Monetary Policy Cycle

Five major central banks, five different decisions in a single week. Why policy cycles have desynchronized, and what it means for non-US assets.

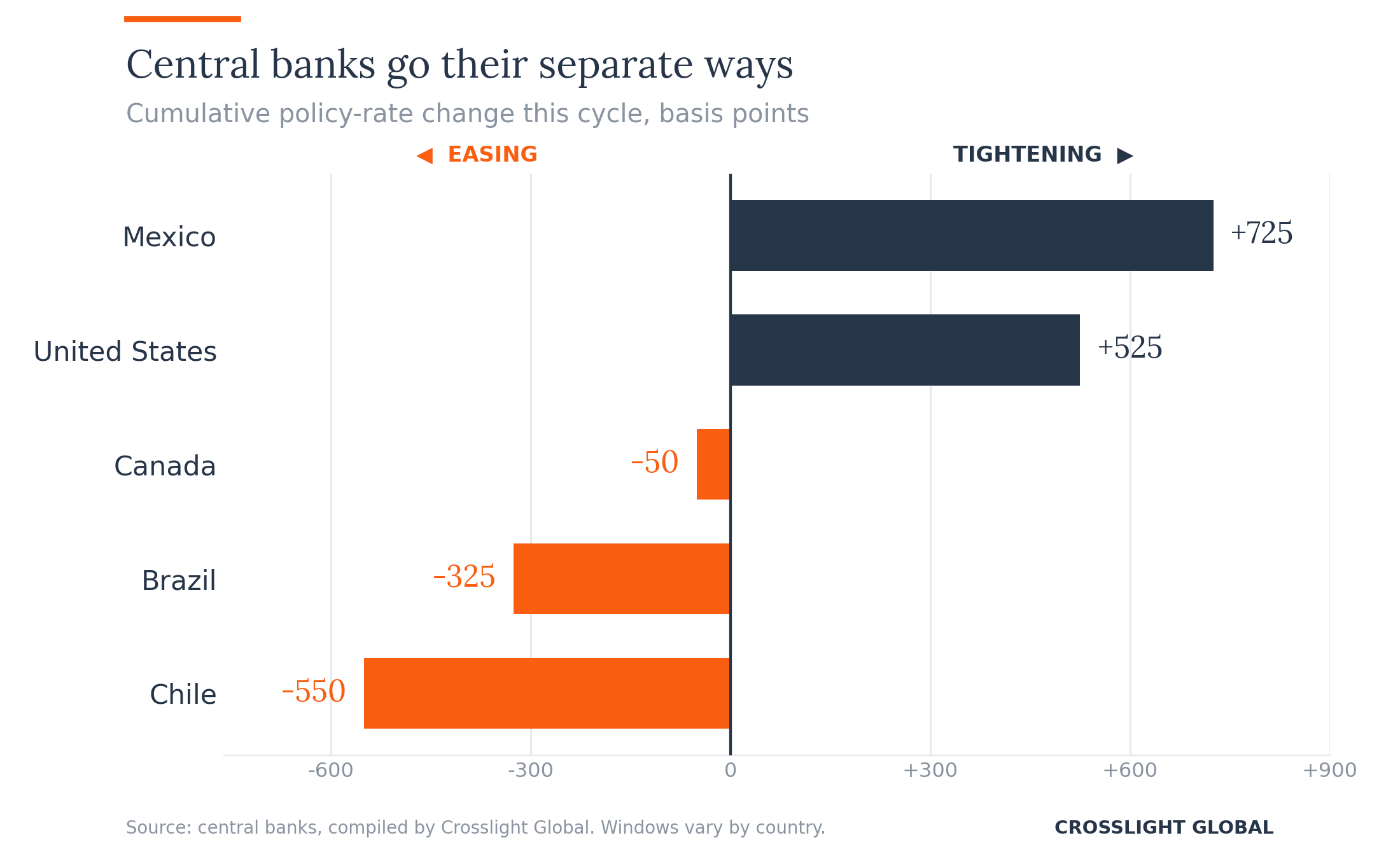

This week, five major central banks (the US, Brazil, Chile, Colombia, and Japan) are scheduled to announce their policy decisions. Top on the focus list is the US Fed, which is widely expected to maintain the status quo, having tightened +525 bps between March 2022 and July 2023. In Latin America, Brazil and Chile are likely to stand pat as well. The stark difference, though, is that both central banks began aggressively cutting rates a year ago, with the cumulative ease totaling -325 bps for Brazil and -550 bps for Chile. Neighboring Colombia looks set for another reduction, following five cuts since the turn of the year. In striking contrast, following the end of its negative rates regime in March, ingredients appear in place for Japan to implement a second hike by the end of Q3.

The policy smorgasbord, in turn, is an outcome of increased divergence in growth and inflation trends observed in the post-pandemic period. EM central banks, who were the first to acknowledge the pandemic-induced risk in inflation, initiated the global tightening cycle in early 2021, well ahead of their DM counterparts. The subsequent Russian invasion of Ukraine in February 2022 likely extended the duration of the EM hiking cycle, particularly for Central and Eastern European countries. Nevertheless, with the notable exception of the US, the monetary stance across DM and EM over the past year had begun pivoting in favor of growth. In June, the ECB delivered its first rate cut since 2019. Earlier this month, China surprised markets by trimming key interest rates in the hope of stimulating growth. Alongside Japan, Turkey is an outlier: the central bank in March 2024 lifted the policy rate by +500 bps to 50% to counter stubbornly high inflation.

Arguably, policy decisions have become less correlated even for economies with historically strong ties. The North American trio (Canada, Mexico, and the US) presents a case in point. Last week, the Bank of Canada reduced its policy rate by 25 bps, marking a second consecutive cut after a similar move at the June meeting. Mexico began its hiking cycle in mid-2021, a three-quarter lead versus the US. Between June 2021 and March 2023, Mexico undertook a cumulative tightening of +725 bps, more than twice the pace of +325 bps in the US. Among other factors, this likely helped underpin the MXN’s relative strength over this period.

Absent an unanticipated price shock, the medium-term policy trajectory going forward is biased toward global easing, although a reversion to a generalized low-rate environment of the past is highly unlikely. Specifically, three interrelated factors are likely to drive a continuation of desynchronized monetary cycles. First, trade restrictions and protectionist policies could present a challenge to a sustained trend of disinflation globally. Second, the pivot away from globalization to domestic industrial targeting is vulnerable to a combination of policy lapses and implementation missteps. Third, US election uncertainty means that the market risk premium might stay elevated for now. Indeed, the Fed’s decision to maintain its key rate at close to the current peak may temporarily limit the room for further easings elsewhere without running a risk on their currencies. In this regard, EM countries tend to be more susceptible to capital outflows.

CrossLight expects interest rate differentials to play an active role in driving global asset prices. Given our central conviction that a theme of US exceptionalism will likely prevail through year-end, we see little urgency for the Fed to act for now, except for the purpose of an insurance cut, as the US easing cycle could be shallower than what market participants currently priced in. Given the recent strength in rates, we are cautious about duration and positioned for curve steepening. On the other hand, we advocate accumulating select non-USD assets as value opportunities present themselves in the second half of 2024, favoring countries with supportive fundamentals and carry appeal.

---

Tags: Monetary Policy, Global Economy, Interest Rates, Global Macro, Emerging Markets