The Emerging Market Playbook is Now a Developed Market Necessity

Inflation, debt, currency shocks, liquidity cracks. The fault lines once confined to emerging markets are now showing up in the US.

I’ve spent most of my career observing global markets from a seat that was not in the spotlight, but close to the action. Through many of the major events of the last two decades, my job was to make sense of the noise and relay what I was seeing to some of the world’s largest institutional investors. I had to earn trust by being clear-eyed, steady, and informed, especially when the path ahead wasn’t clear.

That experience shaped the way I see things today. Because when I look at the U.S. market in 2025, I see something eerily familiar. It feels a lot like the environments I once saw in places people used to call “too risky.”

Rising inflation, debt sustainability concerns, geopolitical flare-ups, currency risk, political dysfunction, liquidity cracks, all of it. These are the same fault lines we’ve seen across the emerging world for decades. The only difference now? They’re showing up in the U.S. and other developed markets.

This article isn’t about doom and gloom. It’s about pattern recognition. It’s about bringing the lessons learned from emerging market investing into today’s conversation. Because if you’ve never seen what happens when policy credibility fades or when liquidity dries up, you’ll want someone on your team who has.

## Inflation: Uncomfortable, Not Uncharted

U.S. inflation remains the top financial concern for households and a persistent risk for markets. In April 2025, Gallup found that 29% of Americans cited inflation or the cost of living as their top concern, for the third consecutive year.

And yet, I can’t help but put this in perspective.

In 2022, Turkey’s inflation surged to 80%. Grocery staples doubled in price. The currency tanked. And the government, after making a series of unorthodox rate cuts, had to reverse course with aggressive hikes to stop the outflows away from the Lira. Brazil did the same in 1999, pushing its Selic rate to 45% after a currency devaluation.

By comparison, the 5 to 6% inflation we’re seeing in the U.S. feels intense, but it’s manageable. That doesn’t mean it’s harmless. When inflation erodes confidence in central banks, markets become volatile quickly. However, emerging markets have shown us that it’s not just about the number. It’s about how you respond.

## Geopolitical Shocks: The Market’s Oldest Blind Spot

Markets don’t price in war until it’s at the front door. However, when conflict arises, it affects everything, commodities, interest rates, currencies, and risk appetite.

That’s not just theory. During Russia’s 1998 default, geopolitical instability and economic mismanagement caused a major crisis. Russian bonds plummeted. Capital quickly moved out. And the contagion wasn’t limited to Moscow. U.S. hedge fund Long-Term Capital Management (LTCM) was so exposed that the Federal Reserve had to organize a bailout to stop a broader market crash.

Fast forward: Russia’s invasion of Ukraine in 2022 caused a commodity shock, triggered sanctions, and sent investors scrambling for safety.

IMF data shows that emerging-market equities decline about 5% per month during major conflicts, more than doubling the drop seen in developed markets. Why? Because geopolitical risk impacts EM more severely. But here’s the catch: as global interconnectedness increases, those same dynamics are affecting Wall Street.

Experience navigating EM shocks isn’t just a niche anymore, it’s necessary.

