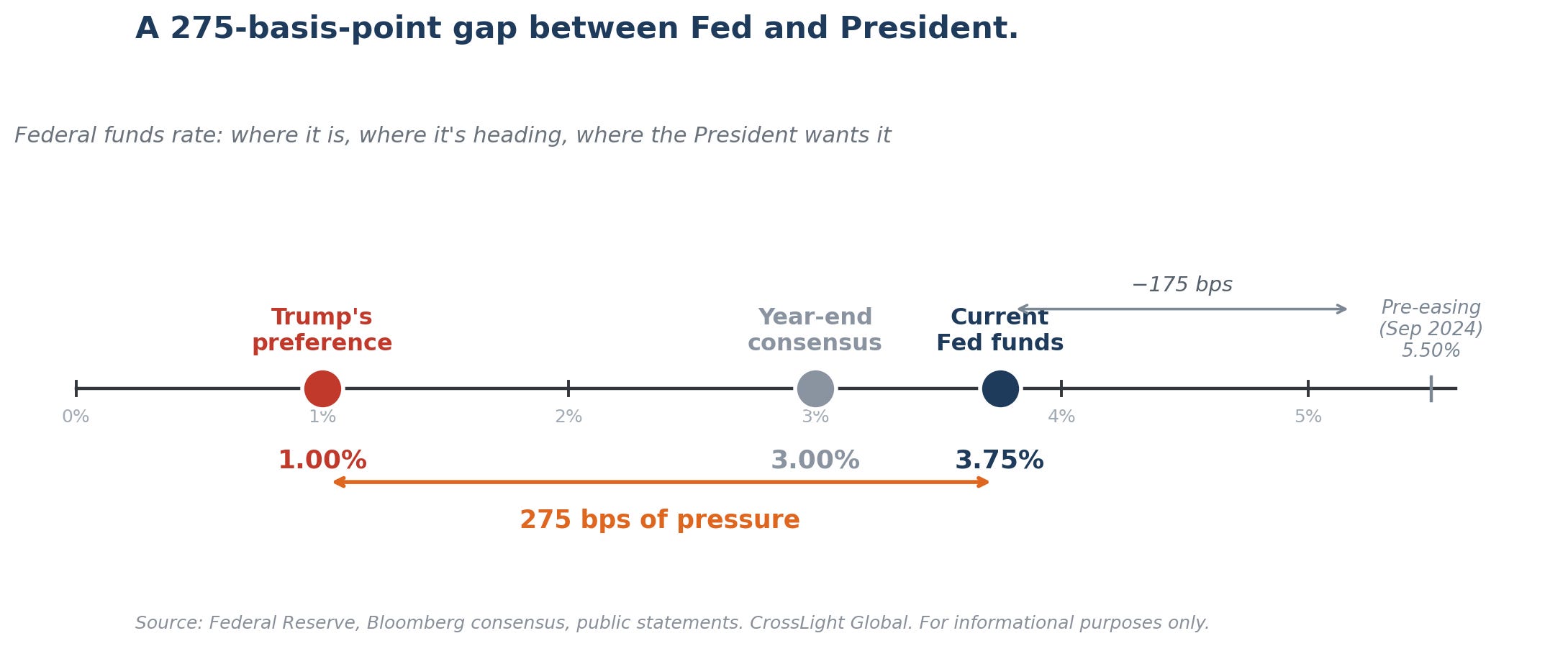

Last week’s nomination hearing for Kevin Warsh put Fed independence back on the table. Warsh said the right things: a commitment to independence and no rate-cut promises to the President. Trump, less restrained, repeated his view that America “should have the lowest interest rate in the world” and warned he would be “very disappointed” if a Warsh-led Fed failed to deliver.

On Friday, the Department of Justice dropped its criminal investigation into Jerome Powell, clearing one of the larger obstacles to a Warsh confirmation. US Attorney Jeanine Pirro left the door ajar, noting the probe could resume should the facts warrant. Whether the impasse is resolved before Powell’s term expires on May 15 is anyone’s guess; one workable scenario is for him to remain acting Chair until his successor is confirmed.

