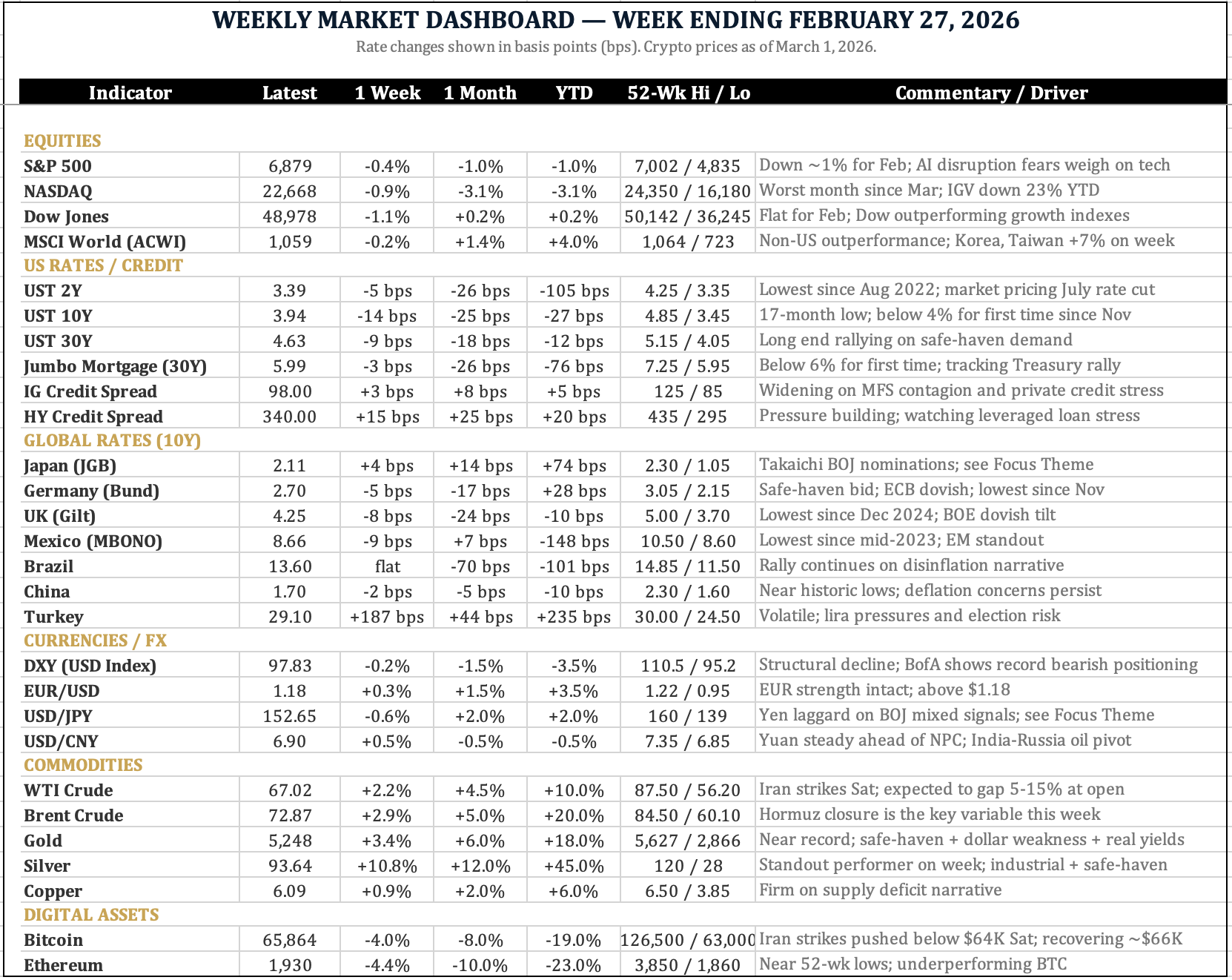

Crosslight Weekly Perspective - March 1, 2026

Japan Was Where Yields Went to Die: The BOJ owns half its bond market. As Japanese yields wake from a generation-long sleep, the repatriation of capital could ripple across global markets.

