Crosslight Weekly Perspective - July 12, 2026

The dollar has clawed back its 2025 losses, propped up by a wide US rate gap and oil priced in greenbacks. Both supports are cyclical, and as they fade we look to emerging-market currencies and gold.

**Key Takeaways**

- The ceasefire between the United States and Iran broke down last week. Oil rose, but not by enough to change the picture. We still expect global growth to hold up in the second half.

- The Fed looks set to leave rates where they are through year-end, even as central banks abroad raise theirs. That gap has been the dollar’s best friend.

- As that advantage fades, we expect money to move toward assets outside the dollar. Emerging market currencies and gold top our list.

## MARKET RECAP: Carry On?

The dollar spent 2025 falling and has spent 2026 climbing back. A widely watched gauge of its value against other major currencies is up 2.7% this year, after a 9.4% drop last year. In our view the recovery rests on two supports, and both trace back to the war between the United States and Iran that began in late February.

**Higher interest rates.** At the start of the year, investors expected the Fed to cut rates. The war changed that. Rising oil prices revived inflation fears, and by spring markets were betting on at least one rate rise before year-end. Higher rates mean holders of dollars are paid better to wait.

**Oil is bought in dollars.** About 80% of the world’s oil trades are invoiced in dollars. When the price of oil spikes, buyers around the world need more dollars to pay for the same barrels.