Why does this matter? Because American economic exceptionalism has rested, in no small part, on the Fed’s reputation. If the next Chair is seen to bend to political demand, markets will read it as a softening of the inflation-fighting mandate, an awkward signal at a moment of surging oil prices. Traders are not waiting for confirmation: front-end rates already firmed on Friday’s news, on the assumption that a Warsh Fed will cut.

The Iran spillover into the macro data has already arrived. The energy component of US CPI rose 10.9% month-on-month in March, the fastest pace in over two decades. Spending at gas stations climbed 15.5% month-on-month, the largest single-month jump since the series began in 1992.

Growth, for now, is holding up. The composite PMI surprised to the upside at a three-month high of 52.0 against a 50.6 consensus. The University of Michigan consumer sentiment index landed at a record-low 49.8, but was revised up from a preliminary 47.6, cold comfort perhaps, but better than feared. Put simply, an economy near full employment with inflation a full point above target is not obviously one that needs lower rates.

Lower short rates have fueled the rally in risk assets ever since the Fed began easing in late 2024, taking the funds rate down 175 bps to 3.75%. The President, for the record, would prefer 1%. But the long end, which is what most of the real economy borrows against, answers to markets, not to the Fed. If inflation persists, holders of 10-year and 30-year Treasuries will demand higher yields to compensate. Cutting at the front end while the long end refuses to follow gives you a steeper curve, not cheaper financing.

The equity expression of a steeper curve is long regional banks and life insurers, underweight office REITs and homebuilders. Business models that fund short and lend long win; those that refinance long lose.

Our base case has the Fed on hold for the rest of 2026. A cut under Warsh is not off the table, but it would be neither necessary nor wise. Two implications for portfolios follow. First, stay anchored at the front end of the US curve: inflation pressures look sticky, and Gulf-related fiscal outlays could rouse the bond vigilantes. Second, lean into non-dollar exposure: Fed easing erodes the dollar’s carry advantage over the yen and euro and sharpens the medium-term case for higher-carry emerging-market names such as the Brazilian real and the Mexican peso.

#### Heard Through the Grapevine: The Medallia receipt

A small detail sits behind one of last week’s two private-credit defaults. Thoma Bravo bought Medallia for $6.4 billion in 2021, a bet on customer-experience software during the era of near-zero rates. The lenders, Blackstone, KKR, Apollo, and Antares, now hold the keys, and $5.1 billion in equity is wiped out. Blackstone’s largest credit fund flagged Medallia and Affordable Care as the two names driving its non-performing ratio to a record 2.4%. UBS warns that an “AI SaaSpocalypse” could double private-credit default rates to 9 to 10%. The vintage matters: this is the 2021 cohort, financed at money-for-free rates, refinancing into a world where neither the rates nor the AI thesis cooperate. The first two names are almost never the only two.

#### Heard Through the Grapevine: The UAE’s other hand

While one hand reached for swap lines, the other was buying gold. The Central Bank of the UAE quietly added 12 tonnes in February. Small in absolute terms, but consistent with the broader pattern: 68% of central banks plan to increase gold holdings in 2026, and emerging-market reserves are tilting away from the dollar in a measured but unmistakable way. The swap-line conversation gets the headlines. The gold purchase is the hedge in case the swap lines do not come.

*Sources: Medallia restructuring and private-credit stress, Reuters and Bloomberg, April 2026, and Blackstone Secured Lending Fund regulatory filings, Q1 2026. UAE gold purchases and central-bank reserve trends, World Gold Council Central Bank Gold Statistics, February 2026, and WGC Central Bank Gold Reserves Survey, March 2026.*

Thank you for reading CrossLight’s Weekly Perspectives. If you wish to talk through any of these themes, please reply to this note. This note is strictly for informational purposes only and does not constitute investment advice for the reader.