Crosslight Weekly Perspective - June 14, 2026

Markets spent the week arguing over war and peace, then closed cheering the largest stock-market debut in history. Plus a plain-English tour of the biggest market on earth.

Some weeks the market argues over a tenth of a percent. This week it argued over war and peace. On Tuesday the White House promised new strikes on Iran and stocks sank. By Wednesday the Dow had shed 900 points in a day, and the morning’s inflation report showed consumer prices rising at their fastest pace in three years. Then the script flipped. Word spread that a peace deal was close, oil gave back its panic premium, and a market that began the week bracing for escalation ended it cheering the largest stock offering in history. Hold that sequence in mind as you read on, because it explains nearly everything below.

## Market Recap: Whiplash, Then Liftoff

Here is the week in order. Tuesday and Wednesday belonged to the war. Fresh threats against Iran’s oil facilities, including the Kharg Island terminal that ships most of the country’s crude, sent stocks down hard and pushed oil above $90 a barrel. Wednesday also brought the inflation report we flagged last week, and it crossed the line we expected: consumer prices were 4.2% higher than a year ago, the first reading above 4% in three years.

The detail mattered more than the headline. Energy alone accounted for more than sixty percent of the month’s increase. Strip out food and energy, which jump around the most, and the underlying rate was a much calmer 2.9%. In plain terms, this looks like a gasoline problem, not an everything problem, at least for now.

Thursday turned the week around. News that Washington and Tehran were close to a deal sent stocks surging, with the Dow up 930 points, almost exactly reversing the previous day’s drop. That same morning brought a second hot inflation number, this one measuring prices charged between businesses before they reach store shelves, and it ran at its fastest since late 2022. Markets shrugged it off, and the logic, if cold, holds up: if peace reopens the oil taps, the inflation everyone fears starts to fade on its own.