## Debt Sustainability: The Numbers Are Starting to Rhyme

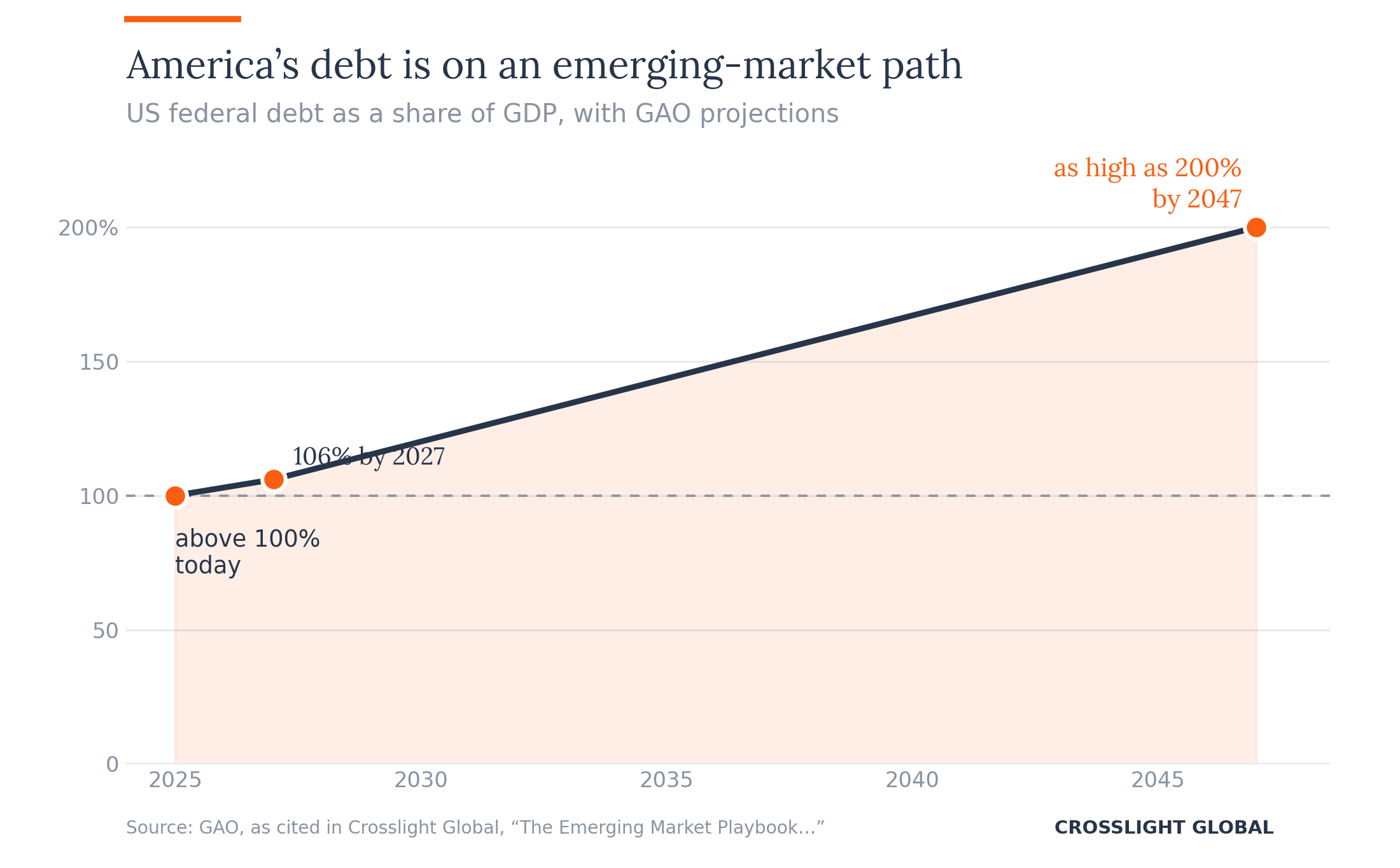

The U.S. national debt now sits above 100% of GDP. According to the GAO, that number could reach 106% by 2027, with projections as high as 200% by 2047 if nothing changes.

These used to be emerging-market numbers.

Argentina’s 2001 default on $100 billion of sovereign debt was catastrophic, but not a surprise. They had pegged the peso to the dollar, borrowed aggressively, and failed to grow. When the math broke, the country fell into recession, froze bank accounts, and defaulted. Even after multiple restructurings, Argentina has defaulted on its debt nine times in its history.

The U.S. has more tools, yes. But markets care about trajectory, not just destination. If fiscal credibility erodes, investors demand a premium, or they walk. The EM lens teaches you to spot those early tremors.

## FX Volatility: Not Just for Currency Traders Anymore

In emerging markets, currency risk is baked into every decision. But in the U.S., it’s often ignored, until it becomes a headline.

But look around. The dollar’s strength or weakness is shaping global liquidity conditions. High rates here have pulled capital from abroad. A dollar slide could ignite inflation. A dollar surge could break something overseas.

This isn’t theoretical.

During the Asian Financial Crisis in 1997, Thailand’s baht collapsed after the country dropped its dollar peg. Within months, the baht fell 60%, the Indonesian rupiah 47%, and the Malaysian ringgit 35%. Countries raised their rates to defend their currencies, crushing domestic growth in the process. One crack in the system became a regional collapse.

In 2025, the U.S. dollar is at the center of the global web. If volatility spikes, the fallout could be international. EM investors know this dance. We’ve had to hedge, adapt, and move quickly. That muscle memory matters now more than ever.

## Political Instability: It’s No Longer Just “ThEM”

Political dysfunction used to be a reason to discount EM assets. Now, it’s part of the U.S. investment backdrop.

Debt ceiling showdowns. Budget gridlock. An election cycle that feels more like a civil war than a democratic process. Markets are watching all of it.

Morgan Stanley has called out rising U.S. policy uncertainty as a material risk. And rightly so. In 2015, Brazil’s President Dilma Rousseff was impeached amid allegations of corruption and fiscal mismanagement. The result? A stalled economy, falling investment, and whipsawing markets. It wasn’t just political drama. It was a macro event.

The U.S. isn’t immune. And investors are learning that political stability can’t be taken for granted.

## Liquidity Risk: It’s Always the Last Thing You See Coming

In calm markets, liquidity feels infinite. In a crisis, it vanishes.

In March 2020, we saw that even U.S. Treasuries, usually the safest and most liquid investments, can become challenging to trade when too many people try to sell at once. By 2023, both the IMF and U.S. regulators were sounding the alarm that it’s getting harder to buy and sell bonds without moving prices, largely because big banks are holding fewer bonds and markets are becoming more volatile.

As I already said, this isn’t theoretical. In 1998, after Russia’s default, funds dumped anything they could to raise cash. Prices gapped. Volatility exploded. LTCM almost broke the system.

EM managers are trained to survive this. It’s not just about alpha, it’s about survival. When there are no bids, you need conviction, calm, and a plan.

## Final Word: The Markets Have Changed. Have You?

If you’ve made it this far, here’s what I want you to take away:

You don’t need to panic. But you do need to prepare.

Many of the risks we see in developed markets, rising inflation, unsustainable debt, policy uncertainty, currency shocks, and liquidity gaps, are not new. They have occurred for decades in emerging markets. Those of us who have invested through these cycles have developed a mindset of discipline, humility, and effective risk management.

This isn’t about “I told you so.” It’s about offering perspective. Many people are encountering this level of complexity for the first time. EM folks have lived it for years.

So, if you’re building a team, a portfolio, or a plan for what’s next, you want people who’ve been here before. People who’ve managed through volatility. People who know what to do when the headlines get scary and the exits get crowded.

We’re not just in uncertain times. We’re in emerging ones.

---

*Tags: Emerging Markets, Global Macro, Inflation, Investing, Fixed Income*