Crosslight Weekly Perspective - February 15, 2026

The Dollar's Demise Is Overstated: China is trimming Treasuries and the deficit math looks grim. But the dollar's demise is overstated; its privilege erodes slowly, not overnight.

### KEY TAKEAWAYS

- Downside inflation surprise and strong payroll report bolster US cyclical stability

- Price volatility in alternative assets persists, but no sign of market contagion

- Concerns over long-term debt sustainability on the back burner, for now

### MARKET RECAP

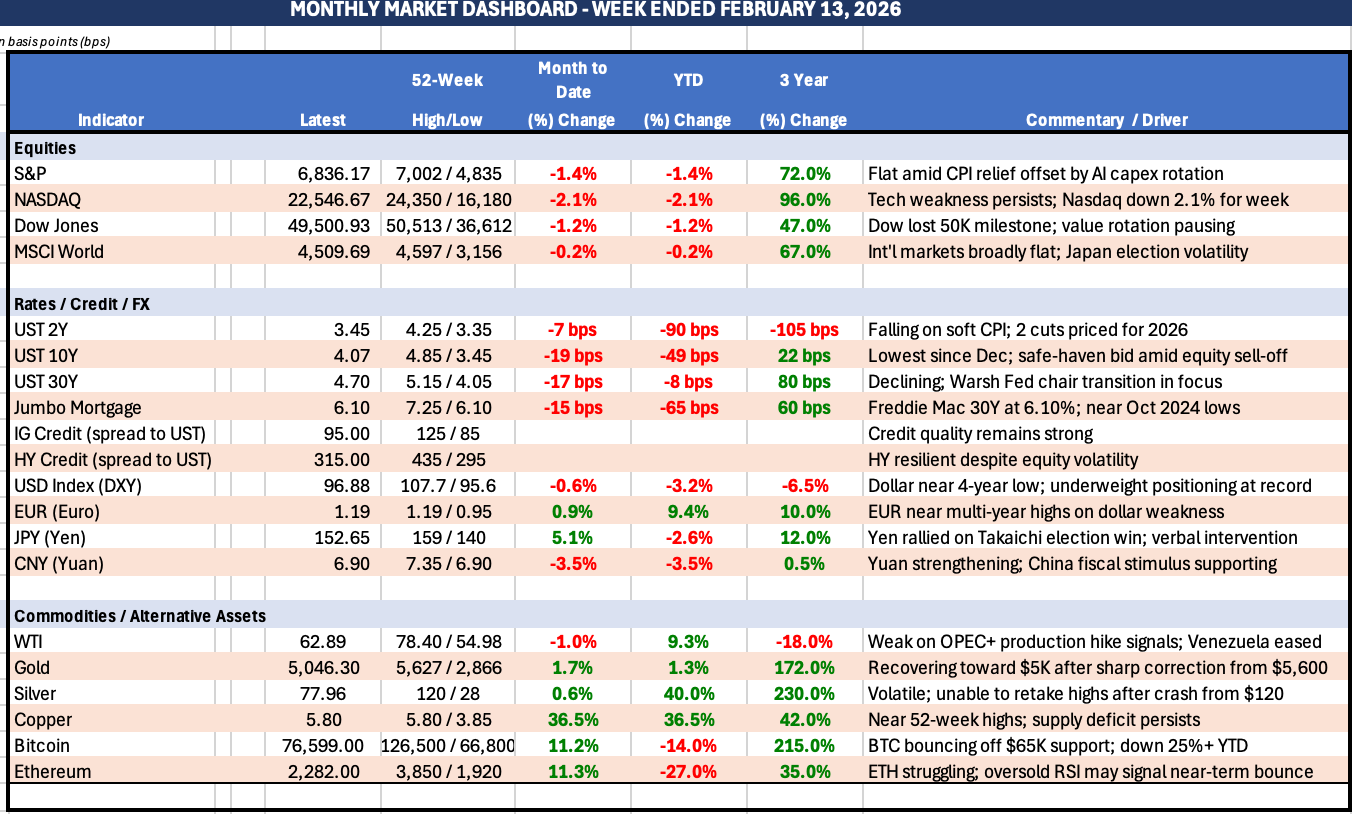

Financial markets ended the week mixed across asset classes.