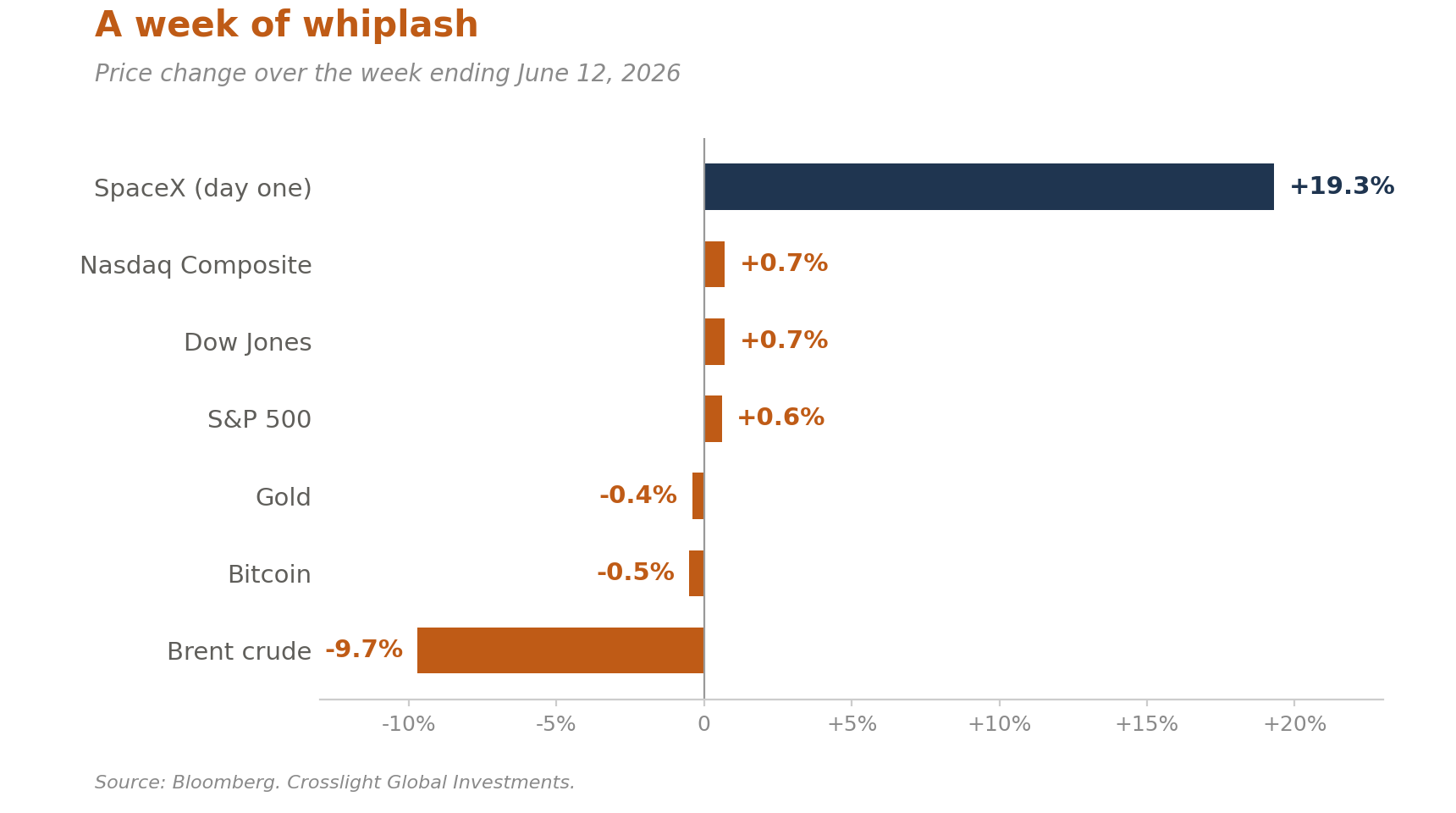

Friday delivered the finale. SpaceX began trading in the largest stock-market debut in history and jumped 19% on its first day, a striking show of nerve in a week that opened with a war scare. The mood lifted elsewhere too. Consumer confidence rose off its record low as gasoline prices eased, and the European Central Bank raised interest rates for the first time this cycle, a small step that nudges Europe further away from the cheap money of the past decade.

### Key Takeaways

- **The war premium came and went.** After a 900-point Wednesday drop and a 930-point Thursday recovery, stocks finished the week modestly higher on hopes of a signed peace deal.

- **Inflation is now two stories.** Headline prices rose 4.2%, a three-year high driven by energy, while core inflation stayed at a tame 2.9%. The new Fed chair’s first meeting on Wednesday is largely a referendum on which number to believe.

- **SpaceX answered last week’s question.** A 19% first-day gain in the middle of a war scare says the appetite for a great story is very much alive.

**Stocks.** SpaceX was the week. The rocket maker pulled off the largest stock-market debut in history, raising about $75 billion, and the shares jumped 19% on the first day to close at $161.11. That kind of welcome, in a week that began with a war scare, tells you the appetite for a great story is alive and well. The broad market was quieter than the headlines suggested: the S&P 500, the Nasdaq, and the Dow each ended up less than 1%, calm final numbers that hide a violent ride in between.

**Bonds.** The interest rate the US government pays to borrow for ten years eased to about 4.5%, down slightly from the week before as hopes of peace took hold. Read that closely, because it is the bond market’s verdict: even after a hot inflation report, lenders decided that peace, and the cheaper oil that comes with it, matters more for next year’s prices than this month’s number. The government’s regular debt auctions, the test of nerve we flagged last week, went off smoothly. Investors still expect the Fed’s next move to be a rate increase, most likely by December.

**Currencies.** The euro rose after the European Central Bank lifted rates. The Japanese yen, the subject of last week’s focus theme, stayed pinned near 160 to the dollar ahead of Tuesday’s Bank of Japan meeting, where a rate increase is widely expected. The dollar, which had climbed early in the week as nervous investors sought safety, gave up that ground on Thursday as the mood improved.

**Commodities and crypto.** Oil made a round trip: up toward the mid-$90s when the threats to Iran’s facilities landed, then back down by Friday as peace talk firmed, a swing that drove much of the week’s drama. Gold, which investors buy when they want a store of value in uncertain times, did its job, climbing to $4,215 an ounce even as stocks lurched and oil fell. Bitcoin steadied above $60,000, the level it had tumbled to in the prior week’s selloff.

