Weekly Perspectives - June 21, 2026

The records keep coming, but a handful of tech giants are doing the work, at valuations seen only once before, in December 1999. A tougher Fed and a closed Strait of Hormuz now test the calm

American stocks keep hitting records. But the gains are increasingly the work of a few big technology companies, trading at some of the highest valuations in history, while most other shares go nowhere. That makes the market more fragile than the headline figures suggest. Last week brought two fresh tests of those few names, a tougher new chairman at the Federal Reserve and a flare-up in the Gulf. Investors bought anyway.

## MARKET RECAP: Hope Springs Eternal

A preliminary peace deal between America and Iran cheered investors last week, more than canceling out a surprisingly tough debut by the Federal Reserve’s new chairman, Kevin Warsh. The pattern is now familiar: since the lows of late March, good news has been celebrated and bad news waved away, and global share prices have climbed to one record after another even as the risks have piled up. That tension turned real as we went to press. Iran has reportedly closed the Strait of Hormuz, the narrow waterway through which about a fifth of the world’s seaborne oil passes, after accusing Israel of breaking the ceasefire, a claim Washington disputes. Two things stood out in the week’s trading.

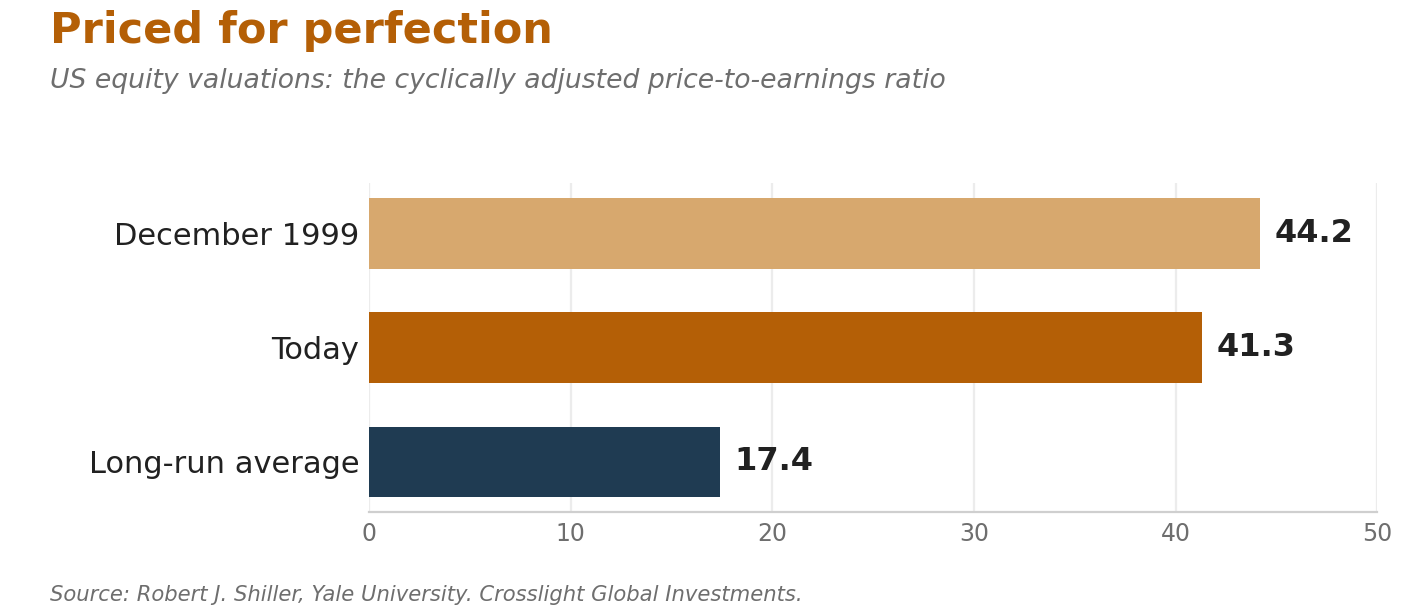

**The rally is all about technology.** So far this year America’s tech-heavy Nasdaq index has risen 14.1 percent, almost twice the 7.3 percent of the older-economy Dow Jones and well ahead of the broad S&P 500’s 9.6 percent. Yet beneath that headline gain, 43 percent of the companies in the S&P 500 are actually down on the year. The index is being pulled up by a handful of giant firms. The story is the same abroad, where the tech-dominated markets of South Korea and Taiwan have jumped 115 percent and 60 percent. The worry is the price. One widely used measure compares share prices with company profits averaged over ten years and adjusted for inflation, to smooth out the swings of the economy. It now stands at 41.3. The only time it has been higher was 44.2 in December 1999, just before the dot-com crash. Its long-run average is 17.4.

**The new Fed is saying less.** Mr Warsh’s first policy statement ran to just 132 words, less than half the usual length. The brevity looks deliberate, and it works: a shorter statement makes the main point harder to miss. Last week that point was the final sentence, “The Committee will deliver price stability,” about as clear a signal as a central bank gives that it is in no mood to cut interest rates. Fewer words may also mean fewer mistakes, since an odd decision that does not match what is happening in the economy is easier to spot. The exception is a genuine crisis, when staying quiet costs confidence rather than saving it.

