The Persistence of US Exceptionalism

America keeps outgrowing the rest of the world. Why the exceptionalism theme is proving stubborn, and what it means for global bonds.

Today’s downside surprise in US GDP contrasts with a recent string of strong activity releases, while the road to disinflation remains uneven. US growth came in at an annualized 1.6% (consensus 2.5%) in Q1. Of note, underlying inflation accelerated to a faster-than-expected 3.7% (consensus 3.4%) in Q1, fueled by a pick-up in services cost.

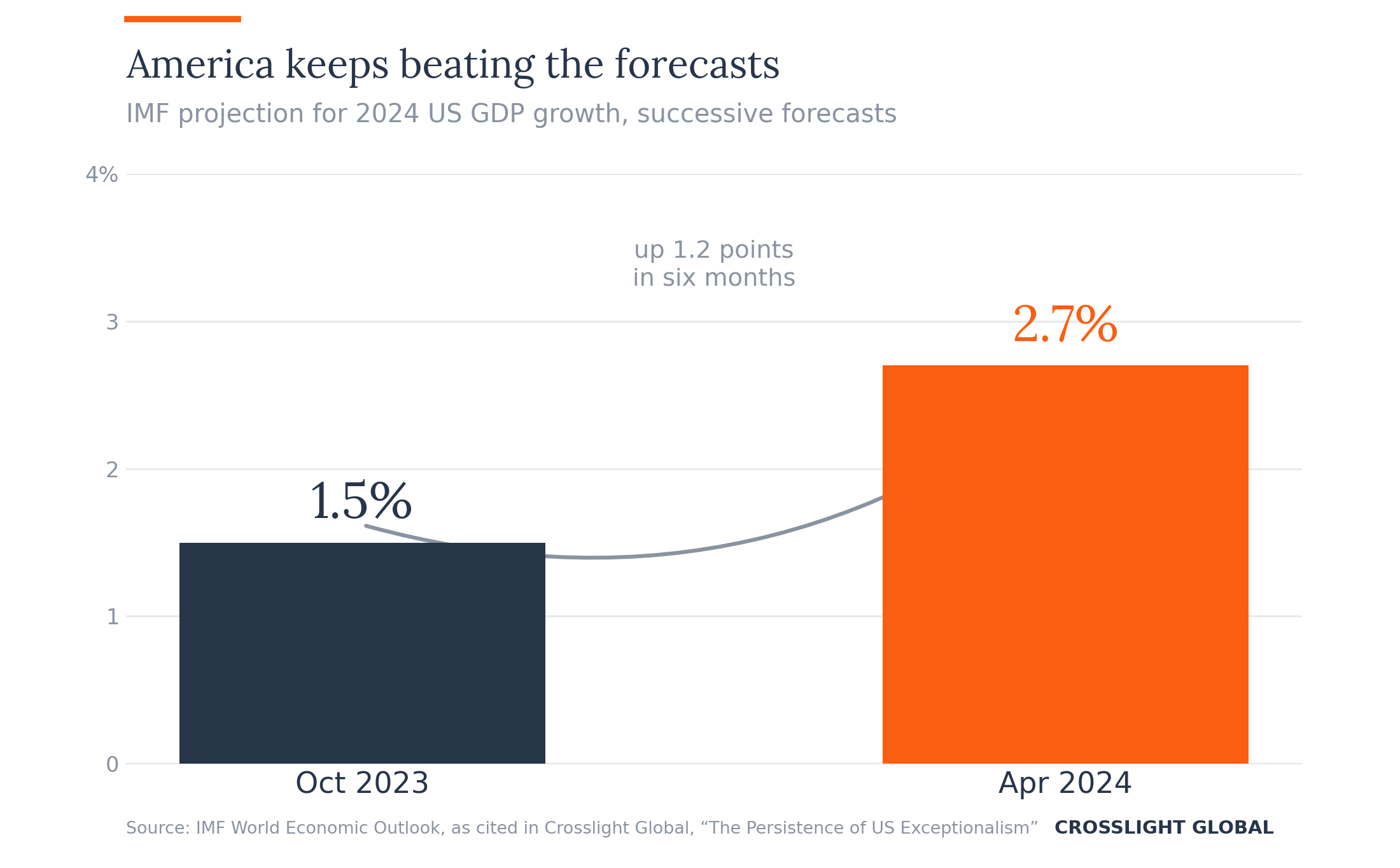

Notwithstanding the disappointing GDP print, the US economy continues to hold up well relative to the rest of the world, reinforcing an ongoing theme of US exceptionalism. Indeed, the IMF earlier this month boosted its 2024 US GDP forecast to 2.7% in the latest World Economic Outlook, markedly higher than 1.5% just six months ago. The upgrade is striking, given that the cumulative 525-bp hike in the Fed funds rate during 2022-23 had previously fanned fears of recession, which, to many market punters, would justify monetary easings as early as March this year.

While firm growth itself is not necessarily an obstacle for rate cuts, there is little urgency for the Fed to reverse course until further clarity on inflation emerges. CrossLight’s base case is for the Fed to stand pat on policy through year-end, but we acknowledge the possibility of an “insurance” ease to cushion potential risks to next year’s growth outlook.

To be sure, the notion of US exceptionalism is not new. As recently as 2018, US growth reached a 13-year high of 2.9%, outpacing not only its developed counterparts but also large EM economies including Brazil (1.8%) and Mexico (2.0%). The point is that diverging economic trends are now becoming more of a norm.

As a case in point, while the US continues to grapple with the inflation narrative, China is saddled with the equally problematic issue of deflation. Moreover, in the face of heightened trade frictions, reshoring production closer to the home region is reconfiguring the global production grid that will result in winners and losers.

From an investment standpoint, the higher-for-longer scenario for US rates presents both a challenge and an opportunity for global bonds. As global policy trajectories pivot away from synchronization to differentiation, global investors with a long-term horizon stand to benefit from fundamental price dislocations in a generalized risk-off environment.

---

Tags: US Economy, Global Macro, Interest Rates, Fixed Income, Emerging Markets