Crosslight Weekly Perspective - March 22, 2026

Leverage Doesn't Amplify Returns. It Amplifies Decay: Retail is piling into 2x and 3x energy ETFs. In a flat, volatile tape, a sideways index can still leave leveraged holders down 18–30%.

### KEY TAKEAWAYS

- No place to hide for investors amid prolonged uncertainty, given the US-Iran deadlock

- Limited scope for stimulative policies hints at downgrades to 2026 global growth

- Keep bond exposure to the front end, given intensifying inflation fears

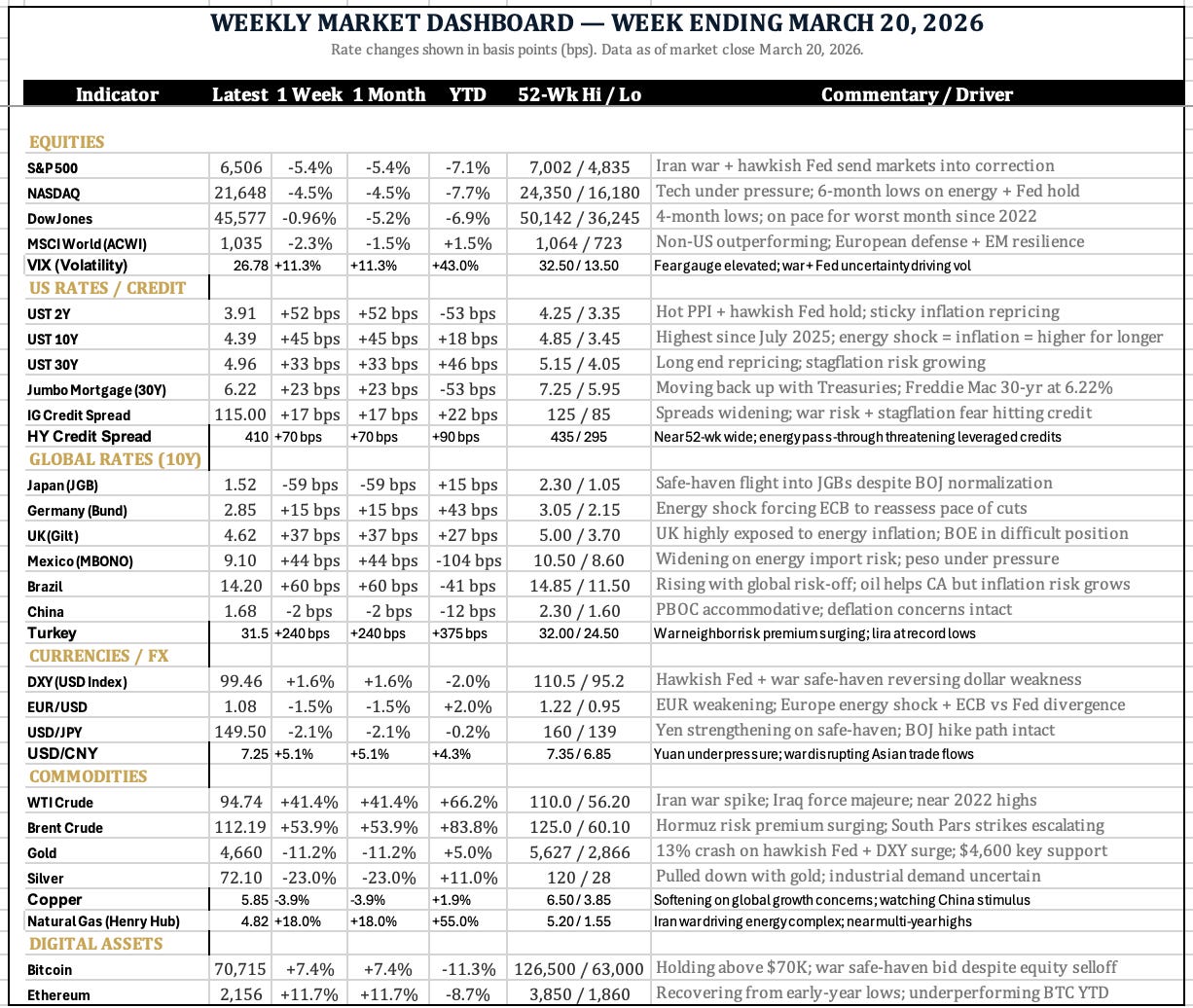

### MARKET RECAP: THE STRIKE PRICE

Portfolio derisking continued unabated for a third straight week. There was no place to hide as the Gulf conflict exerted a toll across asset classes. However, S&P futures rose 0.8% after Friday’s market close, as President Trump suggested a possible winding down of US operations against Iran. But continued military activities over the weekend cast doubt on an imminent resolution on both sides.

