Crosslight Weekly Perspective - June 28, 2026

Selling the Good News: Why Stocks Fell on a Good Week

**Key Takeaways**

- Stocks fell last week even though the news was mostly good. After a long climb, investors decided shares had simply risen too far, too fast.

- The economy still looks sturdy, and the inflation scare is fading. Even so, the Federal Reserve shows no hurry to cut interest rates.

- With the immediate worries easing, the market’s attention is turning to the slower-moving problems that will shape the rest of the year.

## MARKET RECAP: Selling the Good News

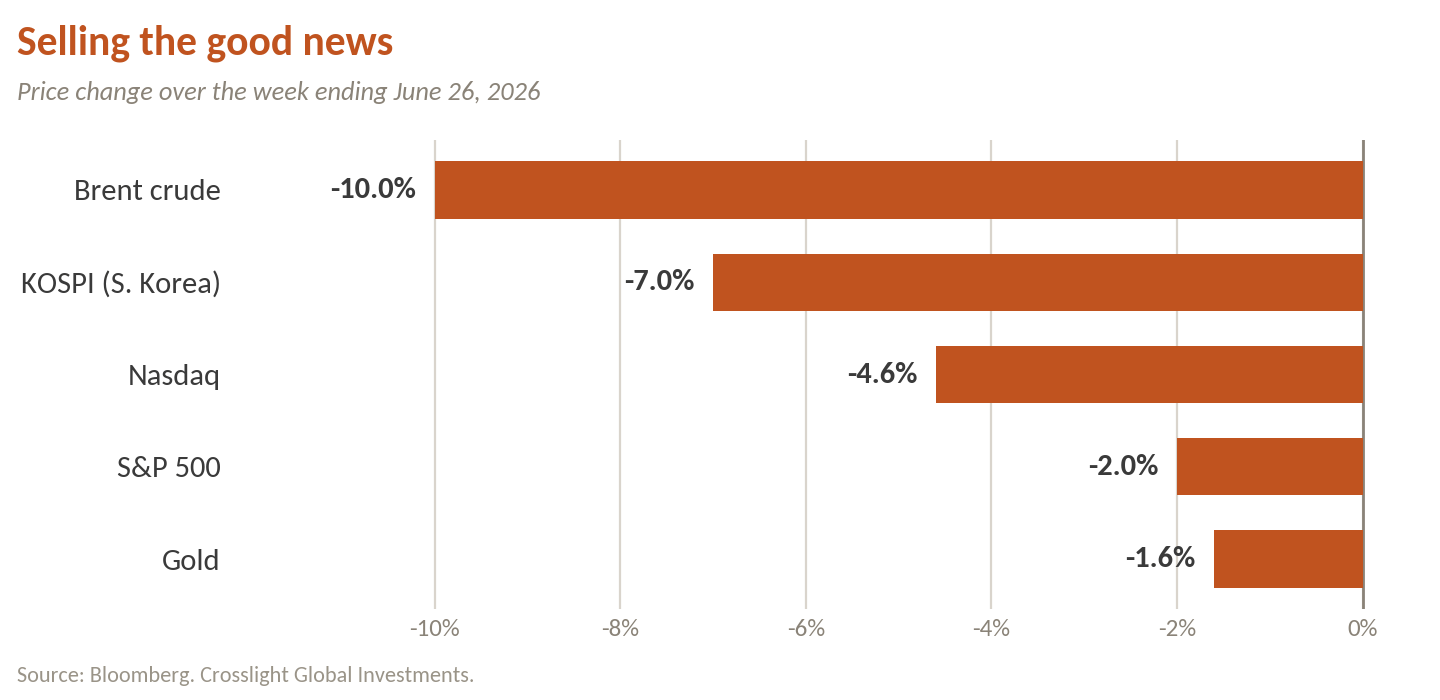

Something odd happened last week. Almost everything that was supposed to cheer investors actually arrived. A shooting war in the Middle East gave way to a truce. Oil, which usually spikes when the region flares up, kept falling. The economy put up strong numbers. And still, stock markets around the world sold off. The Nasdaq, an index packed with technology companies, dropped 4.6%, repeating a slide it had suffered in the first week of June.

The simplest explanation is the oldest one. After a long run, prices had climbed further than the underlying companies were worth, and at some point a crowd that has been buying decides it is time to sell. But three forces gave the selling its shape.

**The Fed is in no mood to cut.** Investors spent the week coming to terms with a Federal Reserve, now led by Kevin Warsh, that cares more about taming prices than about pleasing markets. Most members of the committee that sets interest rates look set to hold them steady for the rest of the year, and an increase, while unlikely, is no longer unthinkable. High interest rates are hard on almost everything, because they let safe, dull savings pay well enough to pull money away from riskier bets. Gold is the clearest example. It pays its owner nothing to hold, so when a government bond pays a healthy return, gold loses its appeal. Its price has fallen 25% from the record it set in late January. A quieter worry sits alongside this. Private credit, which means lending to companies arranged outside the traditional banking system, ballooned in the years when borrowing was cheap. Now the investors who put money in are asking for it back faster than expected, and that corner of finance bears watching.

