Crosslight Weekly Perspective - March 8, 2026

Beware the Ides of March: A Gulf war, a closed Strait of Hormuz, and stagflation in view. Our base case — the conflict drags on — argues for quality duration, gold, and geographic diversification.

### KEY TAKEAWAYS

- Gulf War accentuates trade fragilities, posing downside risks to global growth

- Technical positionings and leverage unwind dominate as short-term market movers

- Elevated geopolitical uncertainties support the case for geographical diversification

*

Think political hardball is new? In 1903, a cartoon blasted Theodore Roosevelt for supporting Panama’s split from Colombia, paving the way for the Panama Canal. History has a longer memory than we sometimes do.

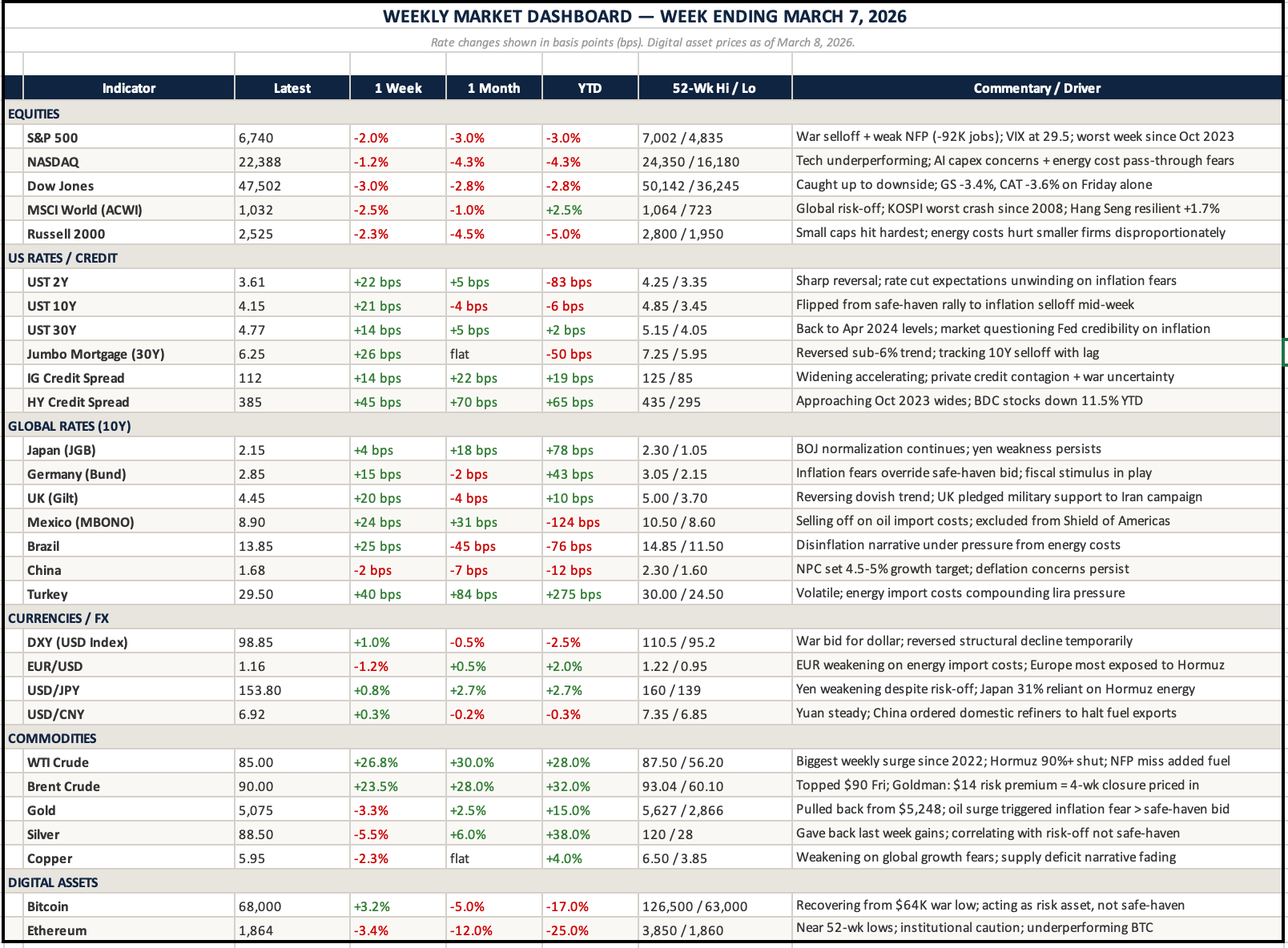

### MARKET RECAP

Global risk assets fell sharply due to military conflict in the Gulf, as the US-Israel strike on Iran expanded to affect neighboring countries, potentially causing significant disruption to global growth.

- Unsurprisingly, global equities were all down. The most notable decline was in stock markets outside the US, with Korea dropping 11.5% after a recent strong run, while Japan and Taiwan both fell 5%. European markets closed the week down by 6-7%, compared to a 2% drop in the S&P.

- The US dollar strengthened on safe-haven demand, with the DXY rising roughly 1% to a six-week high. Emerging market currencies underperformed, led by the South African rand (-3.7%) and the Mexican peso (-3.2%). Among major currencies, the euro and yen fell 1.6% and 1.1%, respectively, but the Canadian dollar rose 0.5% against the dollar.

- In the bond market, US Treasuries weakened across all maturities due to inflation concerns fueled by rising oil prices, with the 10-year yield ending the week 20 basis points higher at 4.14%. However, Friday’s weak jobs report provided some relief for short-term bonds with 1–2-year maturities.