- US equities held up comparatively well, with the S&P down 1.9%. European bourses were the main underperformers — Germany fell nearly 5% on oil exposure. Asian markets were mixed: China and Japan lost 2%, while South Korea and Singapore gained 5.4% and 2.2%.

- Rising energy costs weighed on bonds globally. The 10-year Treasury rose 10 bps to 4.38% — an eight-month high — on the Fed’s hawkish hold and a hot PPI print. UK gilts bore the brunt: a 17 bp spike took the 10-year to 5%, a 17-year high and the highest in the G7.

- The dollar softened after two weeks of gains. The euro led, up 1.4% on the ECB’s hawkish hold; the Norwegian krone gained 2.1%. Asian currencies lagged — the rupee, peso, and baht each fell more than 1%.

- Commodities remained bifurcated. Brent gained nearly 9% vs. WTI’s 1.4%, widening the spread to $14. Precious metals continued to sell off despite war fears — likely technical after the November–January rally — with gold down over 10% and silver tumbling nearly 16%.

### LOOKING AHEAD THIS WEEK:

The main factor remains the Gulf conflict. Any change in diplomatic signals or new military escalation will influence oil prices first and everything else second. Markets end the week pricing in a 45% chance of a Fed hike by October, a sharp reversal from last week’s 70% probability of a cut. That re-pricing is how every data release this week should be interpreted.

**Flash PMIs (Tuesday — US, Eurozone, UK, Japan)** are the week’s most market-sensitive scheduled data. Forecasts cluster around 51.5–52.0 for the US composite, signalling modest expansion, but any reading showing manufacturing contracting under energy cost pressures will accelerate the growth-downgrade narrative and hit equities. European PMIs carry extra weight given the region’s exposure to oil.

**UK CPI (Wednesday)** arrives with gilts already at a 17-year high. A hotter-than-expected print would put the BOE in an impossible position — energy-driven inflation on one side, a slowing economy on the other — and push the 10-year yield toward 5.25%. Watch the services component closely.

**Japan CPI (Friday)** will determine whether an April BOJ hike remains on the table. The BOJ held at 0.75% in March but upgraded its inflation forecasts; a strong print reinforces the case for the next move and could strengthen the yen further.

**Fed Chair Powell speaks Sunday (already in play).** His tone on whether the Iranian energy shock is “transitory” or a durable inflation threat will set the tone for the week. Markets are listening for any signal that hikes are back on the table.

**Banxico (Thursday)** is a closer call than it appears. The bank paused its easing cycle in February at 7.00% as core inflation stayed stubbornly above 4%. Higher oil prices now complicate any resumption of cuts. A hold is more likely than the market expects.

**Private credit stress (ongoing).** BCRED’s $3.7 billion in Q1 redemption requests — exceeding its 7% quarterly cap — is the slow-moving story with potential for sudden acceleration. Blackstone is simultaneously marketing a new private credit CLO. Watch for further withdrawal announcements from other managers; Morgan Stanley and Cliffwater already moved this month. If retail contagion takes hold, the spillover to leveraged loan markets and HY spreads could be significant.

**US-China trade (background risk).** Trump’s postponement of the Beijing summit removes a potential catalyst for de-escalation. With markets already under pressure, the absence of any positive trade signal is itself a headwind.

### FOCUS THEME: THE LEVERAGE TRAP IN A VOLATILE MARKET

About $8.4 billion has moved into oil and energy ETFs year-to-date. XLE alone just posted its two largest monthly inflows on record in January and February. Retail is leaning into the conflict trade, and a meaningful portion of that is being expressed through leverage.

What’s getting far less attention is what happened just before this shift. In January, leveraged equity ETFs saw $7 billion in outflows, the largest monthly redemption on record. That wasn’t random. It was positioning. As the market we’ve been in since late 2022 began to change, institutions stepped back.

For most of the past three years, the environment rewarded leverage. Trends were steady, volatility was low, and buying dips worked. That backdrop is no longer in place. The transition has been subtle, but the behavior of more experienced capital has already begun to adjust. Retail, for the most part, has not.