- Global equities saw Asia-Pacific leading the pack, with outsized weekly returns in Korea (+8.2%), Japan (+5.8%), and Thailand (+5.6%). In the US, the S&P shed -1.4%, led by financials amid fears of AI-induced disintermediation.

- In currency markets, a weak-dollar theme resumed after a one-week hiatus. The Japanese yen and the Thai baht gained +3.0% and +1.8% respectively, buoyed by post-election optimism. The Norwegian krone (+1.7%) was the distinct outperformer in Europe, given diminished prospects of a rate cut following an upside CPI surprise.

- Global bonds had a uniformly strong week. US Treasuries overcame a solid January employment report, as a downside CPI surprise pushed the 10-year bond yield down to 4.05%, the lowest since last November. In Japan, long-dated bonds closed -12 bps as investors digested Prime Minister Sanae Takaichi’s fiscal expansion plans.

- For precious metals and cryptocurrencies, market action remained choppy, with silver plummeting by 10.7% on Thursday. For the week, silver retraced its losses to finish -0.5%, but gold showed tenacity, gaining +1.6%. Bitcoin traded below the $70,000 level for most of the past week.

### LOOKING AHEAD THIS WEEK

Despite a shortened week due to Presidents’ Day, a slew of data releases (Q4 GDP, durable goods, industrial production, flash PMIs, and FOMC minutes) will provide further clues on the state of the US economy. Major markets across Asia are closed for the weeklong Lunar New Year holidays.

### FOCUS THEME: Quick Thoughts on the Dollar’s Exorbitant Privilege

Last week, Chinese regulators reportedly urged domestic banks to reduce Treasury exposure, citing volatility and concentration risk. This is consistent with China’s decade-long shift away from Treasuries, with holdings down from a $1.3 trillion peak in 2013 to $682 billion today. Separately, pension funds in Denmark, the Netherlands, and Sweden have also reduced or exited Treasury positions over the past year.

Meanwhile, the Congressional Budget Office’s (CBO) annual report last Wednesday warned that the U.S. fiscal path is unsustainable, echoing similar concerns raised by Fed Chair Powell in January. The agency projects a $1.4 trillion increase in deficits over the next decade, driven by tax and immigration policies. As a share of GDP, the deficit is expected to rise to 6.7% by 2036, up from 5.8% this year and well above the long-term average of 3.8%.

These developments have raised questions about the dollar’s status as a reserve currency and its role in financing persistent deficits. In our view, those concerns may be overstated in the near term for two reasons.

First, relative to other G7 countries, U.S. reliance on foreign investors is not unusually high. Foreign ownership of Treasuries has declined from nearly 50% in 2008 to about 30% today—roughly in line with Germany and the UK, and well below France’s 54%.

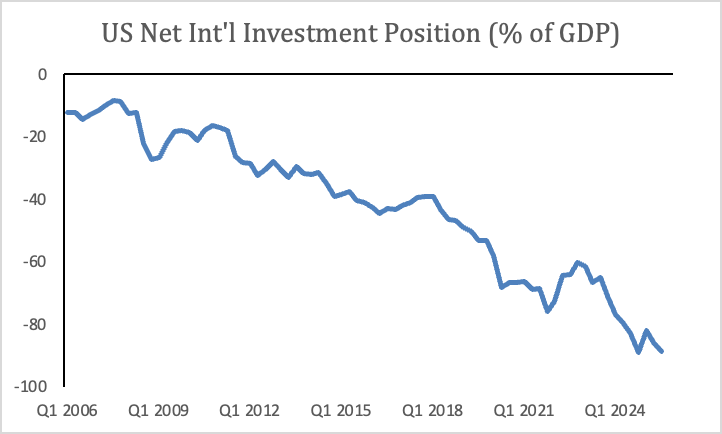

Second, while the U.S. net international investment position has deteriorated sharply to -90% of GDP from -10% two decades ago, much of this reflects valuation effects. Strong outperformance of U.S. assets and dollar appreciation have increased the dollar value of foreign-held liabilities, mechanically weakening the NIIP.