**Key Takeaways**

- The US-Iran deal removes some of the near-term threat to the world economy, for now.

- Geopolitics is the weak point. A lasting global recovery is hard to build while the Gulf can erupt without warning.

- Share prices are high and interest rates are higher than markets would like, which leaves little room for disappointment.

**Stocks.** The prospect of a quick end to the standoff in the Gulf did most of the work. In a holiday-shortened week America’s S&P 500 rose 0.9 percent and the Nasdaq 2.6 percent. Asia led the way, with South Korea up 11.4 percent, and most European markets gained 2 to 3 percent.

**Bonds.** The Fed’s tougher tone hit short-term government bonds hardest, since their value depends most on the next few interest-rate decisions. The interest rate on a two-year US government bond rose to 4.18 percent, while the rate on a thirty-year bond slipped to 4.90 percent, having topped 5 percent only days earlier. (When the interest rate on a bond rises, the bond itself is worth less to anyone already holding it.) Borrowing costs also rose in Britain and the euro area. The exception was Brazil, where the rate to borrow for ten years jumped to 14.8 percent after its central bank cut rates even as the inflation outlook worsened.

**Currencies.** The dollar rose as nervous investors looked for somewhere safe, helped by the prospect of higher American interest rates. The most striking move was the Japanese yen, which weakened to 161.30 to the dollar even after the Bank of Japan raised interest rates, prompting fresh talk of government action to prop it up. The Indian rupee went the other way, firming on hopes the Strait would soon reopen, though it remains one of the year’s weakest currencies.

**Commodities and alternatives.** Anything that pays its owner nothing to hold had another poor week, squeezed by the peace deal and the strong dollar. Brent crude oil fell almost 8 percent, a second weekly drop in a row. Precious metals fell across the board, wiping out their gains for the year; gold, at $4,156 an ounce, is now 23 percent below the record it set in late January. Bitcoin stayed weak at around $63,000, less than half the $126,200 it reached last October.

## LOOKING AHEAD THIS WEEK

**Inflation, again.** The week’s most important number is the Fed’s favorite measure of inflation, known as core PCE, due on Thursday. Prices are expected to have risen enough in May to push the annual rate to 3.4 percent, the highest in two and a half years and an uncomfortable figure for a central bank that has just promised price stability. Surveys of business activity in America and the euro area on Tuesday, and in Japan on Monday, should show the economy still growing, if slowly. And Taiwan’s export orders on Tuesday, a good gauge of demand for technology, are expected to have jumped 49 percent on the year.

**Central banks drifting apart.** Mexico’s central bank is expected to hold rates at 6.50 percent on Thursday, ending the run of cuts it began in March 2024. Thailand should also keep rates steady, at 1.00 percent, on Wednesday. Hungary, going the other way, is likely to trim its rate to 6.00 percent on Thursday. The theme keeps recurring: the world’s central banks no longer move in step, and the gaps between them are where the opportunities in currencies open up.

**The Strait is the wild card.** The calm in markets assumes the trouble in the Gulf will be short-lived. If the Strait of Hormuz stays closed, oil prices will not stay down, and the inflation problem already worrying the Fed will get harder to solve. It is the clearest risk, in either direction, this week.

## HEARD THROUGH THE GRAPEVINE

**The Fed finds its voice by losing its words.** A 132-word statement is a small change with a big message. For years central bankers tried to guide markets with ever more language, until the guidance itself became something to worry about. The new approach bets that fewer words, clearly meant, are harder to misread. “The Committee will deliver price stability” does not leave much room for the hopeful reading investors tend to prefer. Last week they were still deciding whether to believe it.

**Oil’s calm faces a test.** For most of last week crude fell, as the US-Iran peace deal raised hopes that the Strait of Hormuz would soon reopen and the war’s supply shock would fade. Then, just as we went to press, Iran announced a fresh closure of the Strait, the most important bottleneck in the oil trade, a move Washington disputes. Markets have not yet had their say; the first real test comes when trading resumes. If investors treat the closure as a bargaining chip that will soon be reversed, the calm holds. If they do not, the cost shows up quickly, first at the pump and later in the inflation figures.

---

*Thank you for reading CrossLight’s Weekly Perspectives. If you wish to talk through any of these themes, please reply to this note. This note is strictly for informational purposes only and does not constitute investment advice for the reader.*

**Sources:** Bloomberg; Federal Reserve (June FOMC statement); US Bureau of Economic Analysis (PCE); S&P Global and Institute for Supply Management business surveys; Bank of Japan; Banco de México; Bank of Thailand; Magyar Nemzeti Bank; Reserve Bank of India; Robert J. Shiller, Yale University (cyclically adjusted price-earnings data); Taiwan Ministry of Economic Affairs; Reuters; Financial Times; The Wall Street Journal; CNBC; John T. McCutcheon, “Taken for a Ride,” Chicago Tribune, 1929 (public domain).

*Copyright © 2026 CrossLight Global. All rights reserved.*