- Commodities had a mixed week. Oil prices soared amid heightened risks in the Gulf: Brent crude jumped 23.5%, while WTI surged nearly 27% — the biggest weekly move since 2022. Gold and silver didn’t attract safe-haven buying, likely due to the unwinding of leveraged positions; gold fell 3.3%, and silver declined 5.5%.

### LOOKING AHEAD THIS WEEK

The Strait of Hormuz remains closed. That single fact changes everything this week. Brent above $85 is no longer a headline; it’s just part of the overall cost. Every day those shipping lanes stay shut, the damage grows. Refiners reroute. Insurers adjust prices. The impact on what consumers actually pay becomes harder to undo. The question has shifted from who controls Tehran to a harsher reality — how many weeks of disrupted oil flows before the economy starts to break down?

CPI drops on Wednesday. The consensus is 2.5%, but that’s a February figure — a snapshot from before the world changed. Nobody will trade based on what it says. Instead, they’ll focus on what March and April look like, with energy costs re-pricing underneath everything. Powell speaks on Thursday, and the conversation has shifted completely. We’re no longer debating when the Fed will cut; now we’re questioning whether they can cut at all this year. Retail sales on Tuesday offer one last clear look at the American consumer before the shock wave hits.

If you’re managing capital or running a business, this is the week when your planning assumptions start to fall apart. Gold isn’t just a hedge right now — it’s a bet on everything that’s unresolved. Geopolitical risk, policy paralysis, and real yields remaining flat. Credit spreads are widening, and it’s not speculation driving that. Energy isn’t just a sector call anymore; it’s the factor that revalues everything else. This week’s advantage goes to those who positioned themselves before the crisis, not to those still waiting for things to settle down.

