Most Investors Think They Own Gold. They Don't.

Why Gold, Why Now: Structure, ownership, and the macro case for the world’s oldest reserve asset

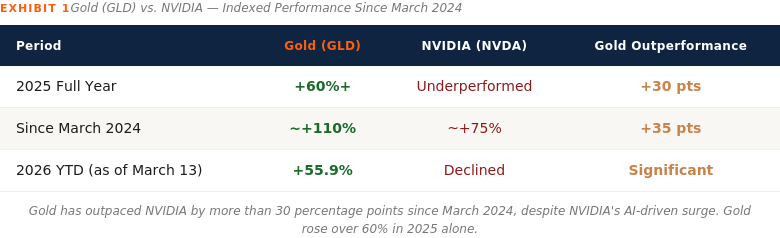

Gold rose more than 60% in 2025. Since March 2024, it has even outperformed NVIDIA by more than 30 percentage points. Price moves of that magnitude attract attention quickly, but the current case for gold is less about momentum and more about the macro environment in which portfolios now operate.

Anyone who has spent time on a trading desk knows that moves like this usually tell you something about the environment investors are navigating.

The Policy Backdrop

The current administration’s increasingly public tension with the Federal Reserve around interest rates introduces uncertainty around the future path of monetary policy. Markets have recently pulled back from pricing aggressive rate cuts, but the direction of policy still matters. If rates ultimately move lower while inflation remains sticky — a scenario markets have experienced before — investors historically begin shifting toward stores of value. Gold has often been one of the primary beneficiaries of that shift.

There is also a straightforward portfolio dynamic at work. When economic growth slows, dividends compress, or real yields decline, the opportunity cost of holding a non-yielding asset falls. In that environment, gold’s lack of income becomes less of a disadvantage relative to other assets. Lower interest rates also tend to weaken the U.S. dollar, which has historically supported higher gold prices.

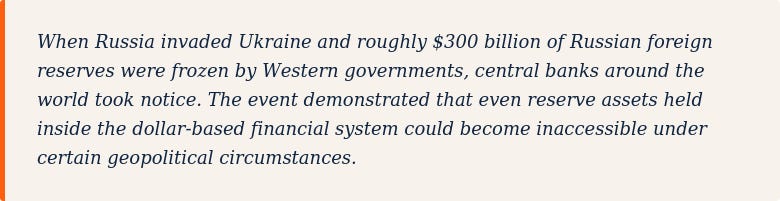

Beyond monetary policy, a deeper structural trend is also emerging. Since the Russia/Ukraine conflict, central bank gold purchases have accelerated to near-record levels. The logic is straightforward. Gold remains one of the few reserve assets that sits outside the modern financial system and outside the direct control of any single government.

What Investors Actually Own

A second issue that receives less attention is the structure of the gold market itself.

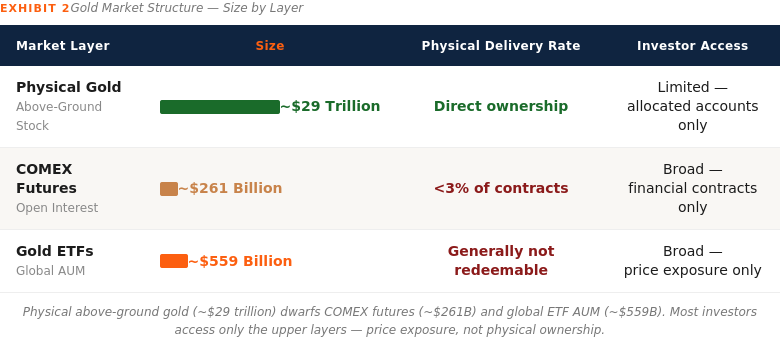

The global gold ETF market is currently valued at roughly $559 billion. That sits on top of a physical gold market estimated at approximately $29 trillion in above-ground value. In other words, the ETF layer represents only a small fraction of the underlying asset.

More importantly, many ETF investors do not actually hold gold as they believe.