### KEY TAKEAWAYS

- US-Israeli strikes killed Iran’s Supreme Leader; Iran retaliates across the Gulf; Strait of Hormuz effectively closed — oil expected to gap 5–15% at Sunday’s open

- Bonds rallied hard despite hot inflation data, with the 10-year falling below 4% for the first time in four months. Stagflation risk is now the central debate

- Gold, silver, and Treasuries are catching the safe haven bid; equities, crypto, and credit are not

### MARKET RECAP

Markets were already in risk-off mode before Saturday’s events in Iran. Bonds rallied, US equities sold off, and credit stress emerged across multiple corners of the market.

- The 10-year UST yield fell 14 bps to 3.94%, a 17-month low despite a January PPI print that came in far hotter than expected (core +0.8% vs. 0.3% consensus). That disconnect tells you where the fear is: not inflation, but growth. For the month, the 10-year dropped roughly 25 bps, its strongest February rally in a year. Mexico’s 10-year MBONO hit its lowest level since mid-2023.

- The S&P 500 slipped 0.4% on the week, finishing February down about 1%. The Nasdaq lost over 3% for the month, its worst showing since March, dragged down by AI disruption fears after Block announced plans to cut nearly half its workforce, and by CoreWeave’s guidance, which sent shares down 20% on Friday. The tech-software ETF (IGV) is now down 23% year-to-date. Meanwhile, non-US markets outperformed decisively: the UK gained 2.1%, and South Korea and Taiwan each surged over 7% to new all-time highs after the Lunar New Year break.

- In commodities, gold rose 3.4% and silver surged 10.8%, both on safe-haven demand. Brent crude closed Friday at $72.87, up 2.2%, already pricing in elevated Gulf risk. Bitcoin fell to roughly $64,000, now down 21% on the year.

**Iran**

Late Saturday, the United States and Israel launched coordinated strikes on Iran, killing Supreme Leader Ali Khamenei. The US deployed B-2 stealth bombers and sank nine Iranian naval vessels. An interim three-person leadership council, President Pezeshkian, judiciary chief Mohseni Ejei, and cleric Alireza Arafi, has been appointed to govern until the Assembly of Experts selects a successor. Iran retaliated with missiles and drones targeting Israel and US bases in Bahrain, Kuwait, and Qatar. Most were intercepted; one struck near Jerusalem, killing at least nine. Three US service members were killed. Iran’s navy has reportedly closed the Strait of Hormuz to commercial shipping, the passage that carries a fifth of global oil supply. Dozens of vessels are clustered at the Strait’s entrance, and Middle Eastern airports in Abu Dhabi, Dubai, and Doha have suspended operations. Analysts expect Brent to open 5–15% higher Sunday evening, putting the $77–84 range in play. OPEC+ announced a 206,000-bpd output increase from April, but the math is straightforward: if oil can’t move through Hormuz, incremental supply doesn’t matter. War-risk insurance premiums are spiking, and some underwriters may refuse cover for US- and Israel-linked vessels altogether. The UN Security Council convened an emergency session. Guterres warned of an uncontrollable escalation. Rubio speaks with G7 counterparts on Sunday.

### LOOKING AHEAD THIS WEEK

The Iran conflict will dominate this week. The immediate questions: will the Strait of Hormuz reopen, will Iran’s interim leadership escalate or stabilize, and will Congress move to constrain presidential authority for further military action? On the macro calendar, the main US releases are non-farm payrolls (consensus 60k, Friday) and ISM Manufacturing (consensus 51.5, Monday). Both will be read through the stagflation lens: inflation running hot, growth softening. In China, the annual National People’s Congress begins on March 5, focusing on economic targets and the five-year plan through 2030. For allocators, the convergence of geopolitical shock, energy disruption, sticky inflation, and weakening growth creates a uniquely difficult environment. The Treasury rally may extend as safe-haven flows accelerate. Gold is positioned to benefit from compounding tailwinds: dollar weakness, geopolitical risk, and compressed real yields. The oil risk premium, which had been building gradually, now faces a step-change.