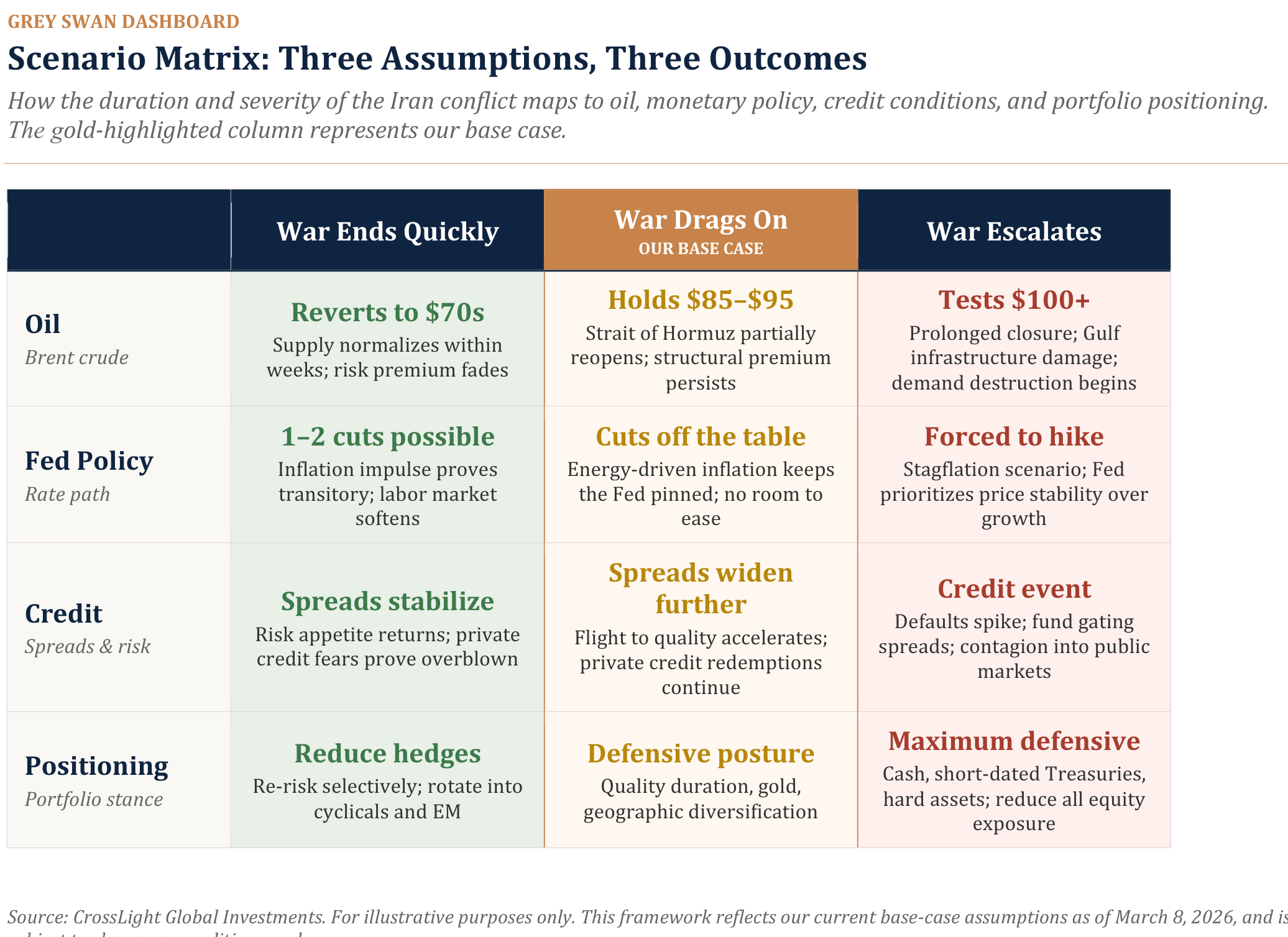

### FOCUS THEME: Beware the Ides of March

The situation in the Middle East is moving fast, and the range of outcomes is wide. Rather than pretend to know how this ends, we’ve built our strategy around three working assumptions. If even one proves correct, the implications for portfolios are significant. If all three hold, we’re looking at a fundamentally different investment landscape for the rest of the year.

**The war drags on.** The administration initially talked about four to five weeks. That timeline is already under pressure. Khamenei was killed on day one, but the Iranian military has proven more durable than expected; a decentralized command structure and a cheap, effective drone arsenal have kept the regime in the fight. Talk of US ground troops changes the calculus entirely. Once boots hit the ground, the historical parallels shift from Gulf War I to Iraq and Afghanistan. Neither ended quickly. Neither ended well.