Consider the largest gold ETF, GLD, which holds roughly $147 billion in assets. The trust stores gold through HSBC as its primary custodian, with the potential for additional sub-custodial arrangements. Investors purchasing shares in the ETF are buying an interest in the trust rather than a direct title to specific bars of gold.

In normal market conditions, that structure functions well as a trading instrument. But it is important to understand the difference between price exposure and physical ownership. Most individual investors cannot redeem ETF shares for allocated bullion.

Below the ETF market sits something even larger: the futures market. COMEX in New York handles the majority of global gold futures trading. Open interest reached roughly $261 billion in late 2025. Yet fewer than three percent of those contracts ultimately result in physical delivery. Most are simply financial contracts tied to the price of gold rather than claims on the metal itself.

Periods of market stress occasionally reveal the difference between those layers. During the market disruption in March 2020, premiums on physical coins rose sharply while electronic gold prices remained relatively stable. When financial markets experience strain, paper claims and physical metal can move in different ways.

That possibility is not hypothetical. It is precisely the type of environment gold is meant to hedge.

Most investors access only the upper layers — price exposure, not physical ownership.

Perspective for Investors

It is important to be clear about what this note is and what it is not. This is not a recommendation to buy gold today. Markets move in cycles, and gold itself has experienced long periods of both strength and weakness.

The purpose of this note is simply to encourage investors to understand what they actually own in their portfolios.

Too often in our industry, conversations about assets drift toward buzzwords and narratives. Investors hear the same themes repeated across television, conferences, and publications like Barron’s, but the underlying structure of the investment is rarely examined closely.

For investors evaluating gold exposure, ownership structure matters.

Allocated physical bullion stored in segregated vault storage represents the most direct form of ownership. A bank safe-deposit box is frequently misunderstood; in certain bank failure scenarios, the holder may still be treated as an unsecured creditor.

For investors seeking exchange-listed exposure while maintaining a clearer claim to physical metal, the Sprott Physical Gold Trust (PHYS) offers a different structure. The trust stores allocated bullion at the Royal Canadian Mint and publishes serial numbers for individual bars. The structure avoids derivatives and allows for the redemption of shares for physical metal under defined conditions.

Exchange-traded funds such as GLD and IAU remain useful instruments for investors seeking price exposure. The challenge arises when those instruments are assumed to represent direct physical ownership.

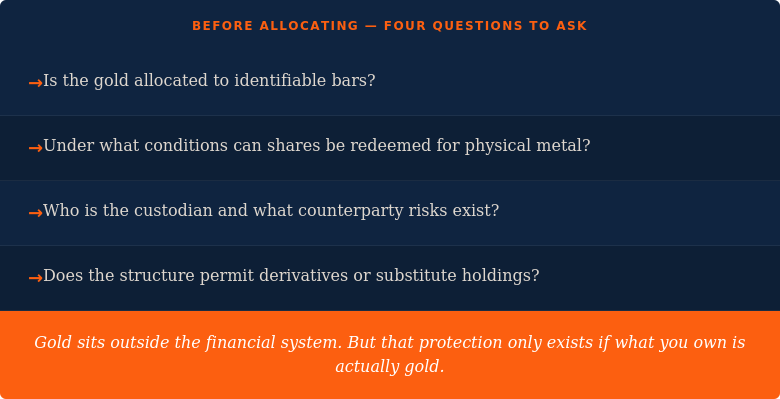

Before allocating capital to gold, investors should ask several structural questions:

If those questions cannot be answered clearly, the investor may be gaining price exposure rather than the systemic hedge gold is often intended to provide.

Gold has always played a role in portfolios because it sits outside the financial system. But that protection only exists if what you own is actually gold. Understanding that distinction is where serious investing begins.

CrossLight Global Investments

This article is strictly for informational purposes only and does not constitute investment advice. CrossLight Global Investments is a registered investment adviser. Past performance is not indicative of future results.

Copyright © 2026 CrossLight Global. All rights reserved.

By CrossLight Global Investment Partners on March 16, 2026.

Exported from Medium on March 23, 2026.