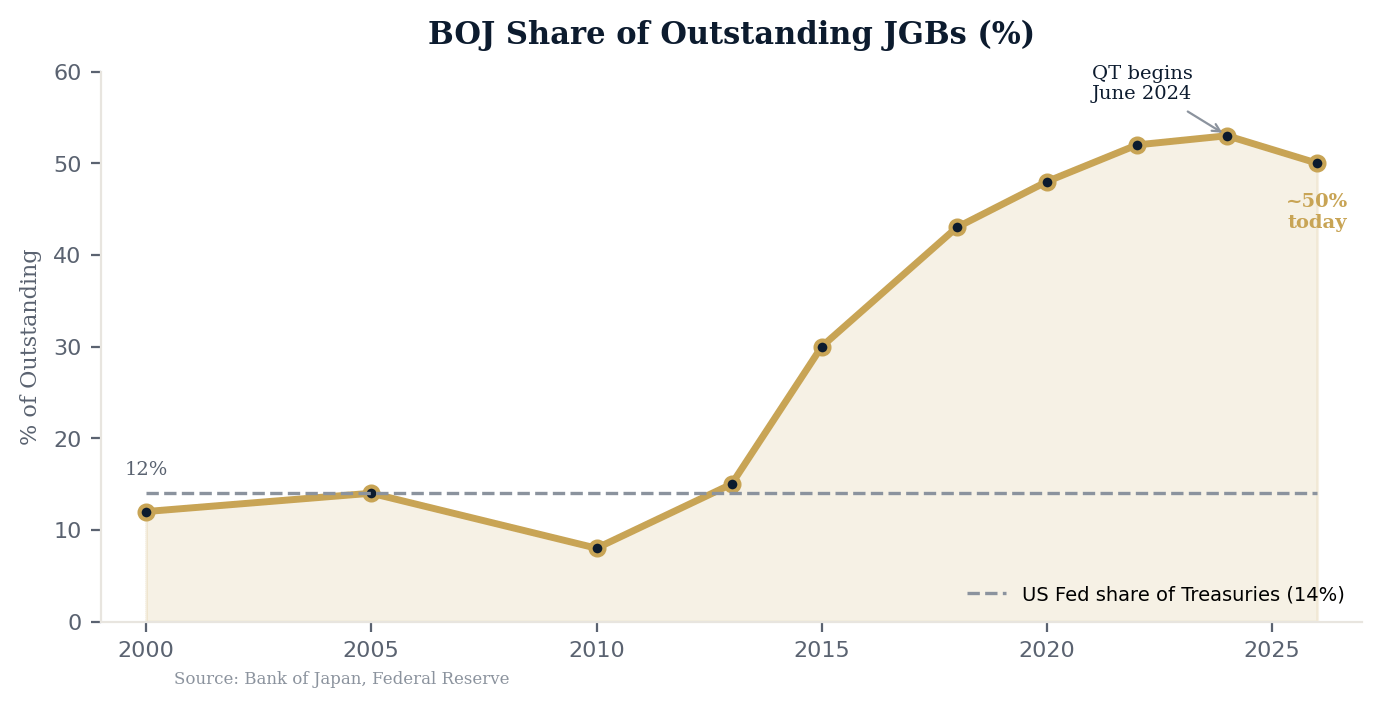

### FOCUS THEME: Japan - The Land of the Rising Yields

For decades, Japan was the place where interest rates went to die. The Bank of Japan held rates at or below zero for much of a generation, and Japanese government bonds yielded so low that global investors largely ignored them. That era is ending, and the implications extend well beyond Tokyo. The catalyst is political. Prime Minister Sanae Takaichi, fresh off a landslide election win in February, nominated two pro-growth academics to the BOJ’s nine-member board, a signal that she intends to keep fiscal policy loose even as the central bank inches toward tighter money. It’s a familiar tension: a government that wants to spend versus a central bank that wants to normalize. Friday’s Tokyo CPI surprise (1.6% YoY vs. 1.4% consensus) only sharpened the debate. The numbers behind this story are striking. The BOJ currently owns roughly half of all outstanding Japanese government bonds — up from just 12% in 2000. By comparison, the US Federal Reserve holds about 14% of outstanding Treasuries. No major central bank in the world is this deeply embedded in its own sovereign debt market.

After ending its sub-zero rate regime in 2023, the BOJ has raised rates four times to 0.75% — the highest in 30 years. But that’s still well below the US (3.50–3.75%) and Europe, which is why the yen remains weak despite two rounds of currency intervention in 2022 and 2024. Market chatter of a coordinated US-Japan intervention in January 2026 kept the yen from breaching 160, but the pressure hasn’t gone away.

Three things to watch as Japanese yields continue to rise:

**The money is coming home.** Japanese banks, pensions, and insurers spent the past decade buying foreign bonds, particularly US Treasuries, in search of yield they couldn’t find at home. Higher domestic yields will reverse that trade. As offshore holdings mature, expect a gradual repatriation into JGBs. The good news for currency markets: most of those foreign positions are hedged, so the yen impact should be muted.