## Looking Ahead This Week

**The peace deal watch.** The biggest story this week may be one that isn’t on any calendar: whether Washington and Tehran actually sign. A deal reopens the Strait of Hormuz and pulls oil, and the whole inflation outlook, lower. A collapse sends both the other way. Watch the oil price; it is the market’s live scoreboard on the odds.

**A new hand at the Fed.** The Federal Reserve meets Tuesday and Wednesday, and for the first time since 2018 a new chair runs the room: Kevin Warsh, at his first meeting. No rate change is expected, but the rest is wide open. With headline inflation at 4.2% and core at a tame 2.9%, the meeting is really an argument over which number to believe, and markets will weigh every word for how fast Warsh would move if the energy spike spreads.

**Japan’s turn.** On Tuesday, the Bank of Japan is expected to lift its rate to 1%, the highest in thirty years and the next step in the slow exit we described last week. The hike is a foregone conclusion; the real question for the yen, still stuck at 160, is whether the bank hints that more will follow. Call it the first test of the case we made for the currency.

**The consumer checks in.** Tuesday’s retail sales report will show whether costlier gasoline is crowding out other spending, the channel through which an oil shock becomes an everything shock. A short week: US markets close Friday for Juneteenth.

## Focus Theme: The Quiet Giant

Most Americans already understand bonds better than they think. A mortgage is a bond seen from the borrower’s seat: a bank lent you a large sum, and every month you send back interest plus a sliver of principal, on a schedule fixed years in advance. Investing in fixed income is simply the same arrangement seen from the opposite seat. Now you are the lender. The payments flow toward you, and when the loan runs its course, your money comes home.