**Summer selling, and a wave of new stocks.** Part of the drop was simply mechanical. “Sell in May and go away” is an old market saying: trading thins out over the summer as professionals take their holidays, and thin trading can make any move larger than it would otherwise be. The Nasdaq is also handing back some spectacular recent gains. It rose 15.3% in April and another 8.4% in May, and gains that steep rarely hold. There is a further wrinkle. After SpaceX’s debut, a long line of large technology companies is preparing to sell shares to the public for the first time. When big new stocks arrive, investors often sell what they already own to make room, and the most widely held giants tend to feel it first. Those giants, the so-called Magnificent Seven that led the market for years, have been anything but magnificent in 2026. All seven have trailed the Nasdaq this year, and three of them, Microsoft, Meta and Tesla, have actually fallen.

**Politics, at home and abroad.** The last force is politics. Markets welcomed the 60-day truce between the United States and Iran signed on June 17, but events since then do not point to a lasting peace. Trade is unsettled too. On July 1 the three members of the USMCA, the trade pact binding the United States, Canada and Mexico, begin a formal review of the agreement. Few expect it to collapse, but the three governments want different things, and that disagreement could weigh on North American trade for years. On Friday, President Trump threatened a 100% tariff on European countries that tax digital services, a charge widely read as aimed at American technology firms. And early in the week China placed new export restrictions on ten American companies, cutting off their supply of rare earth elements, the specialized metals used in everything from electric motors to missiles.

**Stocks.** The S&P 500, a broad measure of large American companies, fell for five days straight to end the week down almost 2%. The wildest ride was in South Korea, whose market is heavy with technology shares. A drop of 8% or more during the trading day tripped the country’s automatic “circuit breakers,” which pause trading to let nerves settle, three separate times. The KOSPI index ended the week down more than 7%. Even so, it remains the year’s best performer, having roughly doubled since the end of 2025.

**Bonds.** Government bonds steadied after the previous week’s rough patch. The interest rate on the ten-year US government bond, the number that quietly sets the cost of mortgages and company borrowing, slipped to 4.37%, its lowest in two months. (When a bond’s interest rate falls, the bond itself becomes worth more, so anyone already holding it gains.) The reopening of the Strait of Hormuz, the narrow shipping lane that carries much of the world’s oil, eased fears about inflation and pulled Germany’s ten-year rate down to 2.85%. Cheaper oil helped developing countries too, with Brazil’s ten-year borrowing rate falling to 14.5%.

**Currencies.** The US dollar kept climbing as nervous investors looked for a safe place to park their money. A widely watched gauge of its strength stayed above a key threshold for eight days running, the longest such stretch since May 2025. The currencies that swing hardest with the global mood suffered most, with Norway’s krone down 2.3% and the Australian dollar down 1.7%. The Japanese yen slipped a little further, to 161.75 per dollar, with traders watching closely for any sign that Tokyo will step in to defend it.

**Commodities and crypto.** Raw materials had another slow week, though precious metals drew a few buyers back by Friday. Gold dipped briefly below $4,000 an ounce before settling at $4,089, down 1.6%. Brent crude, the global benchmark for oil, plunged more than 10% to $72 a barrel, erasing the entire price jump the war had caused since February 28. Bitcoin slid below $60,000, more than 50% beneath the record of about $125,000 it reached last October.

## LOOKING AHEAD THIS WEEK

**Economic data.** This week’s focus is centered on the June non-farm payroll gains (Thurs), which is expected to moderate to a four-month low of 115,000. Two forward-looking indicators will provide a first glimpse into the economic impact from the easing Middle East conflict. The manufacturing ISM (Wed) likely stayed broadly unchanged at 53.9 in June, while the Consumer Board index of consumer confidence (Tue) is forecast to rebound to an 8-month high of 94.6 in June. In the EU, consumer price inflation (Wed) probably moderated to 3.0% YoY in June, helped by a decline in Brent crude prices. In Asia, the June PMIs for multiple countries, including China, South Korea and Taiwan, will provide further clues to the second-half growth outlook for the region.

**Central bank watch.** Two Fed speeches are worth noting in the week ahead. On Wednesday, Fed chair Kevin Warsh will participate in the annual ECB forum in Portugal, his first public engagement since the FOMC meeting in mid-June. The forum will also feature central bank heads from the ECB, the UK and Canada. On Thursday, San Francisco Fed President Mary Daly will participate in a moderated discussion in Spain. Elsewhere in EM, Colombia’s central bank (Tue) is expected to raise the policy rate by 50 bps to 11.75%, a two-year high.

---

*Thank you for reading CrossLight’s Weekly Perspectives. If you wish to talk through any of these themes, please reply to this note. This note is strictly for informational purposes only and does not constitute investment advice for the reader.*

**Sources (suggested, edit to match your desk):** Bloomberg; Federal Reserve; US Bureau of Labor Statistics (non-farm payrolls); Institute for Supply Management (ISM); The Conference Board (consumer confidence); Eurostat (EU inflation); S&P Global PMIs; Bank of Japan; Banco Central do Brasil; Banco de la República (Colombia); European Central Bank; Reuters; Financial Times; The Wall Street Journal; CNBC; Clifford K. Berryman, “Path to Peace,” The Evening Star, 1946, U.S. National Archives (NAID 6012362, public domain).

*Copyright © 2026 CrossLight Global. All rights reserved.*