**Foreign investors are paying attention again.** After years of apathy, overseas investors poured JPY 6 trillion ($39 billion) into JGBs in January alone, the second-largest monthly inflow on record. New cross-border collateral agreements with Southeast Asian nations have made JGBs more useful as financial plumbing. The trade-off: more foreign ownership means more volatility when global sentiment shifts.

**The interest bill is getting expensive.** Japan’s debt-to-GDP ratio stands at 240%, the highest in the world, roughly double that of the US (120%) and nearly four times that of Germany (64%). Rising yields on that debt pile translate directly into higher servicing costs, which makes Takaichi’s fiscal expansion plans harder to sustain. The market will eventually demand a credible plan for medium-term debt sustainability. Whether this government delivers one is an open question.

**The bottom line:** Japan’s bond market is waking up after a long sleep. For global investors, that means a new source of yield, a new source of volatility, and a potential catalyst for capital flows that could ripple across Treasury markets, currency pairs, and portfolio allocations. We’ll be watching this closely.

### HEARD THROUGH THE GRAPEVINE

**Niall Ferguson: Khamenei Joins Saddam in Hell, but Iran 2026 Is Not Iraq 2003 (The Free Press)**

Niall Ferguson argues that the joint U.S.-Israeli strikes on Iran, including the reported killing of Ali Khamenei, are fundamentally different from the 2003 invasion of Iraq. He contends that the objective is “regime alteration,” not full-scale regime change or nation-building, and that there is no plan for a prolonged ground war. While acknowledging risks such as regional escalation and oil shocks, Ferguson believes the operation is designed to be short, heavily concentrated, and strategically limited, though it unfolds against the broader pressures of Cold War II with China and Russia.

**America’s trade chaos is just beginning (The Economist)**

The article argues that although the Supreme Court struck down Trump’s use of emergency powers to impose sweeping tariffs, the practical effect may be prolonged uncertainty rather than relief. By pivoting to other statutory tools such as Section 122—and potentially Sections 301 and 232—the administration is set to keep tariffs in flux, triggering further legal battles, refund disputes over roughly $180bn in duties, and continued policy whiplash for businesses and trade partners. Even if some refunds and marginally lower rates act as short-term stimulus, the deeper impact is sustained uncertainty that deters investment and hiring, ensuring trade turbulence persists through Trump’s term and likely beyond.

**Markets are churning furiously beneath the surface (The Economist)**

The S&P 500 may appear stable near record highs, but beneath the surface, markets are experiencing an intense rotation as AI forces investors to reassess business models across sectors. Software and tech borrowers have been hit hard, credit spreads in tech have widened sharply, and private credit and leveraged loan markets are showing signs of stress, while “HALO” stocks and AI hardware firms have rallied. With stock dispersion near decade highs and uncertainty about AI’s true economic impact unresolved, the article warns that volatility could intensify—especially if credit conditions tighten or AI expectations prove either overly optimistic or deeply disruptive.

**China piles pressure on Japan after Takaichi Sanae’s triumph (The Economist)**

The article describes a deepening standoff between China and Japan following Prime Minister Takaichi Sanae’s hawkish stance on Taiwan and defense policy, prompting Beijing to impose targeted curbs on rare-earth exports and to exert pressure on tourism. Takaichi has leveraged the confrontation to strengthen her domestic position and push military reforms, while China has framed her as a nationalist threat and signaled economic leverage without triggering full-scale retaliation. With both sides escalating cautiously through trade restrictions, military posturing, and maritime activity, the dispute risks becoming a prolonged strategic rivalry with significant supply-chain and regional security implications.

**Trump’s Doctrine in Iran and Beyond (The Wall Street Journal)**

Seth Cropsey argues that the U.S.-Israeli strike on Iran crystallizes a coherent “Trump doctrine” that applies tailored, overwhelming force against exposed partners of Russia and China to strengthen deterrence. He contends that targeting Iran after similar pressure on Venezuela and Cuba undercuts rival great powers while reinforcing U.S. credibility and military primacy. Cropsey maintains that sustained sanctions, precise strikes, and regional leverage could trigger systemic collapse in Tehran, framing decisive action as the surest path to long-term peace through restored deterrence.

### MARKET DASHBOARD

Thank you for reading CrossLight’s Weekly Perspectives. If you wish to talk through any of these themes, please reply to this note. This note is strictly for informational purposes only and does not constitute investment advice for the reader.