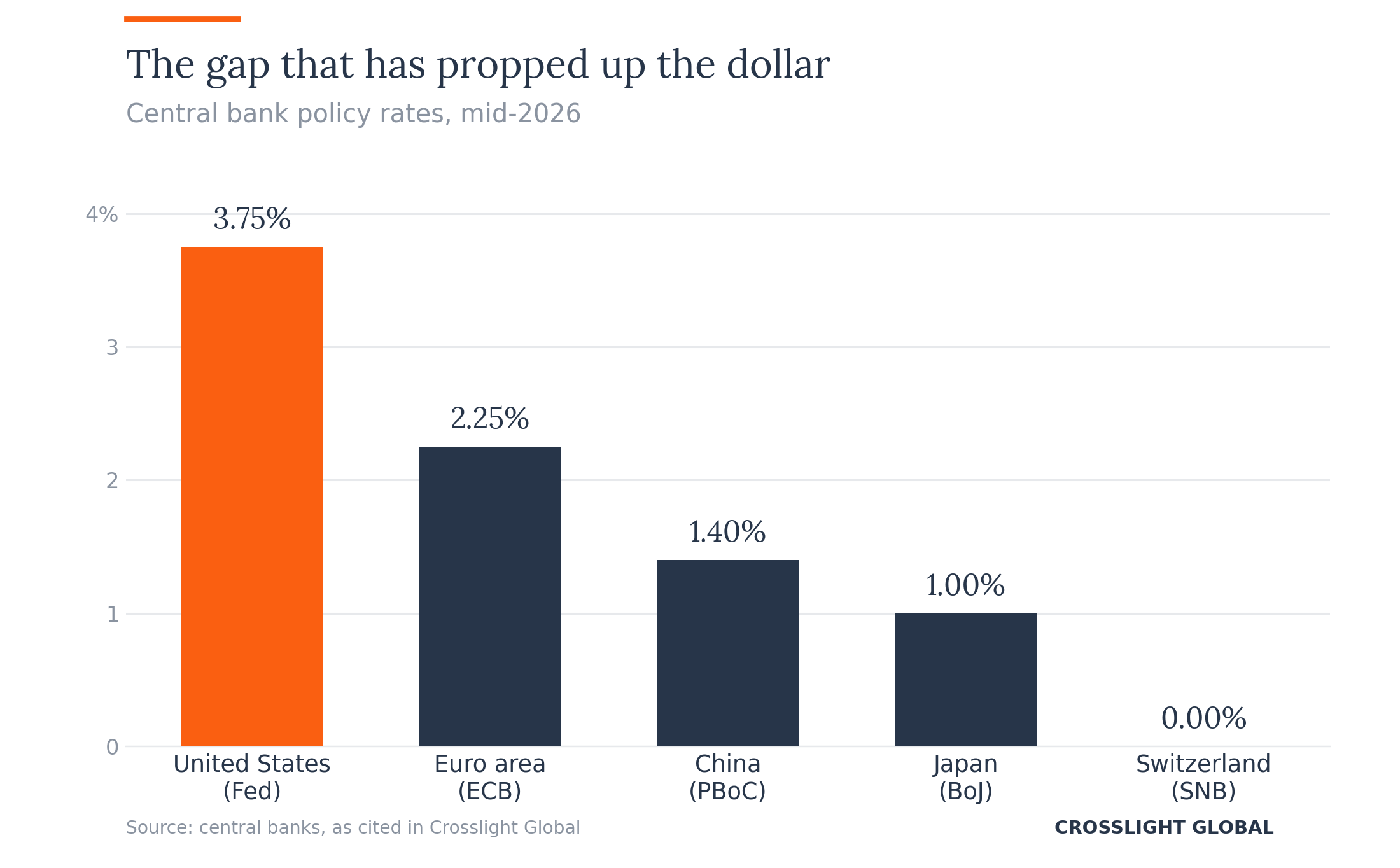

The gap between American rates and everyone else’s is striking. The Fed’s policy rate sits at 3.75%. The European Central Bank’s is 2.25% and the Bank of Japan’s 1.00%, even after both turned tougher on inflation this year. That gap feeds the carry trade, in which an investor borrows in a cheap currency such as the yen or the euro and parks the money in dollars to collect the difference. The same logic works against gold, which pays nothing to those who hold it.

There are exceptions. The Chinese yuan has gained 3.1% against the dollar this year despite a policy rate of just 1.40%. And history suggests interest rate gaps are not what make a reserve currency. Investors will accept a lower yield, in effect paying a premium, for money they trust in a crisis. Switzerland’s policy rate is zero, and the Swiss franc remains as sought after as ever.

Our view is that the Fed will hold rates steady, not raise them, for the rest of 2026. If so, the dollar’s cyclical advantage should fade in the coming months, and longer-term structural forces should reassert themselves as investors rethink valuations worldwide. That conviction points to two ideas for spreading portfolio risk.

First, the carry trade should turn in favor of emerging market currencies that pay generous rates, including the Brazilian real and the Mexican peso.

Second, add to precious metals, gold above all. Demand for the metal is seasonally strong in July and August, and central banks are still quietly adding to their reserves.

Separately, a recap of last week’s markets:

**Stocks.** American markets had a strong week. The Nasdaq rose 1.7% as technology shares rebounded on the back of SK Hynix’s $26 billion debut share sale, and the S&P 500 advanced 1.3%, its second straight weekly gain. Europe went the other way, falling 1.8% and snapping a four-week run of gains after the NATO summit in Ankara revived worries about the alliance. In Asia, Hong Kong rose 3.5% and Singapore rose 4.3% as investors moved money away from the region’s technology-heavy markets in South Korea and Taiwan, which had already gained the most this year.

**Bonds.** US Treasuries weakened after the minutes of the Fed’s June meeting confirmed its stern message and tensions with Iran returned. The 30-year yield ended the week at 5.06%, up 0.07 percentage points and the highest since mid-May. Japan told the opposite story. Bonds rallied after the government urged pension funds to buy more of them, and the 30-year yield fell 0.13 percentage points to 3.88%. At last week’s auction, investors bid for more than four times the bonds on offer, the strongest demand since May 2019.

**Currencies.** A mixed week after June’s broad dollar strength. The South Korean won gained 2.0% and the New Zealand dollar 0.9%, both helped by central banks leaning toward higher rates. The Japanese yen slipped 0.2% and remains near its weakest level in forty years, despite the government’s public commitment to leaving the central bank alone to do its job.

**Commodities and crypto.** Brent crude, the global oil benchmark, rose more than 5% to about $76 a barrel after the ceasefire with Iran agreed in mid-June was annulled. Gold gave back 1.4% of the prior week’s gains as the Fed’s minutes read sternly. Bitcoin rose 2% to a three-week high of about $64,000.