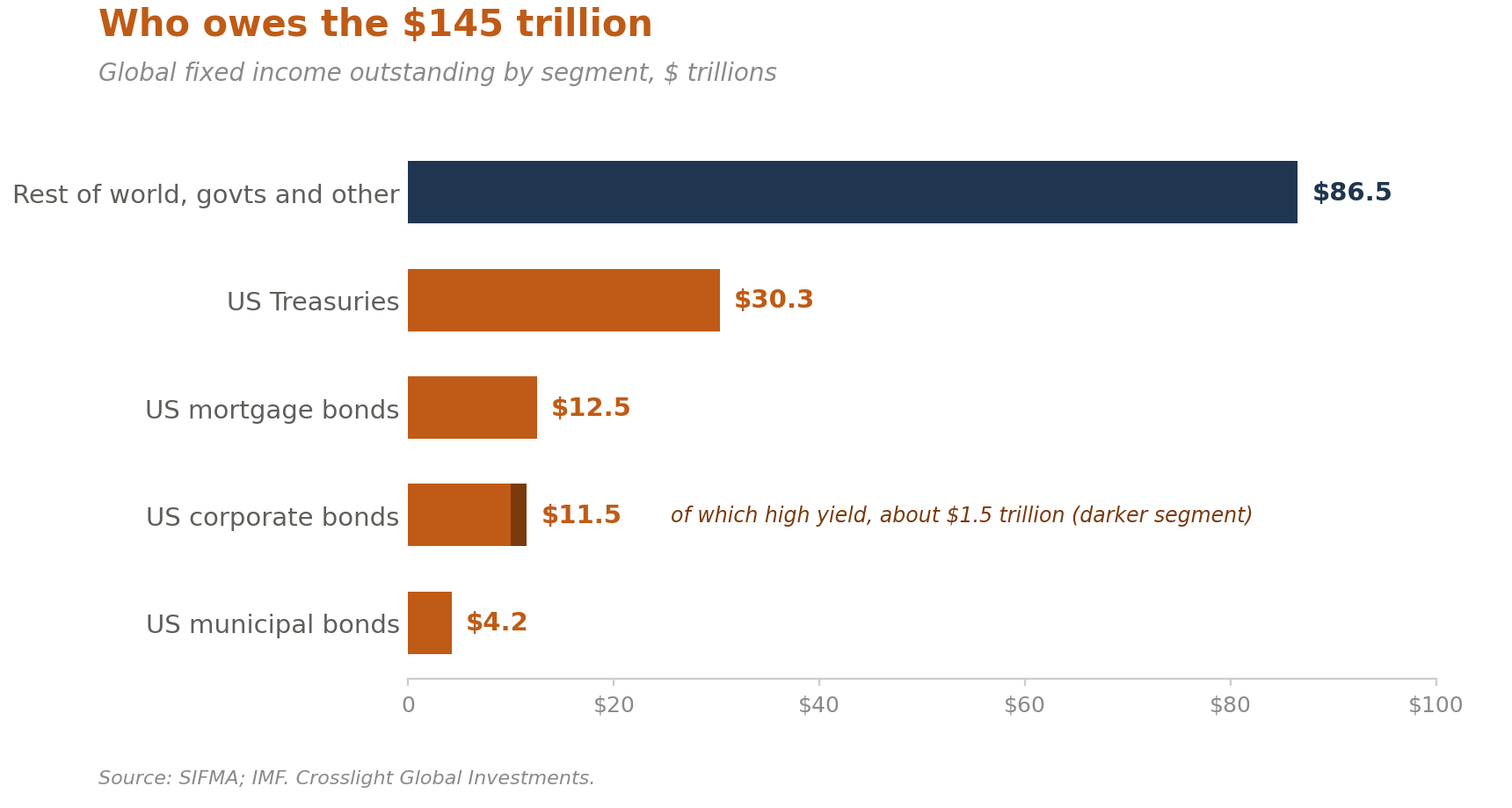

Few people appreciate the scale of this market. The world’s stock markets, the ones that fill the evening news, are worth about $127 trillion. The bond markets are worth about $145 trillion. The largest market on earth is the quiet one, and it finances the noisy one.

So who owes $145 trillion? Start at home. America accounts for roughly 40 percent of the total, and the largest share belongs to Washington: more than $30 trillion in Treasury bonds, issued to cover what taxes do not. American mortgages come next, about $12.5 trillion of home loans bundled into bonds and sold to investors. Your own monthly payment is quite possibly in there, funding a pension somewhere. American companies owe another $11.5 trillion, and roughly $1.5 trillion of that is high yield, the market’s polite term for riskier borrowers who pay extra for the privilege. States, cities, and school districts have borrowed about $4 trillion through municipal bonds, often free of federal tax, to build the roads and water systems beneath your feet. Add it up and America owes close to $58 trillion. The rest of the world owes the other $87 trillion, and there, as in America, governments are the biggest borrowers. Step back from bonds to all the money governments owe, loans included, and public debt worldwide tops $110 trillion, nearly all of it with the G20, and America and China owe about half between them. Fastest-growing of all is the emerging world, where governments and companies together now owe close to $40 trillion. The heaviest borrowing is seen in countries such as Brazil, India, and Indonesia, whose bonds regularly appear in these pages.