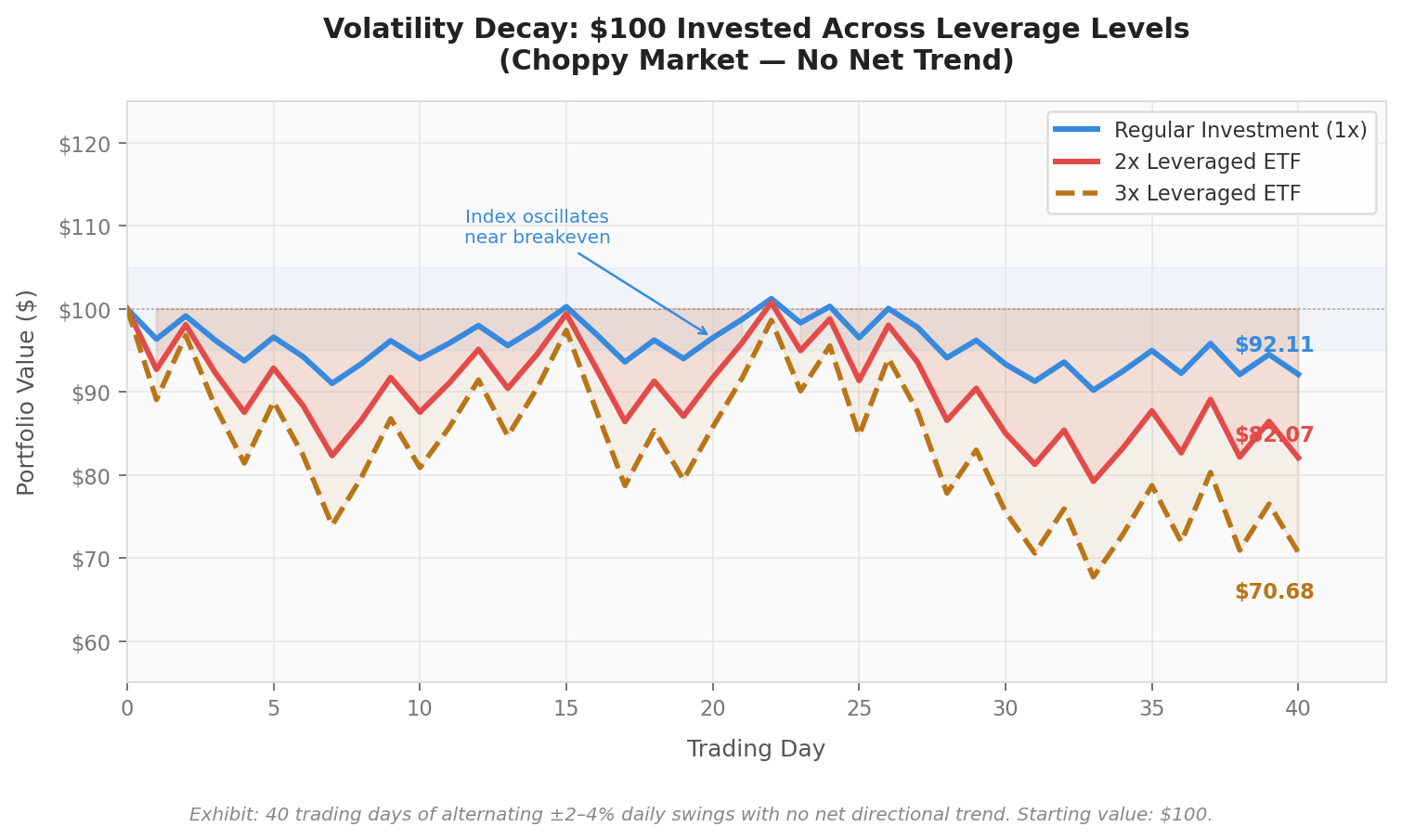

The issue comes down to how these products actually work. Leveraged ETFs reset daily. They are built to deliver a multiple of each day’s move, not the move over time. In a trending market, that distinction doesn’t show up in a meaningful way. In a choppier market, it does, and it compounds.

That’s where volatility decay becomes real. If the market rises 10% and then falls 9.09%, it’s back to where it started. A 2x ETF isn’t. You’re down roughly 1.8%. Stretch that out over a few weeks of back-and-forth trading, driven by headlines and shifting expectations, and the drag adds up quietly.

No single move stands out. But the result is consistent erosion of capital.

*In a flat but volatile market, leverage does not amplify returns — it amplifies decay. A $100 investment subject to alternating ±2–4% daily swings over 40 trading days ends at $92.11 with no leverage, $82.07 in a 2x ETF, and just $70.68 in a 3x ETF, despite the underlying index going nowhere.*

That’s the setup today. Volatility is elevated. Direction is unclear. And a single headline — geopolitical or policy-driven — can reverse markets intraday. This is the environment where leverage works against you, not for you.

The more sophisticated money has already adjusted. The flows reflect that.

So the question for investors stepping into 2x and 3x energy products right now is straightforward: what exactly are you owning?

You’re not owning oil. You’re taking on daily exposure to it, with a structure that resets against you in volatile conditions.

If the underlying view is that markets recover as tensions ease, there are cleaner ways to express that. Standard index exposure does the job without introducing the same drag.

Leverage has its place. It works when the direction is clear and the time horizon is short.

Right now, neither condition is in place.