## LOOKING AHEAD THIS WEEK

**Over the weekend.** The strikes did not pause. Iran hit another ship in the Strait of Hormuz on Saturday and fired on vessels again on Sunday, while American aircraft struck air defenses and small boats along Iran’s coast. The talking has not stopped, though. Washington agreed on Friday to Iran’s request to continue negotiations, and Oman has drafted a plan to operate the strait via two separately managed shipping routes. Tanker traffic has slowed to a crawl while the world waits, and oil opens the week with that tension in the price.

**Economic data.** June’s cheaper oil should show up in this week’s American numbers. Consumer prices on Tuesday are expected to have risen 3.8% from a year earlier, a step down from May. Producer prices on Wednesday likely stayed high at 6.2%, since energy costs work through supply chains with a lag. Retail sales on Thursday are forecast to have grown 0.3% on the month, softer than recent readings as gasoline got cheaper. The University of Michigan’s survey of consumer sentiment on Friday is expected to improve for a second straight month, to 51.0. Abroad, second-quarter growth figures from China (Wednesday, 4.5%), Singapore (Tuesday, 5.6%) and Malaysia (Friday, 5.4%) should confirm that the Asia-Pacific economies remain resilient. China’s trade surplus, reported Tuesday, is projected at $121.3 billion for June, the largest since January 2025.

**Central bank watch.** The minutes of the Fed’s June meeting confirmed a shift toward higher rates. A run of Fed speeches this week, including chair Kevin Warsh on Tuesday and Wednesday, will show how much disagreement sits behind that message. In Asia, the Bank of Korea is expected to begin raising rates on Thursday with a quarter-point move to 2.75%, following New Zealand’s quarter-point rise last week.

## HEARD THROUGH THE GRAPEVINE

**Schrodinger’s ceasefire.** The collapse of the truce found its historian. Niall Ferguson of the Hoover Institution sat down with The Free Press on Thursday to ask whether Iran can hold the Strait of Hormuz hostage forever. He calls the arrangement Schrodinger’s ceasefire, simultaneously a ceasefire and not one, which is as good a description as any of a deal both sides kept breaking while claiming to honor it. He also offers a comparison worth sitting with: the Taiwan Strait matters far more to the world economy than the Strait of Hormuz does. If a mid-sized power can hold one chokepoint this long, the lesson for a larger power writes itself. Oil rose just 5% on the breakdown. Ferguson’s question is whether that calm reflects wisdom or habit.

**The referee goes quiet.** Roger Ferguson, a former vice chair of the Federal Reserve, told CNBC on Wednesday that geopolitics is adding to inflation risk just as the central bank chooses to say less. Under Kevin Warsh, the Fed is stepping back from guidance on where rates are headed, and Wednesday’s minutes revealed little about which way the committee leans. Ferguson’s point is that a quieter Fed leaves investors to read the data on their own. And he reads it differently than we do: last month, he called at least one rate rise this year close to a certainty. Our view remains that the Fed stands pat. It is worth noting that a man who sat in those meetings leans the other way, and that this week’s inflation numbers arrive with little help from the referee.

---

*Thank you for reading Crosslight’s Weekly Perspectives. If you wish to talk through any of these themes, please reply to this note. This note is strictly for informational purposes only and does not constitute investment advice for the reader.*

**Sources.** Market data: Bloomberg; US Bureau of Labor Statistics; US Census Bureau; University of Michigan; National Bureau of Statistics of China; Department of Statistics Singapore; Department of Statistics Malaysia; Federal Reserve; Bank of Korea. Commentary: Niall Ferguson, “Can Iran Hold the Strait of Hormuz Hostage Forever?”, The Free Press, July 9, 2026; Roger Ferguson, remarks on CNBC, July 8, 2026. Front-page image: Udo J. Keppler, “Next!”, Puck, September 7, 1904; Library of Congress Prints and Photographs Division (LC-DIG-ppmsca-25884), public domain.

*Copyright © 2026 Crosslight Global. All rights reserved.*