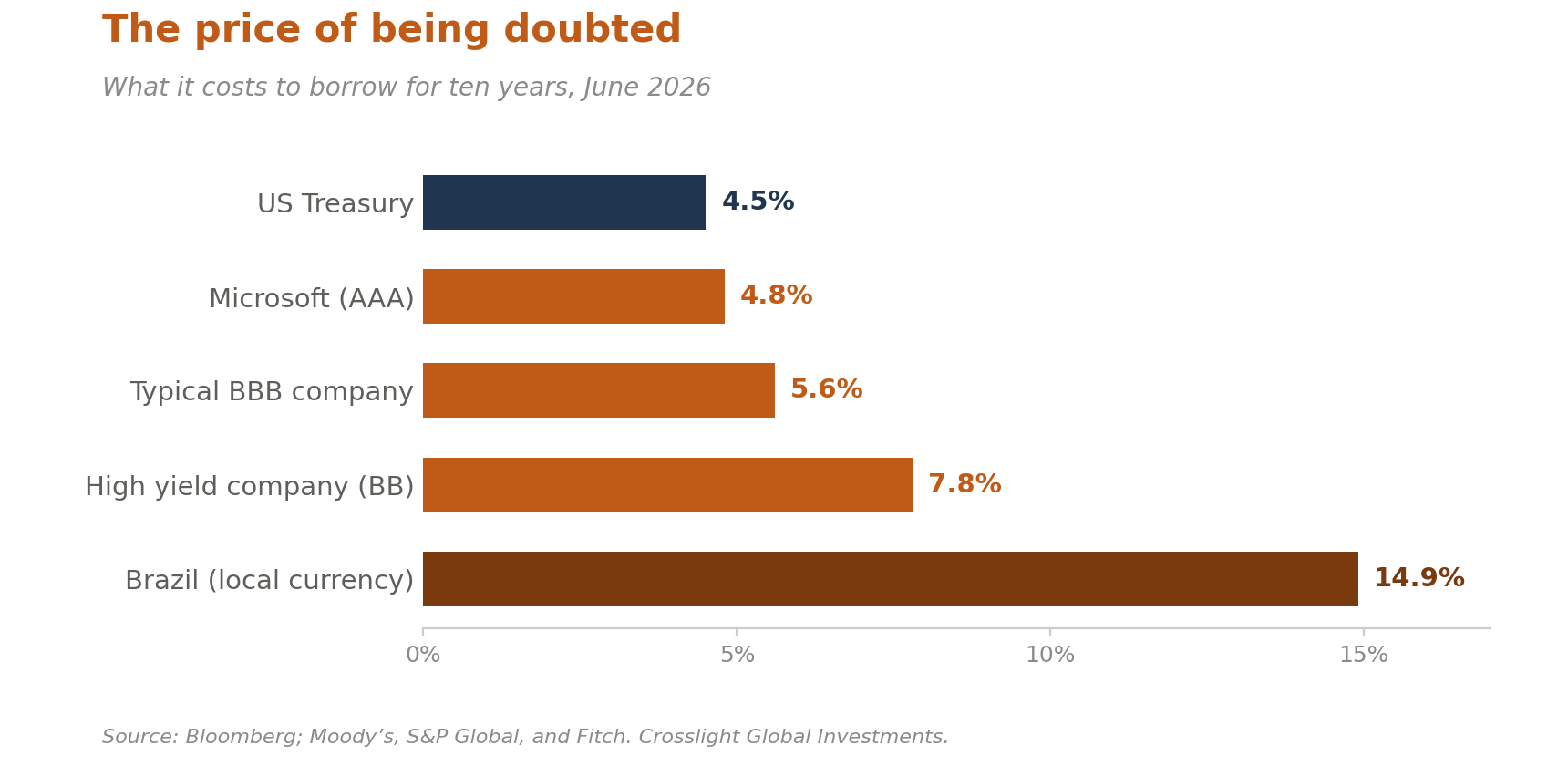

Every lender asks the same question: will I get my money back? When the borrower is you, the answer arrives as a credit score, the three-digit number between 300 and 850 that decides what your mortgage costs. When the borrower is a company or a country, it arrives as a credit rating, a letter grade running from AAA down to D, handed out by agencies named Moody’s, S&P, and Fitch. Same machine, different alphabet. A homebuyer with a 780 score gets a better rate than her neighbor with a 620 score, and the logic carries straight up the food chain to Microsoft and Brazil. The grade is the market’s shorthand for how much doubt is in the room. The interest rate is the price of that doubt.

Watch the price climb as the doubt grows. The US Treasury, with the taxing power of the world’s largest economy behind it, pays about 4.5% to borrow for ten years, less than any other large borrower. Microsoft and Johnson & Johnson, the only two American companies still rated AAA (a grade Washington itself no longer holds), pay only a sliver more. A solid but unspectacular BBB company, at the bottom rung of what the market calls investment grade, pays about a point above the government. A high-yield borrower pays three points more, sometimes much more. And Brazil, whose finances we touched on last week, must offer nearly 15% to borrow in its own currency for a decade. That extra interest exists for one reason: it pays the lender for the added chance that something goes wrong. The bond market offers no free lunch.