**The conflict spreads.** What started as a joint US-Israeli air campaign now touches more than a dozen countries. The UK, France, and Greece have pledged military support. Russia is reportedly feeding Tehran intelligence on US positions. An Iranian warship was sunk by a US submarine off the coast of Sri Lanka — a development that risks pulling South Asia into the equation. This is no longer a contained regional operation. It’s being drawn into the gravitational pull of a much larger conflict.

**The global economy tilts toward stagflation.** Energy infrastructure across the Gulf has sustained real damage. The Strait of Hormuz remains effectively closed, choking off roughly one-fifth of the world’s oil supply. Brent has crossed $90. These aren’t transitory disruptions; they’re structural until proven otherwise. The Fed, which entered the year expected to cut rates, may now have no room to act at all. In a worst-case scenario, central banks could be forced to hike into a weakening economy. That’s the textbook definition of stagflation, and it’s no longer a tail risk.

### HEARD THROUGH THE GRAPEVINE

**”Could This Be the Start of World War III?” (Niall Ferguson, The Free Press)**

Ferguson argues the U.S.-Israeli air campaign against Iran is best understood not as the opening of a world war but as the latest front in a broader cold war with China, one that makes strategic sense only in that global context. The critical variable is duration: a short conflict resembles Gulf War I, but if the Strait of Hormuz remains

closed for weeks, the resulting oil shock could rival the 1970s, inflicting serious economic damage on energy-importing allies in Europe and Asia while inadvertently benefiting Russia and testing U.S. weapons stockpiles needed for deterrence in the Indo-Pacific.

**Donald Trump Calls for More US Military Action in Latin America (Financial Times)**

Trump launched the “Shield of the Americas” coalition with a dozen Latin American nations, urging allies to invite US joint military operations against drug cartels within their borders. Mexico, Brazil, and Colombia were deliberately excluded. Since January 2025, the US has conducted military actions in seven countries, including Venezuela, Iran, Ecuador, and others, despite Trump campaigning on ending foreign entanglements. For investors, the expansion of US military operations across multiple theatres simultaneously has direct implications for defense budgets, fiscal deficits, and Latin American commodity flows.

**”Iran Conflict: Oil Price Impacts and Inflation” (Morgan Stanley Wealth Management, March 2026)**

Morgan Stanley frames the investor calculus around seven things to watch, noting that markets have historically posted double-digit gains during wartime, including both Gulf Wars, but warns that a prolonged conflict creating oil above $100 would be “qualitatively different.”

**”BlackRock Limits Withdrawals from $26 Billion Private Credit Fund” (Bloomberg)**

BlackRock gated redemptions at its flagship HPS Corporate Lending Fund after investors requested 9.3% of NAV in a single quarter, the third major private credit fund to restrict withdrawals in six weeks. The $1.8 trillion private credit market, built during a decade of low rates and loose underwriting, is now facing its first real stress test. The catalyst isn’t just rising rates or geopolitical shock; it’s AI eroding the business models of the software companies that dominate these loan books. When the world’s largest asset manager starts telling investors they can’t get their money back, it’s no longer an isolated incident.

**”China Sets Growth Target at 4.5%–5% for 2026” (Al Jazeera / NPR / Bloomberg, March 5–6)**

China set its lowest growth target since 1991, signaling continuity over stimulus as it navigates a property slump, tariff wars, and now an energy shock from the Middle East. The government also unveiled its 15th Five-Year Plan, committing roughly $4.3 trillion in public spending with a heavy emphasis on AI, semiconductors, and aerospace. Premier Li Qiang was blunt: “Rarely in many years have we encountered such a grave and complex landscape.” The lower target isn’t a weakness; it’s Beijing buying room to restructure without overpromising, while the Five-Year Plan doubles down on technological self-reliance in a world that’s fragmenting fast.