Japan: Land of the Rising Sun, Still

Japan's recovery keeps defying the doubters. Why a soft GDP print looks like an aberration, not a return to stagnation.

Japan appears prone to cyclical hiccups, judging from the latest GDP report. Having narrowly averted a technical recession in the fourth quarter of last year, Q1 growth reverted to contraction territory at an annualized -2.0% (consensus -1.2%). The print was partly due to temporary factors, including earthquake and scandal-related shutdowns of auto plants. Still, domestic consumption continues to be the weak link, as nominal wage growth has yet to catch up with the post-pandemic upturn in inflation.

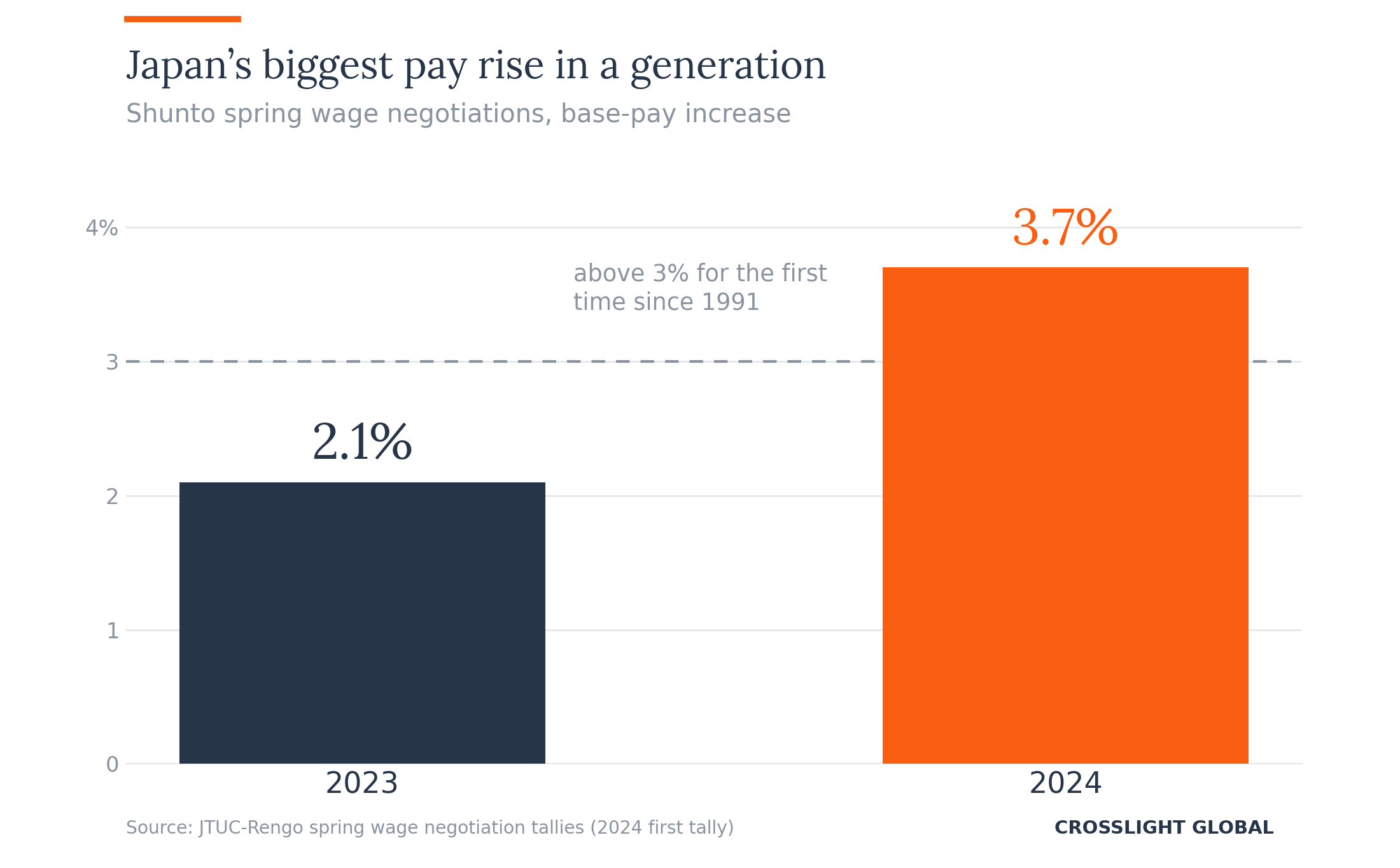

Indeed, with headline inflation resolutely above the 2% target in the past two years, the Bank of Japan in March lifted its policy rate to a range of 0% to 0.1%, from minus 0.1% to 0% previously, effectively ending the world’s last negative rates regime. Barring a brief period from 2006 to 2008, short-term policy rates in Japan have been near-zero or moderately negative since the implementation of a zero-interest rate policy in February 1999. Recent comments from policymakers suggest that incremental tightenings are on track in light of the recent breakthrough in wage negotiations. Companies have committed to base pay hikes of 3.7%, the largest increase in more than 30 years.

Ironically, interest rate hikes are occurring alongside currency weakness, with the JPY down around 9% against the USD in the year-to-date. Moreover, its longstanding status as a safe haven currency now appears less straightforward. Both developments seem counterintuitive at first blush. However, empirical research suggests past risk-off gains in the JPY were driven by portfolio rebalancing activities (such as offshore derivative transactions for both hedging and speculative purposes) rather than relative yield differentials. By design, safe haven currencies typically have low rates (negative, in the case of the JPY) and tend to be under-allocated in normal market conditions.

To be sure, there are economic tailwinds arising from a cheap currency, including bolstering corporate earnings and enticing inbound tourists. That said, trend weakness in the JPY could be problematic in at least three ways. First, the overseas relocation of Japanese manufacturing in the past decades (40% of the total, by some estimates) and the high value-added nature of onshore output have led to a decline in export sensitivity to the exchange rate. Second, the passthrough from higher import prices could accentuate the drag on real household incomes. Third, excessive movements in the currency might erode domestic confidence. Even so, the Ministry of Finance will likely eschew currency intervention as a rule. Policy activism has had limited lasting impact, as demonstrated by official efforts to prop up the JPY in the fall of 2022.

While the disappointing GDP report could rekindle fears of secular stagnation, CrossLight views the Q1 print as an aberration rather than a trend. True, significant structural hurdles remain in Japan, notably demographics. Yet, there are reasons to be optimistic. From a capital flows standpoint, Japan is benefiting from the global shift in geopolitics. In equities, investors’ rotation from China to Japan has helped spur stock prices to post-bubble highs. In direct investments, Taiwanese chipmaker TSMC earlier this year opened its first semiconductor plant in the country. Separately, the progressive relaxation of foreign worker quota is helping to alleviate labor market rigidities. Last year, the number of foreign workers in the country exceeded 2 million for the first time. With the size of its economy neck and neck with Germany’s, these developments augur well for Japan’s economic revival.

---

Tags: Japan, Global Macro, Currencies, Fixed Income, Emerging Markets