The 10-year Treasury now pays about 4.5%. Treat that number as a hurdle, because every other investment you own is competing against it whether you asked it to or not. A stock has to beat 4.5% a year to justify the swings that come with owning it, and it makes no promise that it will. So ask the question plainly: of the stocks in your portfolio, how many are you confident will return more than 4.5% a year, every year, for the next ten? The government will put its 4.5% in writing.

That is the honest case for owning both. Bonds and stocks do different jobs. A stock is an ownership share of a business’s future, and its price swings with every change in the public mood. A bond is a promise with math you can check: this much interest, on these dates, money back at the end. That does not make bonds riskless. The past two weeks proved otherwise, as rising rates marked down the price of existing bonds across the board (rates and bond prices move in opposite directions). But a lender’s losses tend to run shallower than an owner’s, and the income keeps arriving whether the market is cheerful or not.

If you are still working and saving, that steadiness is ballast. An allocation to bonds will not make your 401(k) statement exciting. That is by design. The cushion it provides in the years when stocks fall is what lets you stay invested through them, and staying invested is where most of the long-run return gets earned. We have spent our careers in this market, and the investors we worry about are never the ones who own too many bonds. They are the ones who sell everything in a panic, and a panic does more damage to a retirement than any bear market ever has.

When the working years end, the job changes. A retiree no longer asks her portfolio to grow at all costs. She asks it to send money. A portion of savings shifted into bonds becomes something close to a paycheck: semi-regular payments that cover the groceries and the property taxes without forcing her to sell shares at whatever price the market happens to be offering that month.

None of this is sophisticated, and we mean that as a compliment. Fixed income is the part of investing that behaves most like the rest of your financial life. You have been making these payments for years. At some point, the plan is to start receiving them.

So here is the homework. We are not telling anyone to put 80 percent of their savings in bonds; yields today are fair rather than extraordinary, and the right mix depends on your circumstances and on how well you sleep when markets fall. But most managers we respect agree that stock valuations are stretched, and after the run equities have had, plenty of 401(k)s now hold far more stock and far less fixed income than their owners ever actually chose. Nobody decided that allocation. It built itself, one good year for stocks at a time. Pull up your statement this week and look at the split. If the number surprises you, that is a conversation worth having. You know where to find us.

## Heard Through the Grapevine

**A rocket answered.** Last week we wrote that the warmth of SpaceX’s welcome would say a lot about how much risk investors still have the stomach for. The answer arrived emphatically: up 19% on day one, amid a war scare, in the largest offering ever priced. Take the signal for what it is and no more. One spectacular debut proves the appetite for a great story survives higher rates. It does not prove that every story deserves the price it is asking. The hurdle we describe in this week’s focus theme did not move.

**A new conductor, same orchestra.** Kevin Warsh takes the chair at his first Fed meeting on Wednesday, the first change of leadership at the central bank in eight years. Chair transitions matter more than they should, because markets price not just policy but the person’s instincts, and Warsh arrives with a reputation for worrying about inflation. His opening act is a peculiar one: a 4.2% headline rate that argues for toughness and a 2.9% core rate that argues for patience, with a war that could resolve the difference either way before his second meeting. The polite phrase for this is a full plate.

---

*Thank you for reading Crosslight’s Weekly Perspectives. If you wish to talk through any of these themes, please reply to this note. This note is strictly for informational purposes only and does not constitute investment advice for the reader.*

*Sources: Bloomberg; US Bureau of Labor Statistics May CPI and PPI reports; University of Michigan Surveys of Consumers; Federal Reserve; European Central Bank; Bank of Japan; Japan Ministry of Finance; US Treasury auction schedule; SIFMA Capital Markets Fact Book and Research Quarterly; IMF Fiscal Monitor; Moody’s, S&P Global, and Fitch; Reuters; Financial Times; The Wall Street Journal; CNBC.*

*Copyright © 2026 Crosslight Global. All rights reserved.*