*Source: Federal Reserve Bank of St Louis*

Not surprisingly, bond markets showed little reaction to either headline. Instead, a softer-than-expected CPI print drove a Treasury rally, with the 30-year yield falling to 4.70%, its lowest level since November.

That said, medium-term risks remain. Running deficits at full employment postpones fiscal adjustment, political pressure on the Fed could complicate policy, and geopolitical tensions may gradually weaken foreign demand for Treasuries, particularly from central banks.

Over the next 3–5 years, the dollar may gradually decline as global portfolios rebalance, though likely in an orderly fashion. Its dominant role should remain intact, supported by deep, liquid U.S. financial markets and strong network effects, even as competition from currencies such as the yuan intensifies.

### HEARD THROUGH THE GRAPEVINE

Beneath calm index levels, markets are undergoing a quiet but meaningful repricing. These five pieces highlight the forces driving that shift, from AI’s impact on business models and capital allocation, to rising geopolitical risk, evolving financial infrastructure, and the broader societal changes shaping the next generation.

**Why Stocks Are Making Gigantic Moves All Over the Place (Barron’s)**

Individual stocks are making unusually large moves even as overall market volatility remains subdued. Nearly 30 percent of S&P 500 companies have risen or fallen by more than 20 percent in the past three months, as AI reshapes profit expectations across industries. Chipmakers, data center suppliers, and commodity producers are rallying, while many software firms are falling on fears that their business models may be disrupted. Hedge fund inflows and momentum-driven strategies are amplifying both the upside and downside.

**Investors reluctant to ‘buy the dip’ after AI scares (Financial Times)**

Investors are no longer stepping in to buy stocks that fall on AI disruption fears, reflecting deeper uncertainty about which business models will endure. Even sharp declines in sectors like wealth management, trucking, and real estate have failed to attract the usual bargain hunters, as traditional moats are being reassessed. Institutional capital is shifting toward hardware and infrastructure and away from vulnerable software models. The hesitation reflects a growing recognition that AI is not just another cycle, but a structural shift in profit pools.

**Donald Trump says regime change ‘the best thing that could happen’ in Iran (Financial Times)**

President Trump publicly suggested regime change in Iran would be desirable while deploying a second aircraft carrier strike group to the Middle East, signaling a sharper escalation in posture. The military buildup, including advanced ships, aircraft, and missile defenses, increases US leverage as nuclear negotiations with Tehran continue. The move reflects both preparation for potential military action and an effort to pressure Iran into concessions at the negotiating table. Markets will view this as raising geopolitical risk, particularly for oil, defense spending, and broader regional stability.

**Don’t ban teenagers from social media (The Economist)**

The article argues that banning teenagers from social media would likely cause more harm than good, despite widespread concern about mental health and safety risks. Evidence linking social media to widespread psychological damage remains limited, and bans would be difficult to enforce, potentially pushing teens toward less safe or less regulated platforms. Social media also provides meaningful benefits, especially for isolated or marginalized teens who rely on online communities for support and information. The better solution is stronger regulation, improved safety features, and more transparency from tech companies rather than outright prohibition.

**Asia is turning stablecoins into banking infrastructure (The Economist)**

Stablecoins are rapidly becoming a core part of financial infrastructure across Asia, especially for remittances, freelance payments, and cross-border business transactions. Workers and businesses are using dollar-pegged tokens to avoid high banking fees and delays, with global stablecoin transfers exceeding $4 trillion in recent periods. Adoption is strongest in countries with large freelance populations and remittance flows, where stablecoins offer faster settlement and lower costs than traditional banks. The shift suggests stablecoins are evolving from speculative assets into practical payment rails that could reshape cross-border finance.

Thank you for reading CrossLight's Weekly Perspectives… This note is strictly for informational purposes only and does not constitute investment advice for the reader.